This note was originally published at 8am on July 25, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Plainly, MacArthur’s bleak assessment of the situation, his forecasts of doom, had been wrong.”

-David McCullough (“Truman”, page 834)

We’ve all experienced getting too bearish at bottoms. Historically, when this emotional capitulation comes from the political leaders of our country, we often look back at their Forecasts of Doom as the catalysts for change. Politics are a lagging indicator.

While I’m not sure I’d be accused of being bullish on Keynesian Economic policies or their impacts to the US Dollar since the 2008 US stock market crash, I’m certainly not the US Dollar bears’ huckleberry on this matter right here and now.

Not to name names, but PIMCO’s Mohammed El-Erian has been getting plenty of air-time in recent weeks (Barrons this weekend, Bloomberg article again this morning, etc.) talking up the credit risk in US Treasury Bonds.

Not to callout timing, but this has been El-Erian’s view since PIMCO effectively sold almost all of their US Treasury exposure in Q1 and Q2 of 2011. While I respect Bill Gross and all of his risk management accomplishments over the years, his partner’s Forecasts of Doom for the US Treasury Bond market have not only been wrong since March, but they are wrong, again, on this morning’s Debt Ceiling “news.”

The “news” on anything being commandeered by central planners of the 112thCongress is that the news is going to change. This weekend’s “news” of a Debt Ceiling debate failure may have been good for the Sunday talk show ratings, but it wasn’t bad for what matters to markets – the marked-to-market rating on US Treasury Yields.

If you didn’t know that market prices don’t lie (politicians do) – now you know. Or at least Mr. Macro Market in US Treasuries thinks he knows. Here’s this morning’s reaction to the “news” of doom:

- Short-term Treasuries (2-year yields) – didn’t move 1 basis point versus where they were priced into the end of last week (0.39%)

- Long-term Treasuries (10-year yields) – moved a whole 2 basis points versus Friday to 2.98%

But Mr. El-Erian has a Top 10 article on Bloomberg’s most read that delivers the headline “El-Erian Says US Vulnerable To Downgrade”… Qu’est ce qui se passe avec Le Analysis if the market isn’t reacting to PIMCO’s bleak assessment?

I’m long US Treasuries and have been writing about why since we launched our Q2 Macro Themes at Hedgeye in April. Sure, partly because I’m bearish on US Growth (Mr. El-Erian says he’s bearish on US Growth, but evidently not Bearish Enough or he’d be long the long-bond).

As most of the lagging of lagging indicators (Moody’s, S&P, etc) downgrade the likes of Greece (again!) this morning, I’m moving the Hedgeye Asset Allocation Model to its most invested position of 2011.

Yes, we still have 40% Cash – but that’s less than the 67% Cash we held at the end of February when Wall Street/Washington expectations for growth were will too high by about a double!

Ahead of this Friday’s preliminary US GDP Growth Report for Q2, Hedgeye’s estimate for US GDP Growth remains 1.7%-2.1%. Since the government, to a degree, makes up this number, we make up a range of expectations around current made-up numbers.

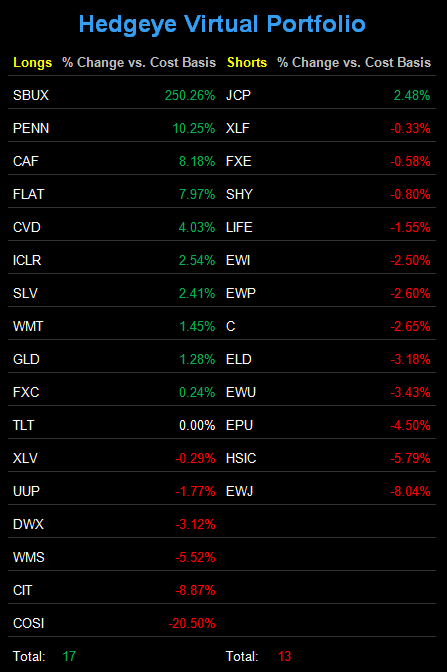

Here’s where the Hedgeye Asset Allocation Model stands as of this morning:

- Cash = 40% (down from 46% last Monday)

- Fixed Income = 24% (US Treasury Flattener and Long-term Treasuries – FLAT and TLT)

- International Equities = 12% (China and S&P International Dividend ETF – CAF and DWX)

- Commodities = 9% (Gold and Silver – GLD and SLV)

- International Currencies = 9% (US Dollar and Canadian Dollar – UUP and FXC)

- US Equities = 6% (Healthcare – XLV)

Obviously as Global Economic Growth Slows and Fiat Fool Policies whip around between Europe and the US like a ping pong ball (see our Q3 Macro Theme presentation, “Policy Pong”), we don’t want to be “fully invested” – not with our own money at least.

As for today, what we’d like to do on this “newsy” morning is sell some Gold high and buy some US Equity and Currency exposure low. We get the bleak assessment about Congress and a President who has a hard time making hard decisions. We also get that markets discount the obvious – and we could very well be looking at “news” of a Debt Ceiling resolution by the end of the week.

My immediate-term support and resistance ranges for Gold (long), Oil (no position), and the SP500 (no position) are now $1590-1619, $97.72-100.24, and 1322-1349, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer