This note was originally published at 8am on July 21, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“There is an invisible tipping point. When we get there, it’s far too late.”

-Seth Klarman

I’ve used this quote from Baupost Group Chief, Seth Klarman, before. When he said it, he was alluding to America. In Europe, I think we’re there. Some Tipping Points are invisible to many, but crystal clear to Mr. Macro Market. You just have to be humble enough to let him show you the way.

For all of you who got this right in 2008, you know exactly what I am talking about. The interconnectedness of Global Macro markets has been clear to you for quite some time now. Considering your portfolio risk from the narrow vantage point of one country and its credit risk is as obsolete as Keynesian Economics.

This systemic problem in our industry’s analytics was born in academia and now it thrives in government. These central planners of the world unite and focus on “risks” after they have been priced in. In doing so, they are blinded by what’s coming next.

Consider the #1 headline on Bloomberg this morning:

“MERKEL, SARKOZY TO OUTLINE POSITION ON GREEK DEBT.”

Gee, thanks.

Meanwhile, as these left leaning Europeans prepare for their 3 hour lunch in Brussels, the rest of the world’s interconnected risk continues to be priced on a tick.

From a Chaos Theorists perspective (an alternative to Keynesian dogma), the deepest simplicity that I can achieve in explaining how this works is watching every grain of sand (market data points - including Price, Volume, and Volatility signals) fall onto my screens – one by one. Unless you have a process to contextualize Tipping Points, how will you know which grain of sand will collapse the pile?

Hedgeye doesn’t have its feet on the floor earlier than any other firm we compete with for bailouts and giggles. We do it because someone needs to be awake every morning, watching the grains of sand.

This morning’s moves in Global Macro are a critical example of what I am ultimately trying to signal – timing:

- Intel (US equity market barometer) flags that margins are peaking last night at the close = US FUTURES DOWN

- China comes out with a brutal manufacturing PMI print of 48.8 in July (versus 50.1 in June) = ASIA DOWN

- Germany then hits the tape with an equally bad PMI print (versus expectations as China’s) = DAX DOWN

There’s obviously a lot of other things going on out there, but the principles of Chaos or Complexity Theory hinge on simplifying what factors have the largest impacts to the ecosystem you are analyzing. US Tech, China, and Germany are large factors.

There’s a difference between correlation and causality. The fundamental slowing of economic growth, globally, is causal to markets and the companies that operate within them. Whereas measuring the correlation between these Global Macro data points and market prices is trivial – if you have a process to absorb them:

- US Equities are going to re-test intermediate-term TREND line support (1319 SP500) this morning

- Chinese Equities had their biggest down day in 3 weeks, closing down -1% at 2765 on the Shanghai Composite

- German Equities are breaking their intermediate-term TREND line of 7198 on the DAX

What do any of these things have to do with Greece?

Exactly. Nothing. Greece is gone. Caput. Gonzo. Au-revoir.

Greek equities have crashed, twice, in the last 2 years and the Greek bond market is illiquid and dark. Europig politicians are not going to be able to do a damn thing to save Greece from themselves. Default and/or restructuring is the only way out.

So they may as well move to the crème brule in Brussels today and focus on what really matters to both the EU and the Euro – Germany’s economic slowdown and Spain/Italy bumping up against massive debt maturities in August and September (it’s July). Focusing on Greece today is far too late.

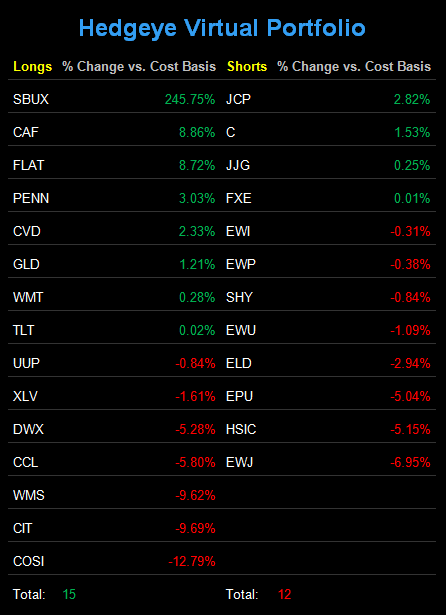

My immediate-term support and resistance ranges for Gold (we’re long), Oil (no position), and the SP500 are now $1572-1623, $95.47-99.08, and 1319-1341, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer