This note was originally published at 8am on July 20, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“I like them more than all of the top-notchers.”

-Harry Truman

I smiled last night as I was reading that passage on page 808 of what my son calls the “heavy book” – David McCullough’s “Truman”:

“He liked the Secret Service agents who watched over him, most of whom came from small towns or backgrounds much like his own and none of whom ever asked anything of him. “I like them more than all of the top-notchers,” he once told Margaret.”

Harry Truman, like all of us, had his issues – but, ultimately, he was victorious in what most of us want to accomplish in life. He achieved above and beyond what anyone ever expected of him.

Markets, too, are like that. They are all about expectations. I think that’s why they resonate with so many of us. They can make you laugh. They can make you cry. And, every once in a while, they can put a sparkle in your eye.

Apple did that last night. The proverbial love-affair Americans have had with this stock extends itself from the product all the way back to the man who bet on himself to create it. Steve Jobs is another great American success story who has travelled the broken road of expectations to infinity and beyond.

With a Debt-Ceiling Compromise finally appearing in the rear-view mirror, Americans have a great opportunity to move forward today. No matter what you think about Steve Jobs or the Global Market – I can assure you of this on both - they are looking forward. And they will both leave those who are caught up in yesterday behind.

Back to the Global Macro Grind…

1. ASIA - surprisingly Asian stocks had a mixed reaction to Debt Ceiling Compromise and the Apple news. Both China and India closed down overnight (-0.1% and -0.8%, respectively), while Korea, Australia, and Japan all closed up over +1%. China and India in particular did not like the food and energy inflation that was marked-to-market yesterday. So keep your eye on that.

2. EUROPE - wet Kleenex reaction to American earnings and Italian Equities in particular look very vulnerable if the MIB Index fails to overcome the 19,559 line in the very immediate-term. We don’t think that there is any irony in the timing of $12.4B in Italian CDS that traded last wk (2x that of the next country in terms of notional size - France). Sovereign Debt maturities for both Italy and Spain are going to be huge in August and September - and the EUR/USD remains bearish/broken below my $1.43 TREND line.

3. USA – S&P futures look as good as they should look with Apple taking over from the Bankers of America and changing the tone of the earning season to something the winners in this world can believe in. The idea is to think, re-think, and evolve; not suck compensation from a Europig’s nipple of a socialized banking system. That’s all I have to say about that.

In terms of risk management levels in the US, as usual, I think you need to take the Apple out of your eye and focus on being multi-factor and multi-duration. That means Stock, Bond, and Currency market moves altogether:

1. STOCKS – what was our intermediate-term TREND line resistance in the SP500 at 1319 is now support. For the immediate-term TRADE (different duration) that’s bullish and should support a new Risk Ranger range for the SP500 of 1319-1352. From a long-term TAIL perspective, my topside target for the SP500 in 2011 remains 1377.

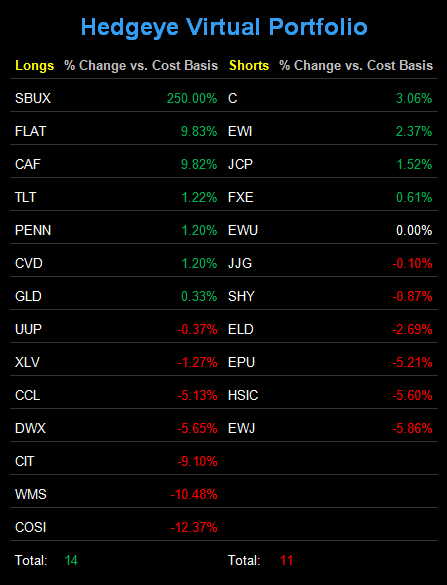

2. BONDS – on our Q3 Macro Themes conference call last week, and really since April, we’ve been saying that A) a Debt-Ceiling Compromise will get done and B) that’s very bullish for US Treasuries. Why? It takes out some of the shorts that are either trading on lagging indicators (Moodys and S&P ratings fears) or short UST bonds on US credit risk. We are long both long-term Treasuries (TLT) and a US Treasury Flattener (FLAT) as we think the long-end of the bond market will continue to see yields fall.

3. CURRENCY – in a strong US Dollar can Americans trust? I guess that depends on which constituency of Americans you ask. I think well over 90% of us say yes (lower gas prices, Deflating The Inflation, and higher employment correlate with a strong US currency). The other 5-10% of you who want to Debauch The Dollar can’t possibly want that for your country in the long-run – you probably want it for yourself.

Whether it’s some Top-Notcher in Washington or a lobbyist trying to convince a professional politician of another policy to inflate, Americans have had enough. They get it. They are America’s “Secret Service.” From small towns to big ideas and sweat capital to big hiring, they are The People who make this country work.

My immediate-term support and resistance ranges for Gold (we’re long), Oil (we covered our short on Monday), and the SP500 are now $1572-1623, $95.51-99.20, and 1319-1352, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer