Initial Claims Rise 10k WoW (13k After Revisions)

Initial unemployment claims came in at 418k last week, up from 408k the prior week (revised from 405k). 1.75k of the claims were attributable to the Minnesota government shutdown. This is down from the prior week, when 11.5k of the claims arose from Minnesota government employees. On a rolling basis, initial jobless claims fell 3k week over week to 421k.

We've stated many times that our analysis shows rolling claims must reach a level of 375-400k on a sustained basis for any improvement in the unemployment rate to occur. We've also noted the relationship between Quantitative Easing and jobless claims, pointing out the fact that when QE is in effect it tends to lower claims and vice versa. Given that QE ended 3 weeks ago, we're not surprised to see rolling claims bounce along sideways. This is also an interesting takeaway for the broader market and the XLF as we also show below the relationship between those two benchmarks and jobless claims.

While there are many systemic risks facing the market right now from Europe to the Debt Ceiling to the Housing market, we come back to jobless claims time and again as the ultimate best read on what matters most for lenders. If jobless claims aren't improving this is a major overhang for the space, and when you add in weak home prices it paints an especially challenging picture for the group.

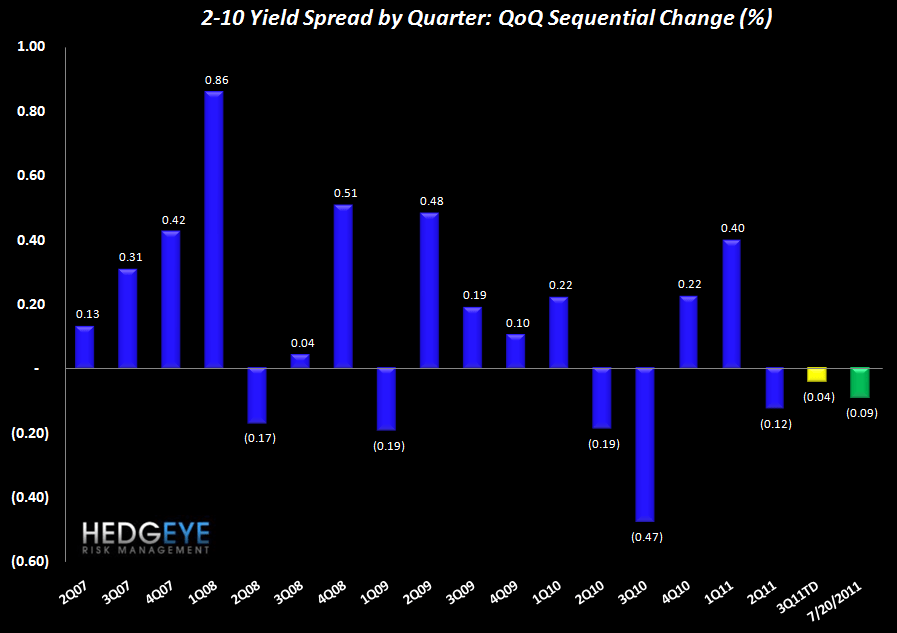

2-10 Spread Close to Flat WoW

The 2-10 spread, which we track as to gauge NIM pressure, was 1 bps wider WoW at 255 bps. The spread is currently running 4 bps tighter than 2Q.

Joshua Steiner, CFA

Allison Kaptur