TODAY’S S&P 500 SET-UP - August 1, 2011

With the most anticipated headline since ‘sun rising in the East’ behind us, the question for risk managers now isn’t about debt deals – it’s about Growth and Earnings Expectations. I’m looking for those 2 things and Europig problems to take back the headlines in the coming week. As we look at today’s set up for the S&P 500, the range is 30 points or -0.49% downside to 1286 and 1.84% upside to 1316.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1028 (-303)

- VOLUME: NYSE 1209.50 (+22.56%)

- VIX: 25.25 +6.36% YTD PERFORMANCE: +42.25%

- SPX PUT/CALL RATIO: 2.30 from 1.60 (44.47%)

CREDIT/ECONOMIC MARKET LOOK:

BONDS – we’ve been on the other side of the PIMCO “credit risk” trade (El-Erian) and focused more on the 2 things that have really provided a bid for bonds since April – US Growth Slowing and Inflation Expectations coming down. New highs in 10 and 30 yr UST bonds on Friday into the “news” this morning. Don’t forget Q1 2011 US GDP was restated at 0.4% on Friday!

- TED SPREAD: 17.08

- 3-MONTH T-BILL YIELD: 0.10% +0.03%

- 10-Year: 2.82 from 2.98

- YIELD CURVE: 2.46 from 2.56

MACRO DATA POINTS:

- 10 a.m.: Construction spending, est. 0.1%, prior (-0.6%)

- 10 a.m.: ISM Manufacturing, Jul, est. 54.5, prior 55.3

- 11 a.m.: Export inspections: corn, soybeans, wheat

- 11:30 a.m.: U.S. to sell $27b 3-mo., $24b 6-mo. bills

- 4 p.m.: Weekly crop conditions

WHAT TO WATCH:

- Deficit agreement would cut $917b in spending over a decade, raise debt limit initially by $900b and assign special congressional committee to find another $1.5t in deficit savings by late Nov., to be enacted by Christmas

- HSBC to cut 30,000 jobs total worldwide by 2013 as part of plan to reduce costs by $2.5b-$3.5b; agreed to sell upstate NY branch network to First Niagara for ~$1b as it pares U.S. ops

- FedEx (FDX) CEO “largely upbeat” on outlook as economy improves, businesses start building inventories: Barron’s

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Commodities Rally as Deal Avoids ‘Act of Collective Insanity’

- Oil Advances From Two-Week Low as Lawmakers Reach Debt Agreement

- Gold Drops From Record as Obama Says Lawmakers Reach Debt Deal

- Copper Rises for Third Day as U.S. Debt Accord Averts Default

- Wheat, Corn Climb as U.S. Debt-Ceiling Accord Avoids Default

- Sugar Rises on Signals Demand Remains Steady; Coffee Advances

- Russia Targets Asia With Cheapest Wheat After Putin’s Export Ban

- ArcelorMittal, Peabody to Put Hostile Bid to Macarthur Holders

- S. African CEOs Told by Eunomix Nationalization May Happen

- Funds Raise Bullish Commodity Bets as Silver Holdings Jump

- BHP Billiton Workers Resume Strikes at Australian Coal Mines

- India’s Cotton Exports May Be Limited on ‘Lackluster’ Demand

- Commodities Beat Stocks, Bonds in July Amid China Expansion

CURRENCIES

EUR/USD – this is the one strike price that should continue to whip around in the next 48 hours as we finally put this dog to bed; watch 1.43 as your TREND line that inflates/deflates everything else (across asset classes). The global market’s correlation risk moves off that.

EUROPEAN MARKETS

- EUROPE: wet Kleenex action continues with European stocks doing nothing on the "news" that is only news to people who need to make it news

- July final Manufacturing PMI; France 50.5 vs preliminary 50.1; Germany 52.0 vs preliminary 52.1; Eurozone 50.4 vs preliminary 50.4; UK Jul Manufacturing PMI 49.1 vs consensus 51.0, prior revised 51.4 from 51.3

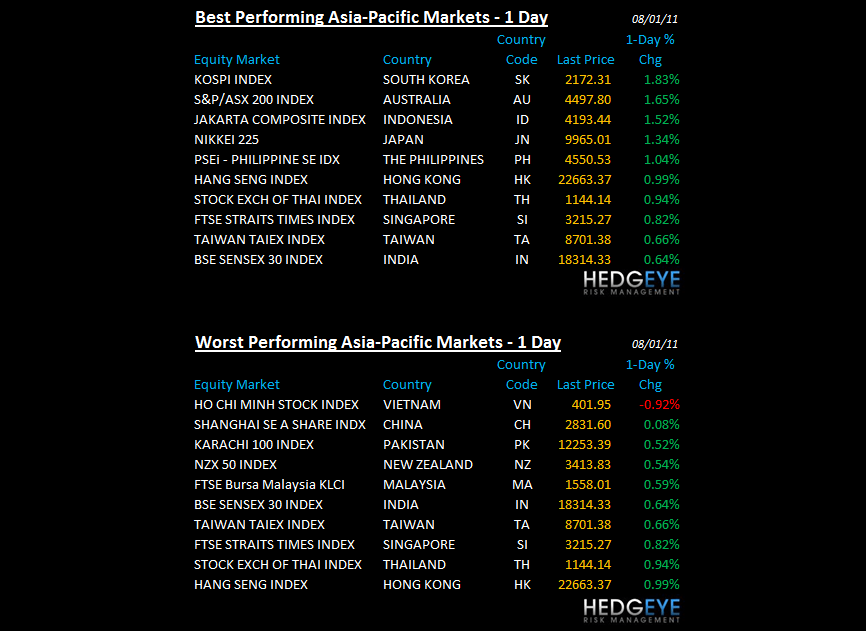

ASIAN MARKETS

- ASIA: broad based rally; no surprises; no consequential levels breached on the upside - I'm long China and India currently.

- China July PMI 50.7 vs 50.1 cons and 50.9 seq.

- Australia July manufacturing index 43.4 vs 52.9 seq.

- Australia June new home sales (8.7%) m/m.

MIDDLE EAST

Howard Penney

Managing Director