THE HEDGEYE BREAKFAST MENU

Notable news items and price action from the restaurant space as well as our fundamental view on select names.

MACRO

Casual Dining

Malcolm Knapp released the Knapp Track Casual Dining data for June over the weekend. Another strong month, as the estimated comparable restaurant sales change in June 2011 is 2.4% and traffic increased 0.5%. I suspect that the strong performance of Red Lobster is helped to drive the 40 basis points sequential improvement from May to June.

Commodities

In terms of commodity news, corn and soybeans may rise as the hot weather of last week threatens yields. The Japanese Food Chain is being impacted by a radiation fallout from the Fukushima nuclear plant as unsafe levels of cesium have been found in beef in supermarket shelves and in vegetables and in the ocean.

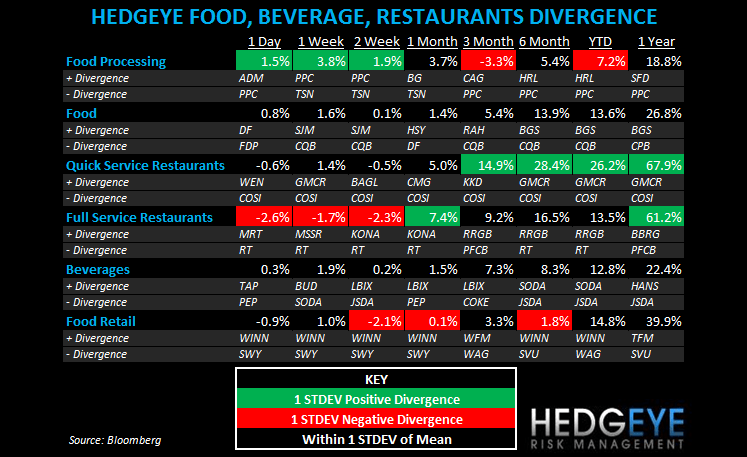

Subsectors

Bucking a trend that has been in place for the last 6 months or so, food processing stocks outperformed over the last couple of months. Full service restaurants lagged their food, beverage, and restaurant peers over the same duration.

QUICK SERVICE

- DPZ UK and Ireland SSS increased +2.4%; UK increased +3.4%; Republic of Ireland (8.4%). Management is confident the company will see SSS growth in the next 26 weeks; marketing spend will be three times the amount versus last year, combined with new products. DPZ is set to report global results for 2Q tomorrow.

- PNRA has been reiterated Buy, with a Price Target of $134, by Sterne Agee.

- TAST, MCD, and CMG gained on Friday on accelerating volume. COSI declined 7.4% on accelerating volume.

FULL SERVICE

- RT reported a disastrous quarter last week and its share price declined -14% on accelerating volume. BJRI also declined on accelerating volume.

- EAT gained on accelerating volume despite the nosedive in RT’s stock. This also confirms out view that EAT is taking share from RT.

Howard Penney

Managing Director

Rory Green

Analyst