Here is a comprehensive view of top line trends in the casual dining category heading into earnings season. Investors understand that commodity costs are elevated. The main battleground in the over-crowded casual dining category is growing same-restaurant sales. Most concepts in the category are still highly focused on attracting traffic through value-focused offerings with others focused on attracting traffic to quieter day parts while increasing turnover during busier times of the day.

DIN

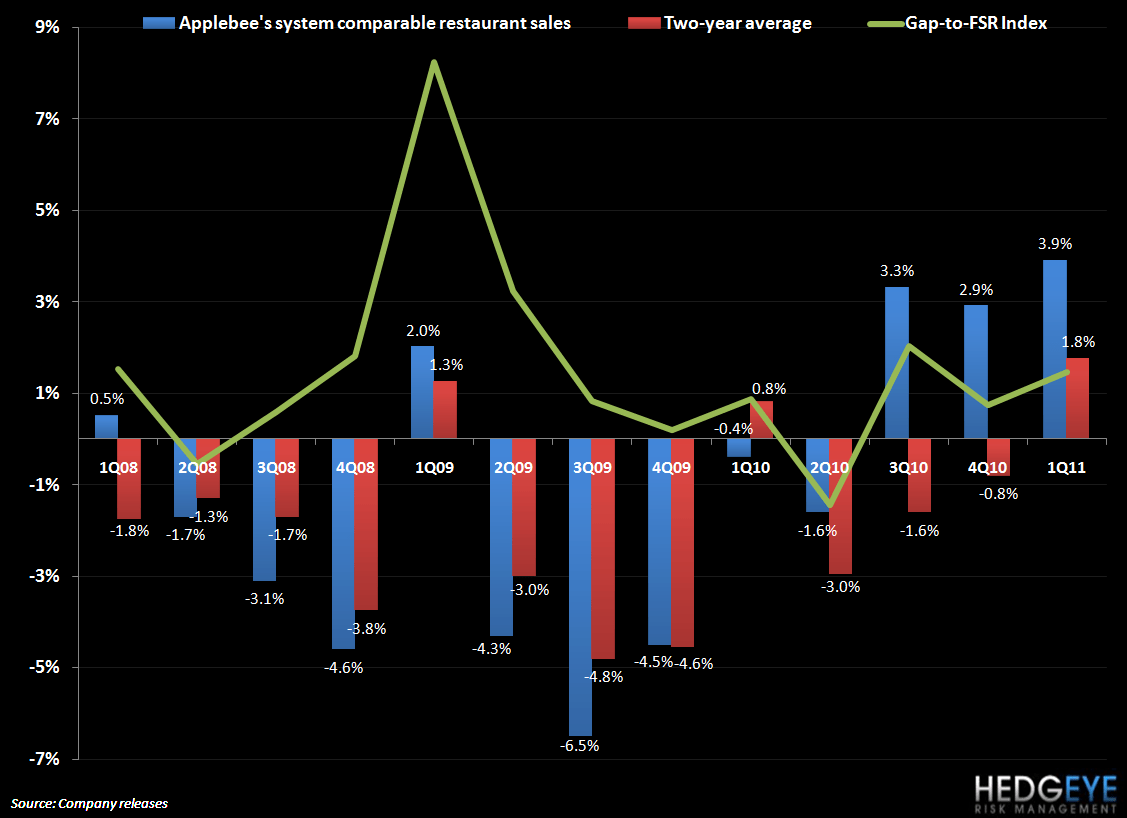

Applebee’s

Applebee’s has been an industry leader in the Bar & Grill category for some time and, along with Chili’s, is taking share from some of the weaker players. While I believe that Chili’s is momentum is improving at a faster rate than Applebee’s, I would be remiss to ignore the strong performance of the Applebee’s system over the past three quarters. With an easier compare, on a sequential basis, in 2Q than 1Q, I would expect Applebee’s system same-restaurant sales to accelerate on a one-year basis in 2Q. Furthermore, the trends in the Knapp Track casual dining same-restaurant sales index have been strengthening of late; given how important the Applebee’s system is for that index (its sheer number of units), I would expect the improving two-year average trends to continue. Indeed, any positive same-restaurant sales print for Applebee’s company sales would imply acceleration in two-year average sales.

IHOP

IHOP is a disaster and, as the chart below illustrates, has been underperforming the broader casual dining space by a growing margin as time rolls on. Management is floundering in its attempts to provide promotions that will attract sufficient traffic and commentary highlighting the need to “better differentiate the customer experience to drive sales and regain momentum” does not inspire confidence. IHOP is a small part of DIN’s business but the lackluster performance is disappointing nonetheless.

BJRI

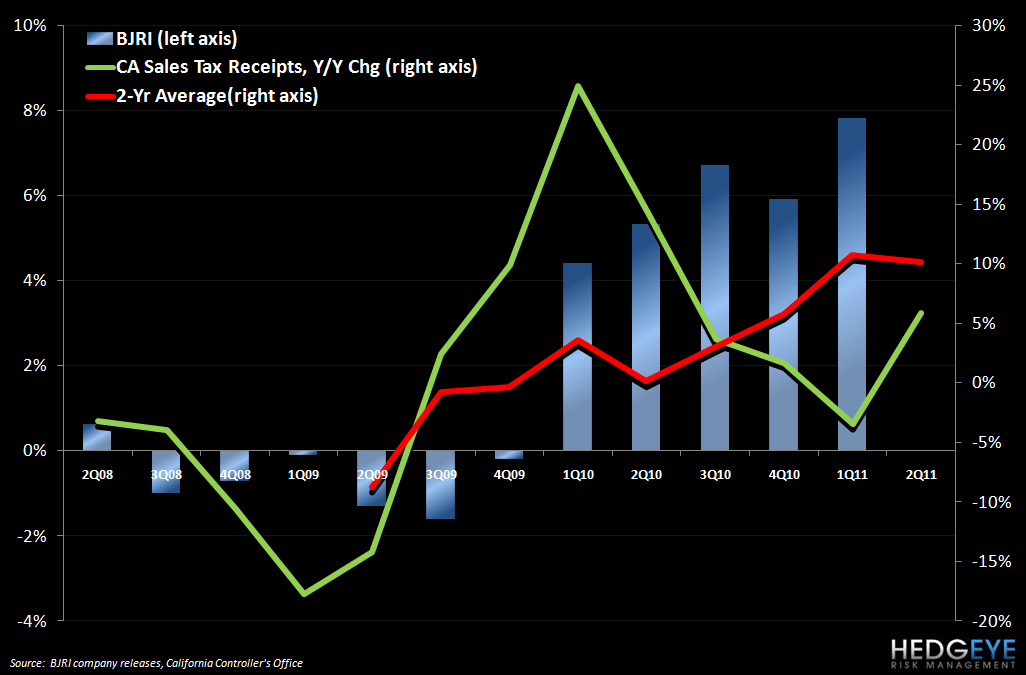

BJ’s restaurant is currently being awarded a lofty multiple of 17.8x EV/EBITDA NTM. Considering that DIN is currently

trading at 9.3x, and is the second most highly-valued company in the casual dining space behind BJRI, investors are clearly willing to pay up for the unit growth potential that BJRI offers. In terms of top-line trends, the company bounced back strongly post-recession. Last quarter’s company same-restaurant sales growth of 7.8% growth was an acceleration from the comp printed in the fourth quarter of 2010 despite a far more difficult compare for the first quarter. Management struck a cautious tone regarding the second quarter, stating on March 20 that, excluding the shift in the Easter holiday and spring break vacations, same-restaurant sales were estimated to be trending at approximately +5.5%. This would imply a sequential slowdown in two-year average trends of 70 basis points.

Looking at California Sales Tax receipts for the second quarter, it seems that consumer spending in the Golden State was robust during April, May and June. The two-year average trend, however, in sales tax receipts was slightly down. Approximately half of BJRI’s restaurants are in California so the chart below suggests that strong 2Q trends could be in store for BJ’s California units.

DRI

Darden is a consensus long but unless you have a bearish outlook on the space, it would not be an ideal play on the short side either. DRI recently reported earnings for their fourth quarter and full fiscal year 2011 recently. As the charts below show, the three primary concepts all saw declines in two-year average trends from the third fiscal quarter. The Olive Garden same-restaurant sales disappointed; two new entrée dishes – soffatelli with braised beef and soffatelli with chicken – drove traffic in line with the industry benchmark but fell short on average check. Additionally, despite raising prices at OG in 4QFY10, management decided against it in 4QFY11. Rather, management will introduce a new core menu and related pricing during the present quarter, the first quarter of fiscal 2012.

Red Lobster’s top-line during the fourth fiscal quarter was strong but two-year average trends did decline 90 basis points sequentially to -0.4%. Management announced on the conference call that the Red Lobster value promotions, was having a big impact on same-store sales.

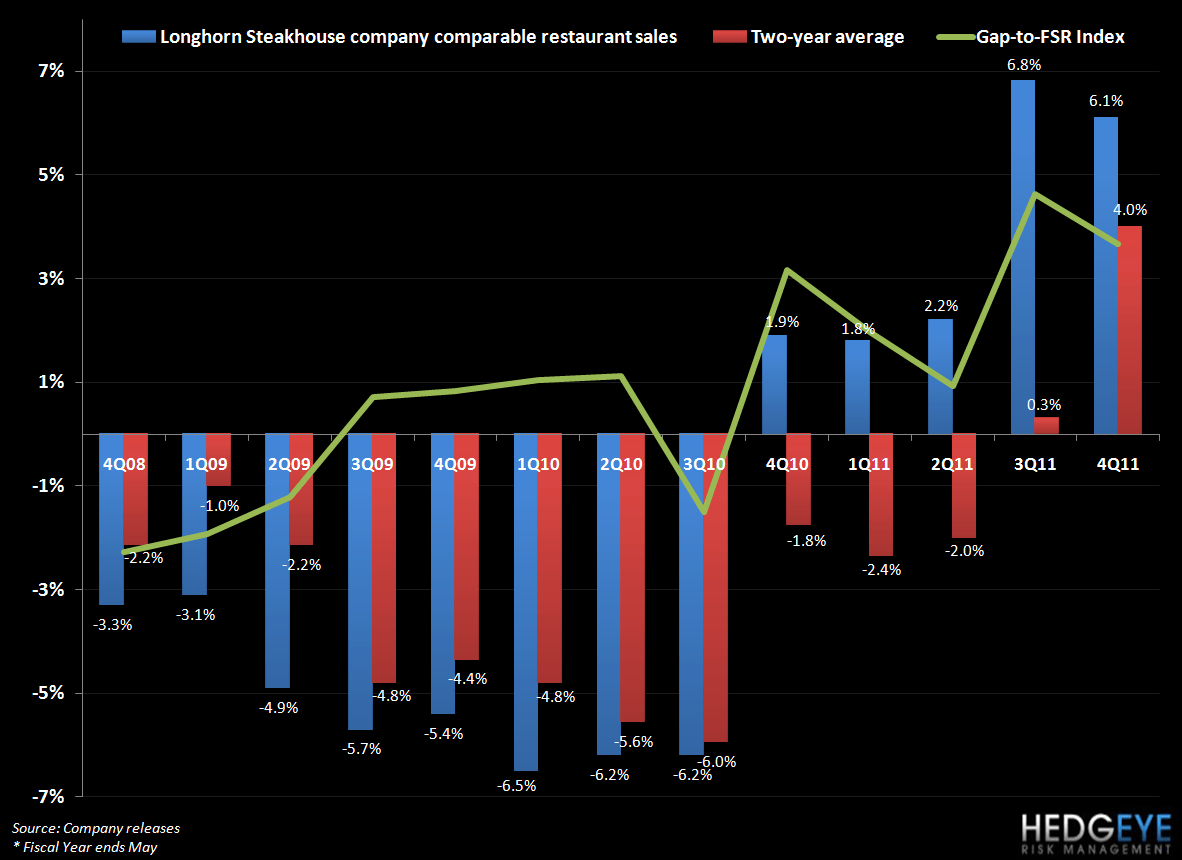

LongHorn printed a +6% same-store sales number for the fourth fiscal quarter, exceeding consensus expectations but implying a sequential slowdown in two-year average trends. LongHorn has been a consistent performer for Darden and has one last quarter of (relatively) easy comps before facing the +6.8% number of 2QFY11.

