This note was originally published at 8am on July 18, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“To hold cash you have to have a conviction that prices of something that you’d otherwise own will go down.”

-Jeff Gundlach, July 2011

That was an excellent quote from an excellent Risk Manager in a Bloomberg interview this morning. Jeff Gundlach is nobody’s yes-man. He has conviction in his research and risk management views and he understands there is a difference between the two.

He also understands how to use Cash as a risk management weapon. Currently, according to the article (“Gundlach Leads Bond Funds Boosting Cash to Most Since 2008 in Bullish Bet”), the CEO and Founder of DoubleLine Capital is running with 5x the amount of Cash he usually does. I like that. Today, Cash is king.

Since the beginning of 2011, one of the best ideas in the Hedgeye Asset Allocation Model has been Cash. We’ve held the most variant view (versus sell-side consensus) about US GDP Growth being slower than expected for the last 8 months. So why be fully invested in Global Equities when you have conviction that growth expectations need to come down?

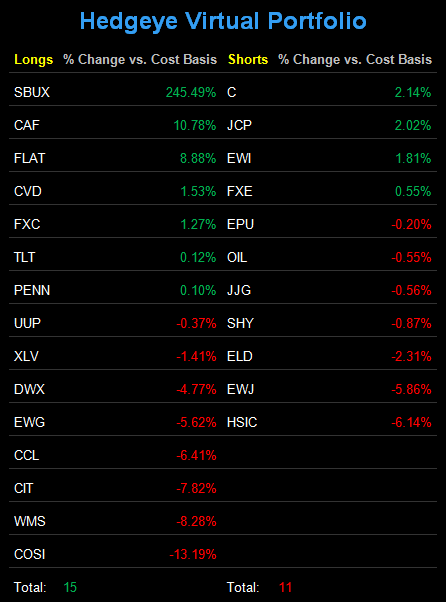

Here’s the Hedgeye Asset Allocation Model as of Friday’s market close:

- CASH = 46% (down from 49% last week)

- FIXED INCOME = 21% (Long-term US Treasuries and US Treasury Flattener – TLT and FLAT)

- INTERNATIONAL EQUITIES = 15% (China, Germany, and S&P Int’l Dividend – CAF, EWG, and DWX)

- FOREIGN CURRENCY = 12% (Canadian and US Dollars – FXC and UUP)

- US EQUITIES = 6% (Healthcare – XLV)

- COMMODITIES = 0%

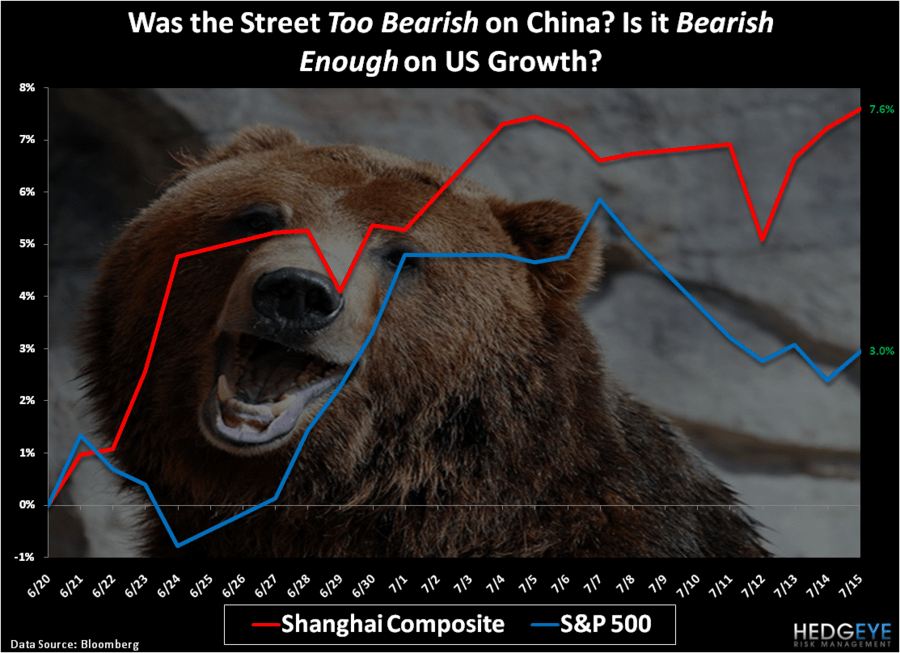

Now some people say they are bearish on US Growth. But are they Bearish Enough? Or, in the case of China, were they Too Bearish? The answers to these questions will be on the tape by the time 2011 is all said and done.

