We were convinced from our analysis of KONA that the company was going to perform well through 2011 and viewed the stock favorably as a result. Over the past month KONA has been the best performing casual dining name over the past month (up 23.4%) and is now up 62% year-to-date.

Early in the quarter, there were some serious questions raised about the future following former CEO Mark Buehler's resignation. As we wrote on June 9th, the departure of the CEO was not related to weakness in the business and the 2Q financial performance confirmed our thesis.

KONA 2Q EPS came in at $0.08 or $0.11 ex-special charges. Same-restaurant sales came in at +9.1%, implying two-year average trends 180 basis points above those in 1Q11. Management also provided some conservative sales guidance for the upcoming quarter. Guidance is for 6% same-restaurant sales in the third quarter, including 3% price. This comp guidance, implies two-year average trends of 3%. This would be a sequential slowdown from the two-year average trend in 2Q but it would likely bolster investor confidence in the company’s ability to continue to grow share. The 3Q trends suggest that the company will post positive SSS for seven straight quarters. Currently KONA is running about 2.2% in pricing; the company took about 150 basis points in June to help offset higher commodity costs.

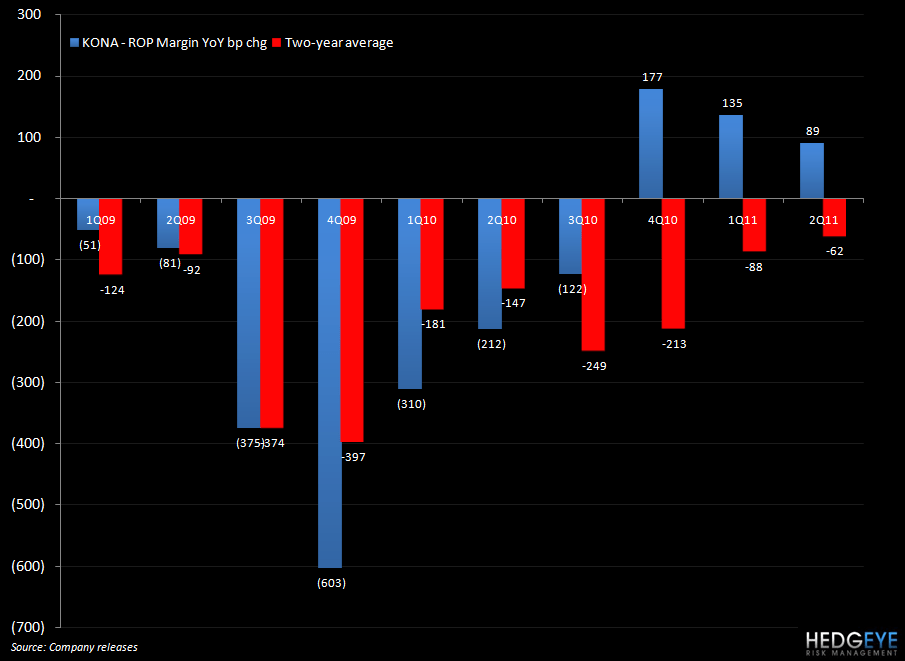

Restaurant level margins also increased year-over-year during 2Q11to 17.2% versus to 16.3% last year. On a sequential basis, restaurant operating profit improved 320 basis points over 1Q11.

We continue to like the KONA story.

Howard Penney

Managing Director

Rory Green

Analyst