Decent results and the MGM catalyst

After reporting what looks like a decent quarter, BYD’s stock is trading lower. The stock traded up into the quarter but once those gains are booked we expect a sharp reversal in the stock. While the quarter was not a blockbuster, it did beat our expectations, particularly in the regional markets. Importantly, BYD’s locals Las Vegas business reported YoY growth and beat our estimate so that market may have stabilized.

We think the stock could bounce significantly off of its morning lows. Anecdotally, there seems to be a lot of interest in the hedge fund community for the next big gaming idea, given the terrific moves that a lot of gaming stocks have had year to date. BYD had a good week of trading but is still lagging the big movers over the past few months. Moreover, with a likely very strong MGM quarter coming up a couple of weeks (August 8th), people will be looking for the usual derivative Strip play – exposure to the Las Vegas locals market. MGM is up over 30% in the last month alone. Watch BYD closely today.

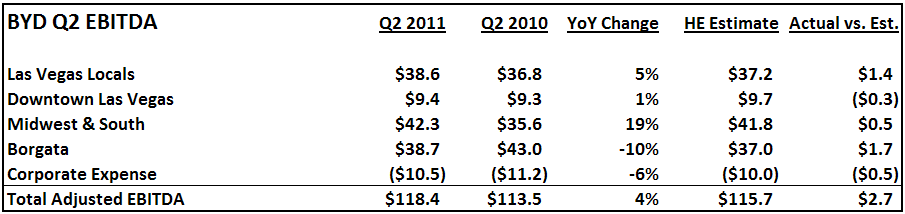

Here are the results from the quarter: