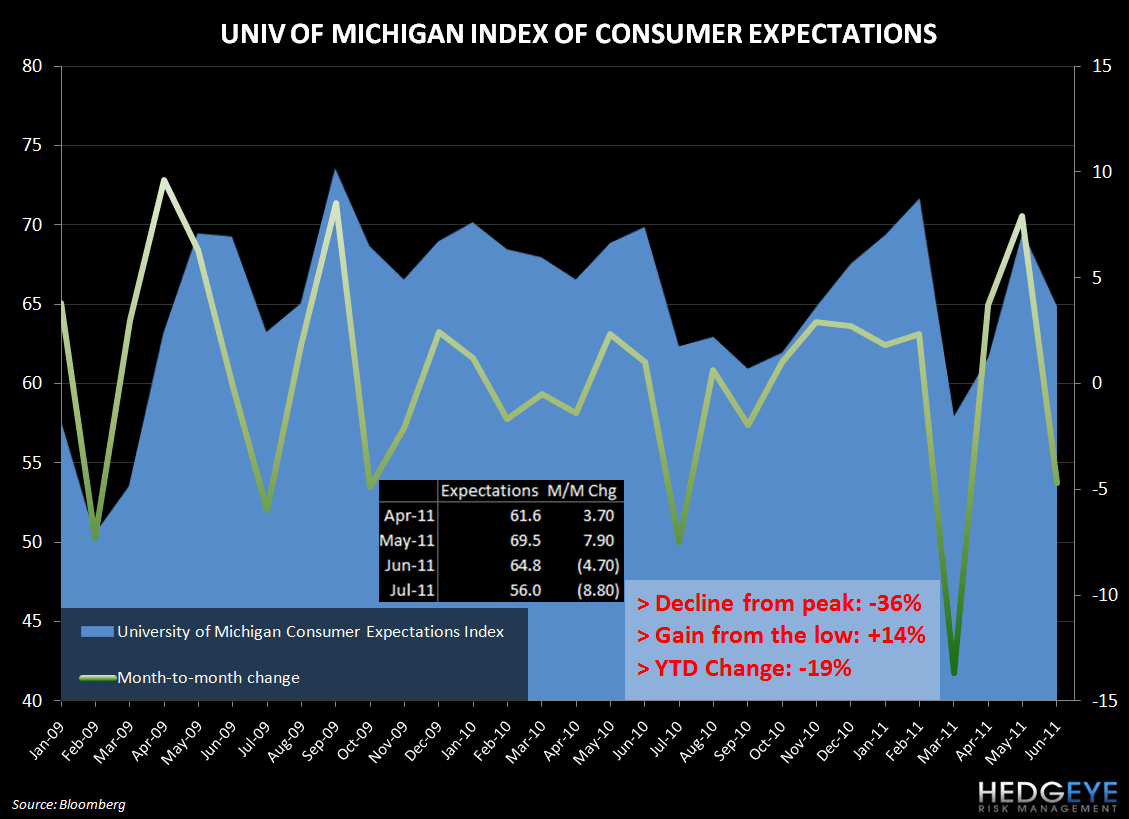

The University Of Michigan Survey Of Consumer Confidence Index collapsed in July. The ongoing employment crisis, reduced home prices, and still-elevated gas prices are weighing on sentiment. The embarrassing debacle in Washington is also likely causing concern.

Looking at the components of the Index, it was telling that expectations came down so sharply, from 64.8 in June to 56 in July. This is the lowest level since November 2009. The overall Sentiment Index declined 7.8 points to 63.7 in July. This month brought the largest decline since March and the lowest level for the Index since March 2009. Current Attitudes declined by 6.2 points to 75.8, the lowest level since November 2009.

With GPD growth slowing to a measly 1.3% in the second quarter, the employment situation showing no real signs of turning around, and gasoline prices at $3.70 per gallon on a national basis, it makes sense that consumers are fearful. The ceaseless media focus on the debt ceiling debate and the apparent incapability of the nation’s elected representatives to reach a resolution is also heightening concerns.

Howard Penney

Managing Director

Rory Green

Analyst