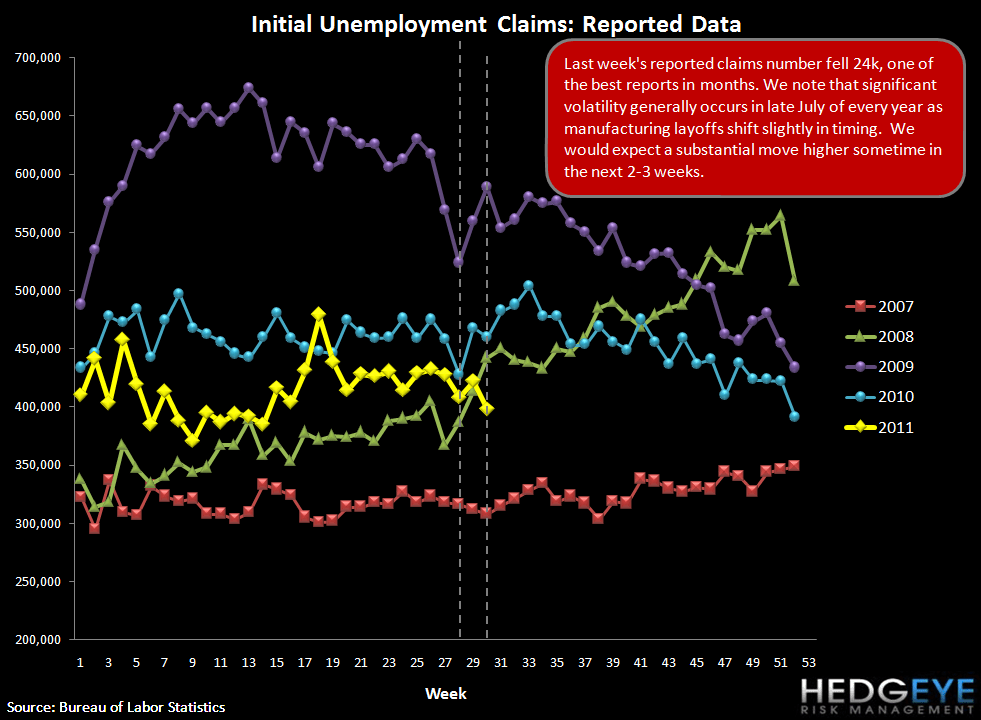

Initial Claims See Another Late July Distortion

Initial claims dropped 20k last week (24k post the revision to the prior week) to 398. Breaking through the 400k line for the first time since April is a positive signal. However, we are cautious around the timing, since late July generally sees a distortion of the seasonal adjustment related to manufacturing layoffs. Manufacturing employees are usually furloughed for a period during the summer, and submit initial claims when furloughed. However, the timing of these furloughs shifts by a couple of weeks, which means the Bureau of Labor Statistics' seasonal adjustment factor doesn't do a great job of capturing them. For evidence of this, check out the typical volatility in late July (as seen in the first chart) and the similar-looking, but not identical, patterns in the NSA data in the second chart. NSA claims dropped more than 100k WoW, well outside of the average move.

Bottom line, we would expect claims to increase back above 400-410 sometime in the next 2-3 weeks as we roll out of the seasonal distortion.

Joshua Steiner, CFA

Allison Kaptur