So let’s take some time to knock down the risk management pins, and look at my Global Macro positions in the aforementioned order:

- CASH– the art of risk management is not losing money when everyone else does. This position is not going to hurt me or my family (that’s how I look at asset allocation, because I can – my hard earned net worth doesn’t have a fully invested mandate).

- TLT – if people aren’t Bearish Enough on US Growth and they are too hawked up on inflation, they really need to be honest with themselves and re-allocate to long-term UST bonds. My immediate-term downside targets in 10 and 30 year US Treasury Yields are 2.82% and 4.11%, respectively. We have been bullish on the long-end of the UST Bond market since April 2011.

- FLAT – I still think an obvious way that both the market and investors can express a bearish view on US economic growth is through compression in the Yield Curve. When La Bernank went to QE1, the 10s/2s Spread peaked at 293bps wide. This morning it’s at 253bps wide. All I need for further compression is 2-year yields arresting their decline at the gravitational support level of zero.

- CAF – Chinese stocks have beaten US stocks by a 2-bagger since the June lows. Last night China closed down a small -0.12% for the Shanghai Composite’s first down day in the last 4. With Global Growth Slowing, I think you pay more for the growth that you can find.

- EWG – Germany is the long position that makes me most nervous. Why? Spend 3 minutes listening to a Eurocrat talk about how well they understand the interconnected global macro risk associated with Italy and Spain (we’re short Italy – EWI). We are long Germany because we like its fiscal and growth positions on a relative basis to almost everyone other than China (of the majors).

- DWX – International Dividend Yield of almost 6% here and guess what? As European stocks go lower, that yield goes higher! Chasing yield doesn’t work unless you buy it right. I have been early here (also referred to as being wrong), but have patience and time.

- FXC – Loonies were one of the best performing currencies in the world last week. We like safe resources. The Canadian Dollar is in a Bullish Formation (bullish TRADE, TREND, and TAIL) – and, yes, I am Canadian.

- UUP – We walked through why we are bullish on the US Dollar and bearish on the Euro in our Q3 Macro Themes Call on Friday (email sales@hedgeye.com if you want the replay/slides). The policy/currency scenario analysis is always complex, but the conclusion needs to be simple and heavily weighted towards timing/catalysts.

- XLV – Healthcare has been the top performing Sector in our 9 Sector S&P Risk Management Model for the last 3 months. We aren’t Johnny Come Latelys here either. At the beginning of 2011, we called Healthcare (XLV) and Energy (XLE) as our 2 favorites. Healthcare remains in a Bullish Formation (bullish TRADE, TREND, and TAIL) at +11.7% YTD.

Commodities at ZERO percent was really wrong last week on one position – Gold. After shorting Gold in December 2010 and covering the short position in January 2011, we’ve been long Gold (GLD) for the better part of 2011, but there are no buts – we aren’t long it here and missed a huge move last week (+3.1% week-over-week) to new all-time highs.

There is nothing inconsistent with the long Gold research and the rest of my positions other than not being long Gold itself. The Gold price is not only repudiating Keynesian Economics, but it continues to prove that it outperforms, big time, when the yield on real-interest rates is negative. Gold bulls can thank the Fiat Fools for that.

Three other week-over-week moves to think about while these central planners of the world attempt to unite one more time this week in Brussels and Washington:

- Euro/USD = DOWN -0.7% last week = bearish intermediate-term TREND (resistance $1.43)

- Small Cap US stocks (Russell 2000) = DOWN -2.8% last week = liquidity risk

- Volatility (VIX) = UP +22.2% to 19.53 last week = positively correlated to the US Dollar

All the while, Fiat Fool in Chief of the Europig nations, Jean-Claude Trichet, woke the world up to an epiphany in the FT Deutschland this morning: “Naturally the Europeans can manage the issue.”

Naturally, we’ll take the other side of that.

My immediate-term TRADE ranges for Gold, Oil, and the SP500 are now $1554-1608, $95.82-98.99, and 1297-1319, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer