2Q results were further confirmation that Domino’s continues to lead the Pizza category. Below is a quick recap and our most important takeaways from the call.

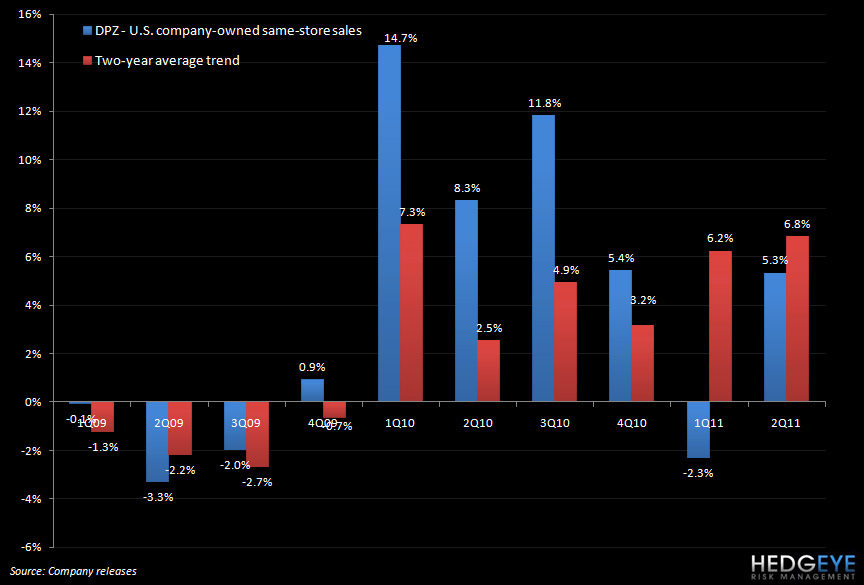

Domino’s Pizza reported very strong 2Q results and is trading sharply higher today, as it should be. EPS of $0.40 cents beat expectations of $0.36 with solid margin improvements on the labor and occupancy lines, offset by higher food costs (cheese and meats). Domestic Company-owned same-store sales grew 5.3% in the second quarter versus a difficult +8.3% compare from 2Q10. This implies a sequential acceleration in two-year average trends of 60 basis points. Consensus was looking for +3.2%. International same-store sales grew 7.4% versus expectations of 6.1%.

Top Ten Takeaways from the 2Q11 earnings call:

- DPZ continues to take share, printing industry-leading same-store sales numbers. This quarter was particularly impressive in that domestic company-owned same-store sales increased on a one- and two-year basis. Management said that this was driven more by increased customer loyalty and improved retention than new customers.

- The company is innovating to stay ahead of the competition on the top-line by continuing to support its revenue line with investment in innovation, such as the new iPhone App, and promotions.

- The company’s stance on pricing remains cautious; a new promotion was launched yesterday which offers a large pizza with two toppings for $5.99. Where the company may take pricing, is in coupons.

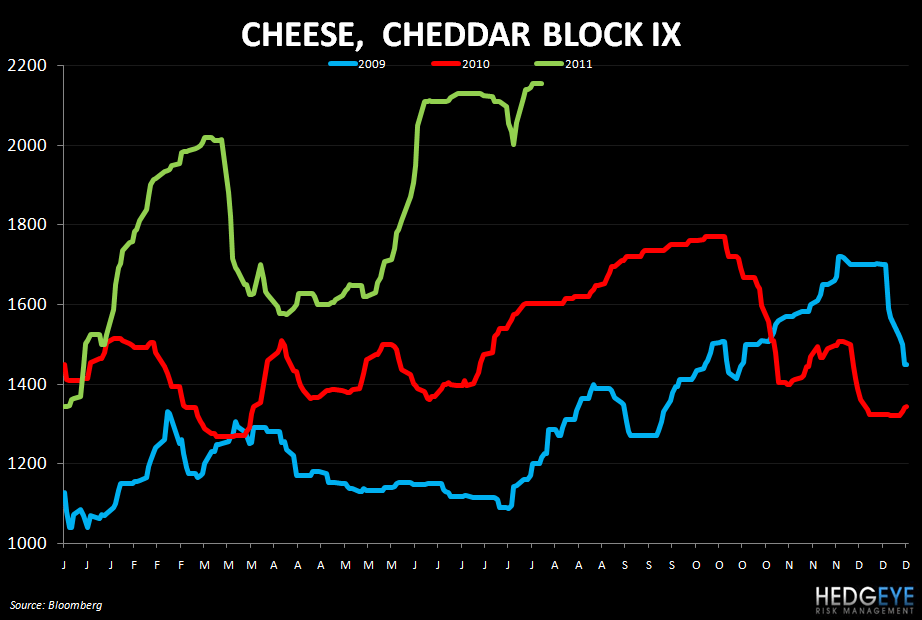

- DPZ raised its commodity basket inflation forecast for 2011 to 4.5%-6% from 3%-5%.

- The price of cheese remains the greatest variable. 2Q brought average per block prices of $1.68 for DPZ, far in excess of what it had expected after the 1Q earnings call. Management has a contract for cheese that eliminates one third of the volatility of the spot price. In the back half of the year, management sees cheese prices “easing off” and finishing below $2 before the end of the year. We would not be so sure; while a cheddar cheese recall did impact prices, demand has kept prices elevated – as management alluded to – and we think the decline in prices could be more gradual than management is implying.

- The company is locked on chicken, locked on wheat into next year, locked on cheese but only eliminating one third of volatility, has some conversion agreements on meat but there is also exposure there.

- The company’s international markets are a big strength with comps in the high-single digits and the company has now had 17.5 years of positive same-store sales comps in international markets. The company is growing at a very fast pace in international markets, emboldened by the strong performance across a broad base of markets, and will see some increase in G&A associated with supporting the infrastructure required to support this growth. Mexico, which had been lagging over the past 18-24 months, has now picked up.

- Overall, the pizza category is not “strong” but Domino’s is taking share from regional pizza players but the company doesn’t see any interaction between its pizza and the frozen pizza category.

- Third quarter comps will likely not be as strong as the company laps a more difficult 3Q comparison that was boosted by advertising.

- The company’s share repurchase authorization has been increased to $200 million by the board of directors. In the second quarter, the company retired approximately 1.75 million shares of common stock for a cost of $41.4 million at an average price of $23.71 per share.

Howard Penney

Managing Director

Rory Green

Analyst