THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - July 26, 2011

Instead of making a decision, Obama reverts to the fear-mongering last night. The US Dollar falls. Treasuries move a beep. UK reports another stinky stagflation number – and upward and onward we go with our risk management day. As we look at today’s set up for the S&P 500, the range is 27 points or -0.93% downside to 1325 and 1.09% upside to 1352.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1809 (-1704)

- VOLUME: NYSE 763.67 (+3.44%)

- VIX: 17.52 -0.23% YTD PERFORMANCE: -1.30%

- SPX PUT/CALL RATIO: 1.58 from 1.16 (-35.41%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 20.63

- 3-MONTH T-BILL YIELD: 0.05%

- 10-Year: 3.03 from 2.99

- YIELD CURVE: 2.61 from 2.59

MACRO DATA POINTS:

- 7:45 a.m./8:55 a.m.: Retail weekly sales from ICSC/Redbook

- 9 a.m.: S&P/CaseShiller 20 City MoM% est. 0.0%, prior 0.09%

- 10 a.m.: Consumer Confidence, est. 56.0, prior 58.5

- 10 a.m.: Richmond Fed Manufacturing, Jul, est. 5, prior 3

- 10 a.m.: New Home Sales, Jun, est. 320k (up 0.3%) from 319k

- 11:30 a.m.: U.S. to sell $18b 4-wk, $20b 52-wk bills

- 1 p.m.: U.S. to auction $35b 2-yr notes

- 2 p.m.: Fed’s Hoenig testifies on monetary policy

WHAT TO WATCH:

- The dollar sank to a record low versus the Swiss franc and Treasuries fell amid little signs of progress to resolve U.S. debt talks

- Dunkin Brands prices IPO after the close

- IMF chief Lagarde addresses Council on Foreign Relations

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Drought Withers Smallest Hay Crop in Century to Boost Beef Costs

- Gold May Decline After Rally to Record Amid U.S. Debt Stalemate

- Sugar Rises on Speculation Supplies Are Limited; Coffee Advances

- Japan Corn Cargoes at Quarter-Century Low: Freight Markets

- Morgan Stanley Raises Gold, Silver Targets Through to 2016

- Gold Miners in South Africa to Join Strikes Hurting BHP, Anglo

- Oil Supplies Decline for Eighth Week in Survey: Energy Markets

- Grain Volatility to Stay on Low Stockpiles, Surging Demand

- Global Natural-Rubber Demand May Grow 3.8%, Palanivel Forecasts

- Cows-for-Bride Inflation Spurs Cattle Theft in South Sudan

- Rice Husks Follow Solar to Power Indian Towns Off Utility Grid

- Rice, Sugar-Cane Crops to Benefit From ‘Good’ India Monsoon Rain

- India May Consider Additional Sugar Exports After September

- Japan to Recall Tainted Beef as Cesium Contamination Widens

CURRENCIES

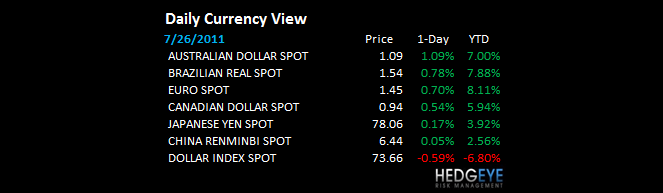

- USD – the only good news here is that the USD is still making higher-lows; the bad news is that America has an opportunity to seize the moment and can’t, yet. The intermediate-term TREND line for the USD Index is $74.79 and needs to be recovered.

- EURO – finally trades above Hedgeye's 1.43 line of intermediate-term TREND resistance, but can it hold? We’ll give this through August 2nd to make sure to not get sucked into a head-fake. We think Europe’s issues are much more severe than America’s for next 3 months.

EUROPEAN MARKETS

- EUROPE: stinky stagflation in the UK and big time failures in Spain/Italy/Greece to recover TREND lines (all bearish) with Finland following

- SPAIN: Spanish stocks down small this morning, but the breakdown yesterday is what mattered. We have immediate-term TRADE downside in the IBEX to 9215 – that’s -6.5% lower and what our models consider probable.

ASIAN MARKETS

- ASIA: rock solid recovery day across the board in Asia with every major market up but India who rightly raised rates to quash inflation pressure

MIDDLE EAST

Howard Penney

Managing Director