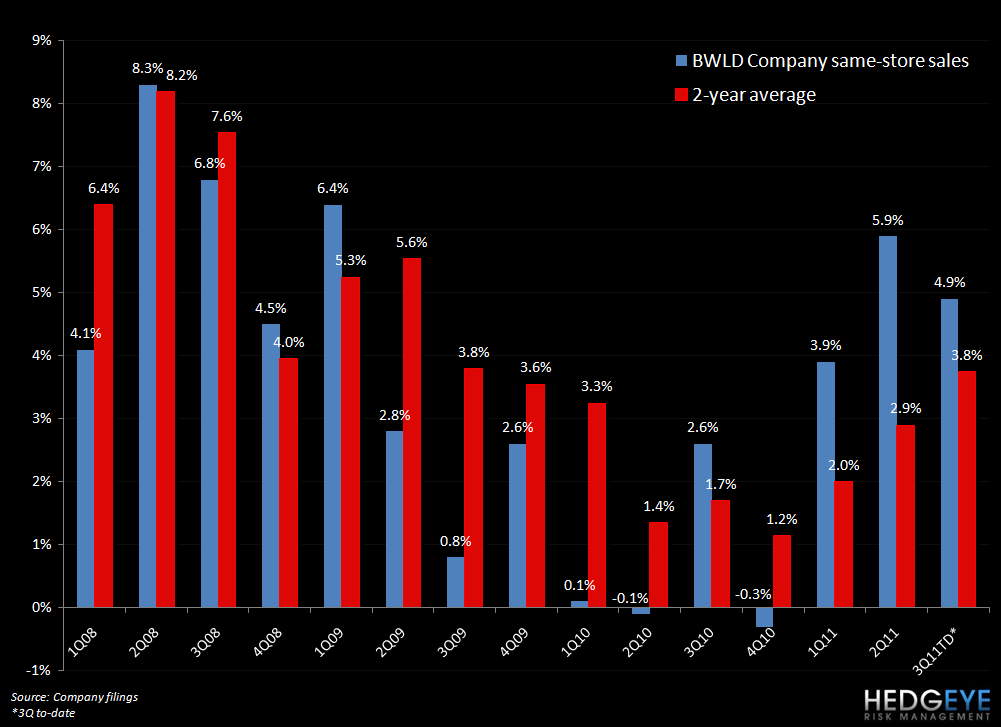

BWLD reported earnings after the close and EPS came in below expectations at $0.58 versus $0.60. Comps, however, blew away consensus with company comps gaining 5.9% year-over-year versus consensus +3.6%. Franchise comps, too exceeded expectations at +2.7% versus +1.6%.

Below are our Top Ten Takeaways from the quarter:

- The same-restaurant sales trends are a huge positive for BWLD. Despite the earnings miss, which is impacting the after-hour trading, people are coming through the door and the resolution of the NFL lockout dispute is another positive for the second half of the year besides the obvious appeal consumers have for the brand.

- Strong comps are likely to continue, in our view, as the football season gets underway and the company increases its media presence in the third and fourth quarter. The company gave the to-date 3Q number as 4.9% which, if it were the reported 3Q comp, would imply a further 90 basis point acceleration in two-year average trends from the 2Q number.

- The company is not taking price, aside from a nominal 10 or 20 basis point increase with the new menu in September, in the near future. Thanks to benign chicken wing prices, the company can afford to let price roll off the menu.

- Chicken wing costs, the most important commodity for BWLD, continue to be favorable in the third quarter. For the first two months of the third quarter, wing costs are averaging around $1.14 per pound versus $1.42 during the third quarter of 2010.

- Operating margin came in lower than expected largely due to higher preopening expense and G&A expense. Some of the increase in G&A was due to higher recruiting and training costs for restaurants opening in the new West Coast market. This is because the new markets do not have the training centers and number of existing personnel required to train new hires. Preopening expenses are also up as unit growth continues at a fast pace.

- Restaurant operating margin, a more pure assessment of restaurant performance in our view, increased year-over-year. Food, operating, and occupancy costs were favorable while labor costs were up slightly year-over-year as higher labor costs were incurred in new markets.

- The company’s earnings power is strong. Despite EPS coming in below expectations, largely because of increased G&A and preopening expense, net earnings growth in the first six months of 2011 was over 29%. The company has raised its expected annual net earnings goal for the year from 18% to “more than 20%” as a result of the strong performance.

- New unit growth is set to continue to contribute to returns but will also keep G&A and preopening expenses elevated. The cost of training people in new markets where there is a lack of training centers is higher than training people in new markets. In the second half of the year management is guiding to 29 company store openings, 37 franchisee openings and 3 in Canada. As long as new unit volumes remain strong, we believe that the cost of growth is worth the price for shareholders. Management calls the expenses, “investments in our future”.

- As the company is opening new stores and expanding into new markets, it is also closing older, lower volume locations. We believe that this is positive for the company in the intermediate-to-long tem despite the immediate term increase in costs associated with the closures.

- Continued innovation in the product and sports-related promotions are likely going to support traffic going forward into 2H11. The lack of a significant price increase, when other restaurant chains are likely going to have to raise prices somewhat, could also help as customers continue to seek value.

Howard Penney

Managing Director

Rory Green

Analyst