Positions in Europe: Short Italy (EWI); EUR-USD (FXE); Spain (EWP); UK (EWU)

Keith’s taking the opportunity to re-short strength in European equities [Italy (EWI) and Spain (EWP)] and the EUR-USD (FXE) in the Hedgeye Virtual Portfolio this AM as the positions run ahead of themselves on optimism about “positive” bailout talks on Greece today at the EU Summit in Brussels.

As we’ve said in multiple research pieces recently (for more, see our portal at Hedgeye.com), we see a long road ahead in Europe’s sovereign debt soap opera as European officials choose to issue short term solutions (band-aids) to much longer term fiscal imbalances.

Should anything come of today’s talks regarding new concessions for Greece’s outsized debt—and at this point everyone is running on pure speculation—we believe the news will at best provide only a short term boost to capital market performance, particularly for the peripherally countries. Bottom line, we’re shorting today’s bounce (Italy’s MIB is trading up +4% intraday and Spain’s IBEX is up +3%) and the EUR-USD cross broke out above our TREND Line of $1.43 (+1.2%).

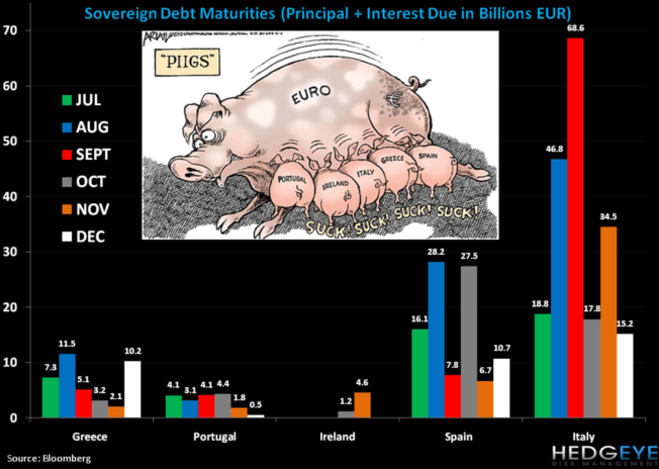

One chart in particular that is worrying us is the coming debt maturities for Italy and Spain over the next 2-3 months.

Our intermediate term TREND levels on European equity indices are not just breaking across the PIIGS, but also teetering around breakdown in Germany (DAX TREND = 7198) and broken in the UK (FTSE TREND = 5925), driven and confirmed by slower high frequency data (Services and Manufacturing PMI figures all slowed in July for Germany, France and Eurozone ave.) and pressing threats of contagion (especially as Italy and Spain push to the forefront) that even fiscally sober countries like Germany and Sweden are not immune to.

Matthew Hedrick

Analyst