MCD is looking as good as the weather is hot today following extremely strong earnings that came in far above the street, and our, expectations. The crux of our negative thesis on MCD at the outset of 2011 was based around the difficulty I foresaw for MCD to “comp the comps” versus the company’s resounding success in driving same-restaurant sales in the U.S. during summer 2010. Following the release of April sales results, we “cried uncle” as the facts changed and sales continued to accelerate.

Having seen the June results, it is clear that MCD is “comping” the comps this summer and management was eager to point out that July global same-restaurant sales are expected to be between 4-5%. Below we offer ten takeaways and a quick recap of the sales trends by region and the markets/factors driving each.

Our ten takeaways from the quarter are as follows:

- MCD US is the most important division for the company from an operating income perspective and the acceleration of same-restaurant sales in June and, as guided to, in July versus extremely difficult compares from 2010 means that MCD is successfully driving traffic through its beverage initiative. Total McCafé beverage sales grew 29% y/y in the second quarter.

- On a global basis, higher commodity and, to a lesser extent, labor and occupancy costs are being offset by positive same-restaurant sales. In China, margins are being negatively impacted by the acceleration of new restaurant openings. New restaurants typically open with lower margins and then accelerate over time.

- MCD is taking share from other QSR companies. TAST’s report of their Burger King restaurants seeing same-restaurant sales decline -5.2% in 2Q is testament to that. Companies that fail to keep up with MCD reimaging and product initiatives are likely to continue to lose market share. The reimaging program in the US will be implemented at 600 restaurants in the US by year-end (200 done as of 1H11).

- The hot weather is driving people in the US to buy beverages. This is a positive for SBUX, SONC and other brands positioned to take advantage. Beverages are driving traffic and are margin-accretive.

- The full-year outlook for the company’s U.S. grocery basket is unchanged at 4%-4.5%. As food at home CPI continues to outstrip food away from home CPI, which gives the company some confidence in taking pricing in the current environment.

- Our pre-earnings assertion that top-line is all that matters this quarter seems to be correct. Companies have made their operations far more efficient than before the recession and, despite margins declining at company-operated stores in the US from 22.2% in 2Q10 to 20.7% in 2Q11, the health of the top line is what investors are focused on.

- China still only represents 3% of global MCD profit. MCD is growing rapidly in China, but the overall pie is growing also. This is not something YUM is seeing – YUM’s US business has already shrunk to 25% of the company’s total operating profit, previously a 2015 target.

- China 2Q comps were up 14.4%, the brand clearly has relevance and there seems to be enough room for MCD and YUM, which also produced double-digit comps in China during 2Q. For MCD, breakfast is approaching 8% of sales in China.

- The company is growing aggressively in APMEA, and China in particular with 175-200 openings in China projected for the year.

- Momentum is strong heading through 3Q with July global comps expected to come in at 4-5%.

U.S.

Drivers: Frozen Strawberry Lemonade, classic core offerings including Chicken McNuggets and the Big Mac, and breakfast supported by the new Fruit & Maple Oatmeal.

Europe

Strong markets: France, UK, Russia.

Drivers: Ongoing restaurant modernization efforts, focus on premium menu offerings.

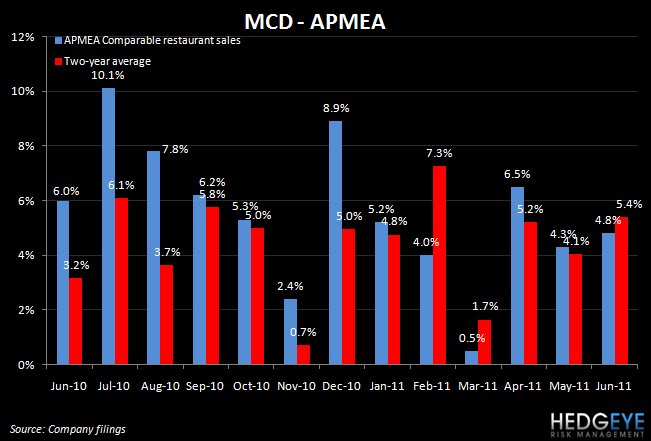

APMEA

Strong markets: China and most other markets.

Drivers: Affordability, drive-thru, delivery and extended hours. Breakfast is offering a lot of growth in China and, despite the sluggish economic growth, Australia.

Howard Penney

Managing Director

Rory Green

Analyst