Positions in Europe: Short EUR-USD (FXE); Italy (EWI); UK (EWU)

As Keith noted in today’s Early Look, alarm bells sounded yesterday on a confluence of factors:

- EUROPE – both European stocks and bonds are turning into a proactively predictable train wrecks. Our research catalysts remain crystal clear (accelerating debt maturities for the majors through September) but, more importantly, now all of our TRADE and TREND lines across every major European stock and bond market (ex-Russia) have been broken and confirmed by volume and volatility studies.

- USA – stocks broke their intermediate-term TREND line of support (1320 in the SP500) and short-term bond yields finally busted a move above my 2-year yield TRADE line of resistance (0.41%). Credit risk derived by market morons in Congress will be priced on the short-end of the curve (where Bernanke has tried to mark it to model for 2 years), so watch that 0.41% line like a hawk.

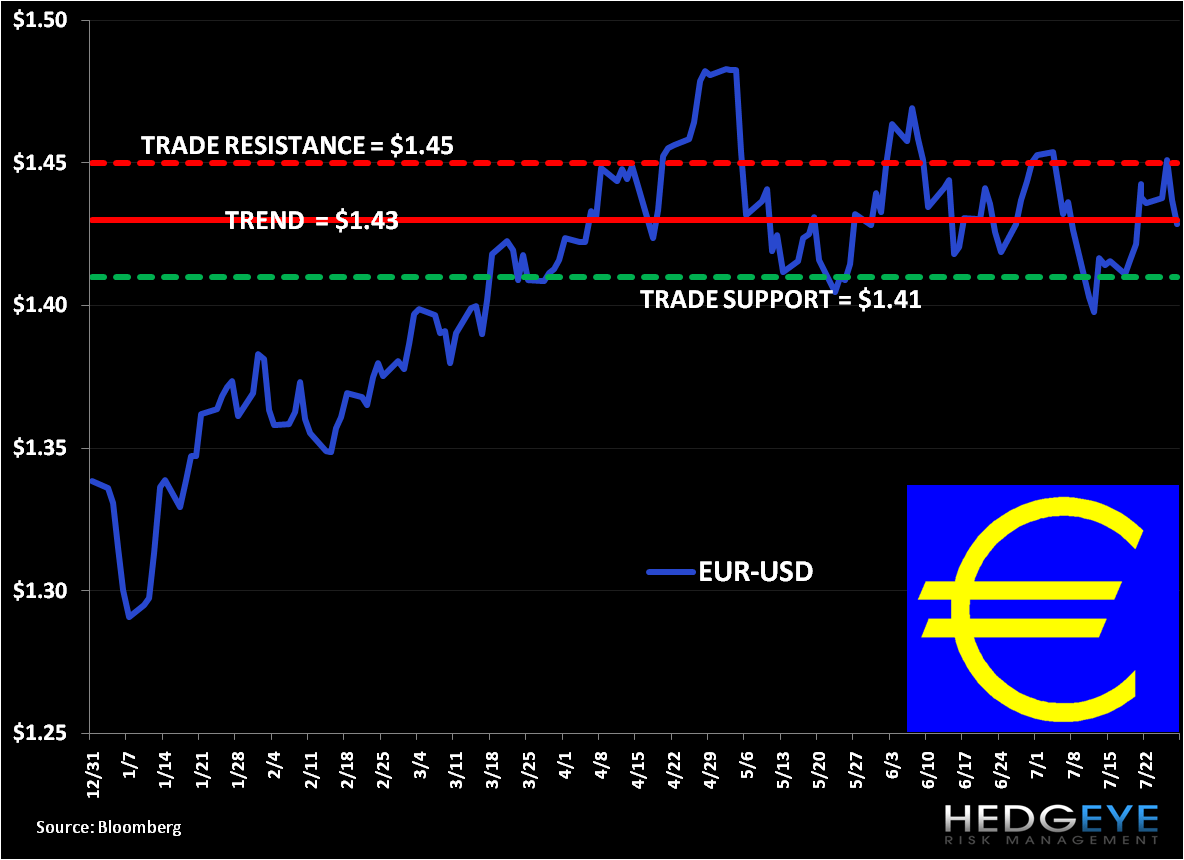

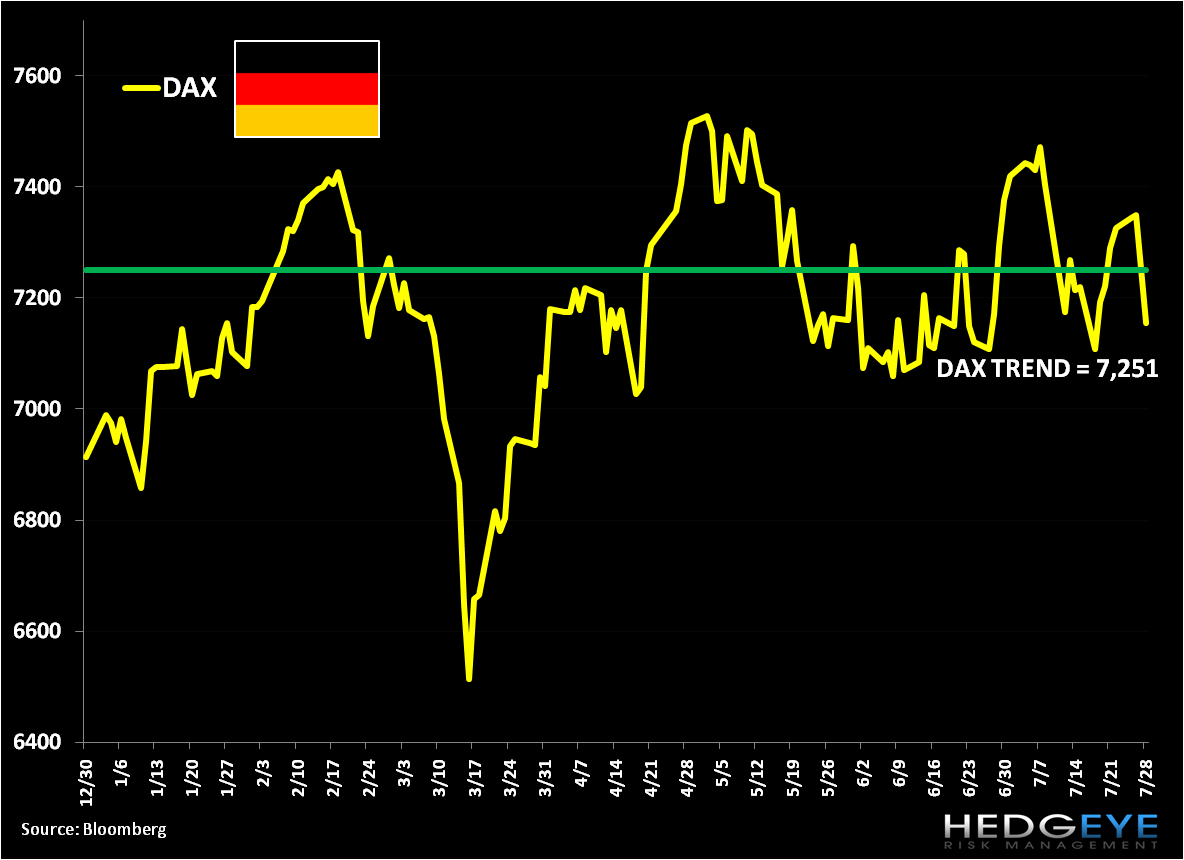

- GLOBALLY – China’s Shanghai COMP TREND line = 2831 (broken); India’s BSE Sensex TREND line = 18,578 (broken); German DAX TREND line = 7251 (broken); FTSE TREND line = 5985 (broken); SP500 TREND line = 1320 (broken); Russell2000 TREND line = 827 (broken); WTIC Oil TREND line = 103 (broken); EURUSD TREND line = $1.43 (whipping around the line)

European indices have been down for the last four days and hit lower today on declining Eurozone confidence readings and a slew of bellwethers missing earnings. We continue to think that European sovereign debt contagion will erode confidence and slow growth across the region, with no country insulated. To this point, Germany’s high frequency data has slowed in recent months with inflation bumping up marginally.

Eurozone Business Climate Indicator 0.45 JUL vs 0.95 JUN (down for 4 straight mths)

Eurozone Consumer Confidence -11.2 JUL vs -9.7 JUN

Eurozone Economic Confidence 103.2 JUL (vs expected 104.0) vs 105.4 JUN (down 5 straight mths)

Eurozone Industrial Confidence 1.1 JUL (vs expected 1.6) vs 3.5 JUN (down 4 straight mths)

Eurozone Services Confidence 7.9 JUL (vs expected 9.2) vs 10.1 JUN

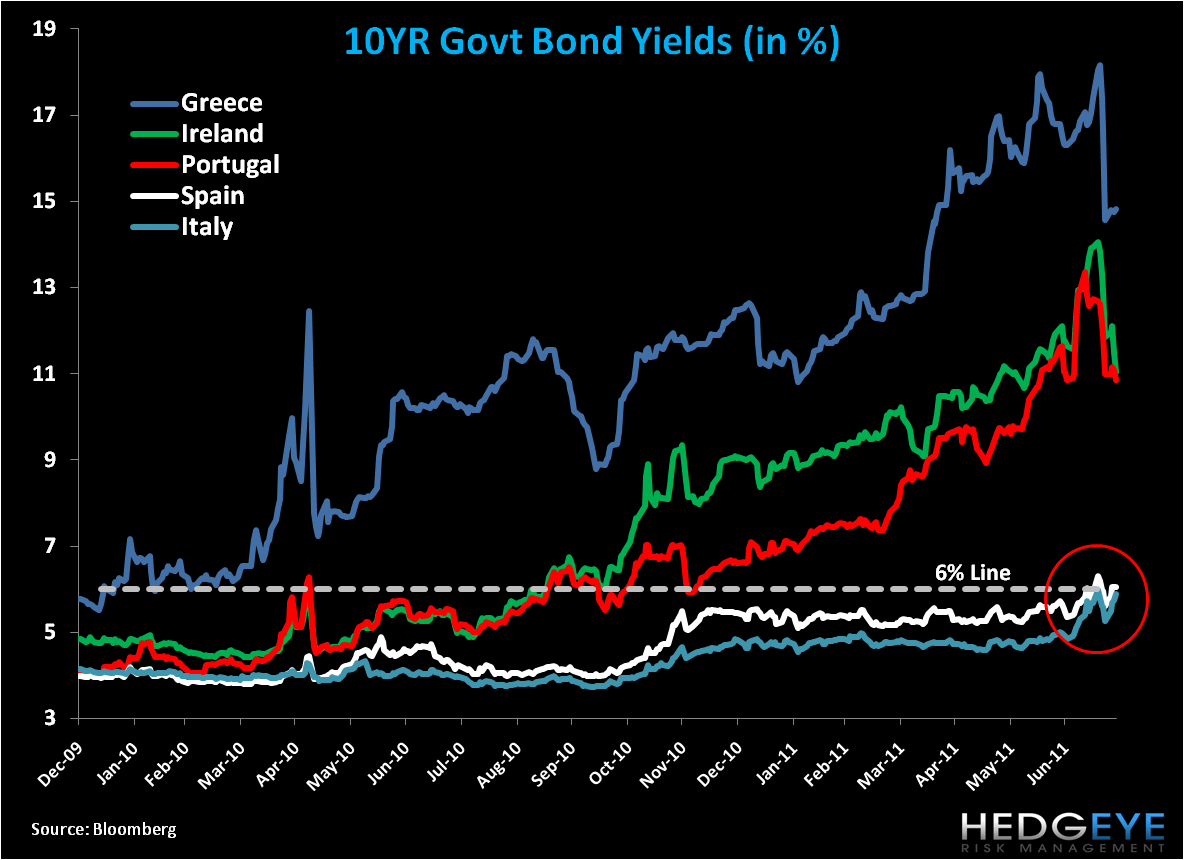

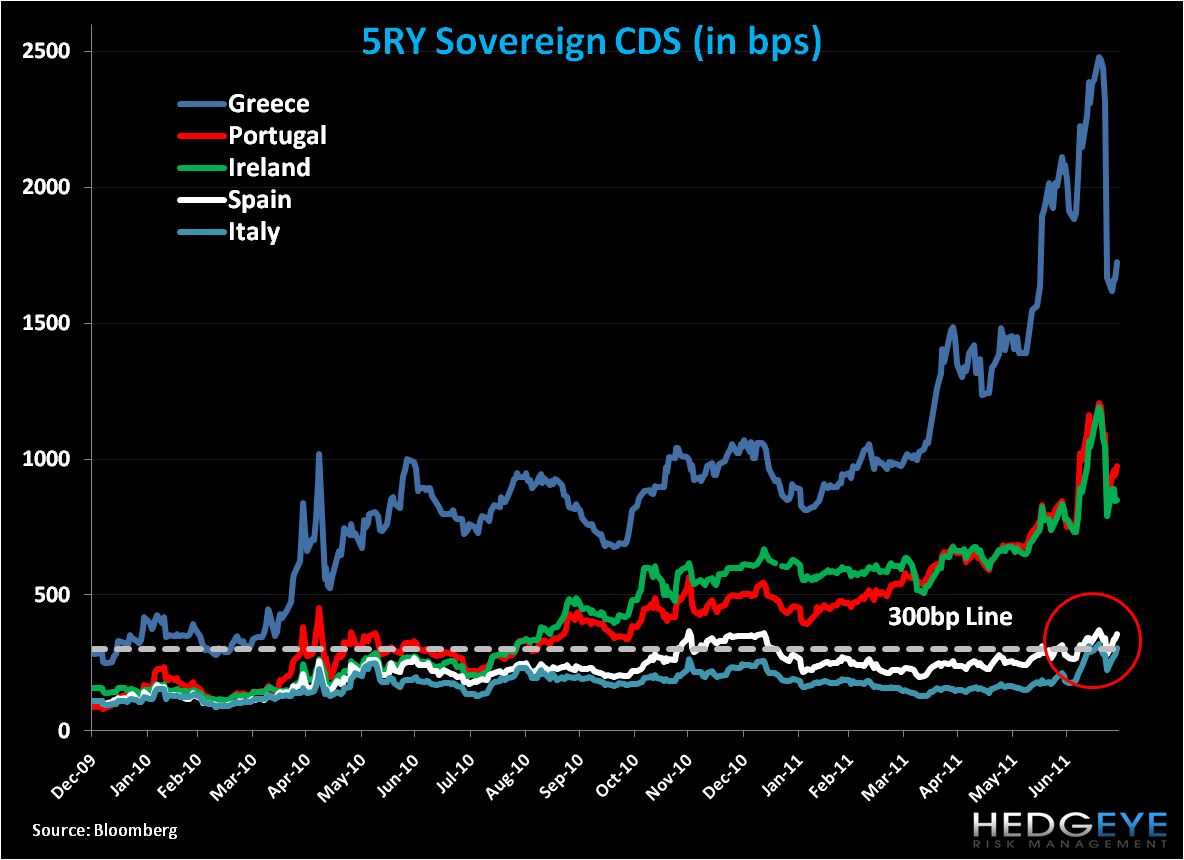

European risk, as indicated by sovereign bond yields and cds prices, has ticked up in recent days following a massive plunge after the announcement of Greece’s second bailout package on 7/21. Critically, the 10YR Spanish government bond yield is above 6%, as Italy’s flirts just below it, and CDS spreads are above the 300bp line for Spain and Italy, two critical (historic) break-out levels (see charts below). Confirming the trend of higher yields, Italy sold €2.7 billion of 10-year government bonds today at an average yield of 5.77% vs 4.94% on June 28.

Below we show our price level charts for the EUR-USD, DAX, and FTSE. The EUR-USD has held in a band between $1.40 – $1.45 since mid March, and we think has largely been supported by implicit guarantees from European officials to fund fiscally imbalanced countries with favorable short-term bailout packages, and in some cases refuse that possibility of default/exit of any Eurozone member country (Trichet and ECB).

We think Spain (IBEX) and Italy (MIB) have more room to run on the downside, despite being down -13.5% and -20.4% since intermediate term highs on 2/17, respectively. We’re currently short Italy via the etf EWI in the Hedgeye Virtual Portfolio. We covered our position in Spain (EWP) on 7/26. Germany has now broken its TREND line of support, an additional ominous sign in our models, as is the UK (FTSE) on sticky stagflation.

Matthew Hedrick

Analyst