MCD will announce sales, along with 2Q11 results, before the market open on Friday, July 22nd.

Recapping the quarter to date, we know April was a strong month beating expectations globally. May on the other hand was not a very strong month for MCD sales. Global comps came in at +3.1% versus expectations of +3.6%, U.S. comps were +2.4% versus consensus at +2.9%, Europe comps missed by a wide margin, coming in at 2.3% versus 3.8% expectations. APMEA was the only division where comps beat consensus, coming in at +4.3% versus 4% expectations.

Compared to June 2010, July 2011 had one less Tuesday and one additional Thursday. As a result, I would not anticipate any major calendar shift. In my recap of the May sales results, I highlighted that there were several changes in the May press release from the April sales release. Firstly, McCafe was not mentioned as a driver of comps in May but it was in April. Frozen Strawberry Lemonade was highlighted but, as I stated last month, this product is drawing customers due to its low price point. I remain skeptical of MCD’s focus on “beverages over burgers.”

Consensus estimates have risen by 0.6% over the past three months, while the sell side still has a slightly bullish bias with 59.2% of analysts holding a “Buy” rating on the stock. Interestingly, the short interest has risen steadily during the quarter, but still at very low levels.

My model is coming up with $1.27 for 2Q11 versus the Bloomberg mean estimate of $1.28. Naturally, my estimate is slightly lower that the street due to a more conservative revenues estimate. The big variable this quarter will be food cost and the impact on margins. I’m currently modeling a 100 bps increase in food costs versus 70bps in 1Q11. Without a big June comp figure, it’s hard to get significant upside absent any “one-time” items.

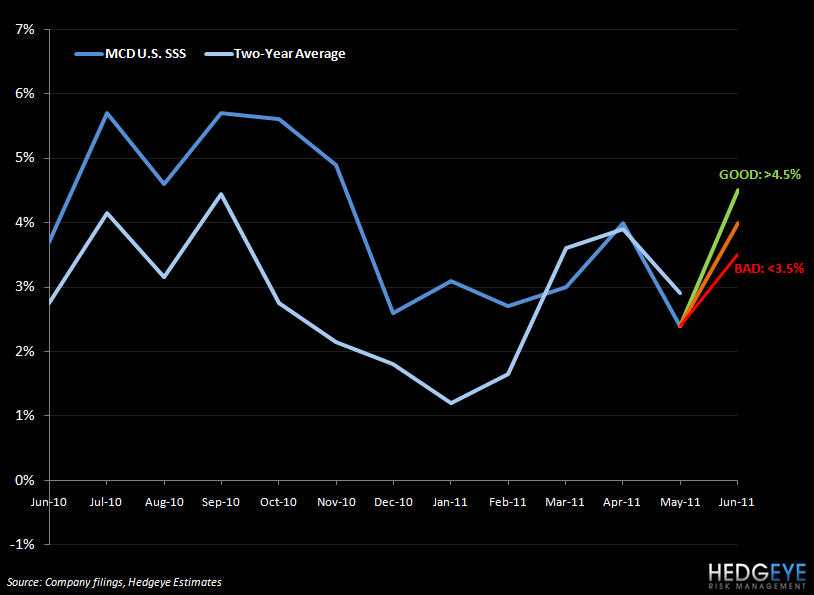

Below I go through my take on what numbers will be received by investors as GOOD, BAD, and NEUTRAL, for MCD comps by region. For comparison purposes, I have adjusted for historical calendar and trading day impacts.

U.S. - facing a compare of +3.7% (including a calendar shift which impacted results by +0.0% to +0.3%, varying by area of the world). Frozen Strawberry Lemonade was launched in May, comparing with the official national rollout of Frappes in May 2010. May 2011 results came in lighter than expected. The June compare is slightly more difficult but I am not anticipating any large miss this month. Expectations have risen to a level that implies that MCD is “comping the comps” in June and July - something I did not think possible in January.

GOOD: A print above 4.5% would be received as a good result, implying two-year average trends roughly 20 basis points above those seen in May. Despite missing consensus, on a calendar-adjusted basis May results implied a sequential acceleration in two-year average trends of 75 basis points. It will be interesting to see what drives the comp in June but, given the focus on beverages and the difficult compare in July fast approaching, I would expect the bulls to be focused on this.

NEUTRAL: A print between 3.5% and 4.5% would be received as a neutral result by investors given that the mid-point of this range implies two-year average trends, on a calendar-adjusted basis, in line with trends in May.

BAD: Same-restaurant sales below 3.5% would imply a sequential slowdown in two-year average trends raise significant doubt about the ability of MCD to match last year’s impressive top-line performance.

EUROPE - facing a compare of +4.7% (including a calendar shift which impacted results by +0.0% to +0.3%, varying by area of the world). Europe was a huge disappointment in May and, as the media has been highlighting constantly, the crisis in Europe has been gathering speed.

GOOD: A print of 6% or higher would be received as a good result for Europe as it would imply a sequential acceleration in two-year average trends after for consecutive months of declines (calendar-adjusted basis). Consumer confidence in Germany (Icon) improved during June, was flat in France, according to INSEE National Statistics Office, and gained in Spain, according to OPINA. A continuing debt crisis is likely hampering expenditure but, to a degree, the situation is becoming a “new normal” and without changes “on the margin”, I don’t expect any impact on MCD’s business in the Old World. Germany disappointed in May while France, Russia and the U.K. were highlighted as bright spots.

NEUTRAL: A result between 5% and 6% would be received as a neutral result because it would imply two-year average trends only slightly above the disappointing results seen in May.

BAD: A result below 5% would imply two-year average trends level with, or below, the disappointing two-year average trends seen in May.

APMEA - facing a difficult compare of +6.0% (including a calendar shift which impacted results by +0.0% to +0.3%, varying by area of the world).

GOOD: A print of 5% or higher would be received as a good result as it would imply a sequential acceleration in two-year average trends.

NEUTRAL: A result between 4% and 5% would be received as a neutral result because it would imply two-year average trends roughly level with May. APMEA was the only region in the world where MCD comps outstripped consensus in May.

BAD: Same-restaurant sales in APMEA below 4% would be received as a bad result because it would imply a slowdown in two-year average trends.

Howard Penney

Managing Director

Rory Green

Analyst