MRT

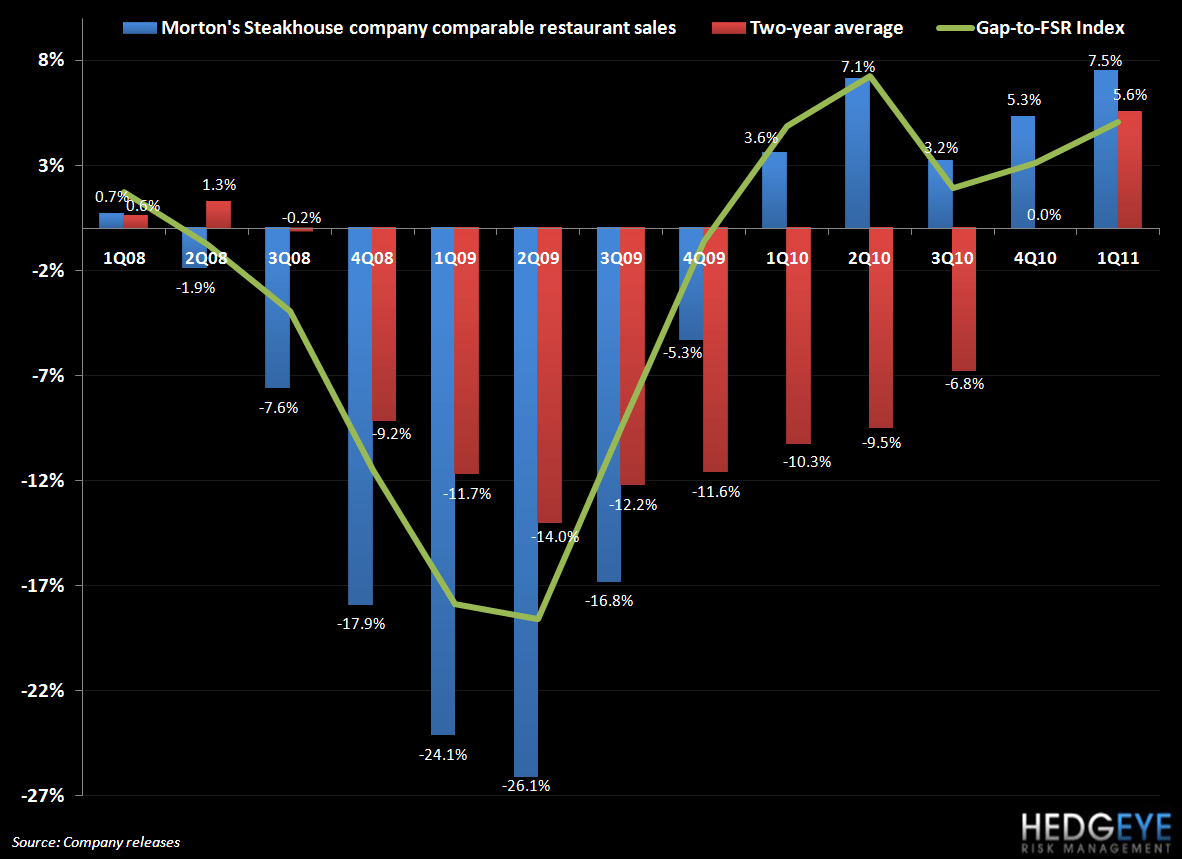

Morton’s is a company that has benefitted from the strong rebound in consumer confidence in higher income brackets. The rebound in equity markets (QE2) has corresponded with a steadying increase in the top-line performance of Morton’s on an absolute scale and, also, relative to the FSR Index. During the earnings call on May 4th, management stated that “The Morton's business continues to align perfectly with business travel and entertainment. Hotel RevPARs, as well as occupancy are on the rise, driven primarily from increased business travel Monday through Thursday.”

We would be of the opinion that, as much of a beneficiary as MRT has been of the rebound in capital markets, a slowdown from here could impact its business severely, as was the case in 2008. The company is guiding to margin expansion, driven by traffic and price (currently ~6% price on menu), in the second and fourth quarters of 2011 but expects 3Q to be “tough” due to lower traffic volumes over that period.

EAT

Chili’s

Ruby Tuesday’s CEO Sandy Beall’s statement that the Chili’s $6 lunch was having an impact on Ruby Tuesday’s lunch business was telling. Clearly the RT business is suffering but for the CEO to call out Chili’s specifically was significant. Given the size of the Chili’s system, the strong performance of the Knapp Track is also encouraging (as it is for Applebee’s). Another struggling casual dining competitor, CBRL, also highlighted “two very large chains” that are “on a big rebound” as being largely responsible for sending the Knapp-Track figures higher and the CBRL Gap-to-Knapp spread wider. The two chains CBRL management was referring to are obviously Chili’s and Applebee’s.

We believe that Chili’s will continue to execute from a top-line perspective in 2Q and, in the process, win over previously skeptical investors. Broad guidance for the year is for “flat-to-down 2%” but, given the strong trends in casual dining, per Malcolm Knapp’s data, it seems likely that two-year average trends will accelerate in 2Q. A print above -1.2% would imply a sequential acceleration in two-year average trends.

RUTH

Ruth’s Chris is has seen solid improvement in its two-year average trends over the last three reported quarters. There are certainly many things to like about this name: a lower average check ($70) than many peers, positive traffic for five consecutive quarters, and the stock is trading at the lowest EV/EBITDA multiple of any restaurant company.

In order to imply two-year average trends in line with those from 1Q11, Ruth’s Chris comparable restaurant sales will need to come in at +1.8% or better. 1Q11 was a stern test for RUTH comps given the significant step up in the difficulty of the compare in 1Q10 and, given the strength of 1Q11 comps and overall industry trends, we would expect 2Q to produce strong top line trends. The company is benefitting from TV advertising which it rolled out in 1Q and, while “comping” the impact of this advertising may prove difficult, for this year it should provide a significant benefit.

Given the overall trend in casual dining, and the fact that confidence levels among higher income consumers, while declining of late, has not declined as sharply as confidence has among consumers in many other income brackets.

RT

Ruby Tuesday’s sales trends were poor during the most recently reported quarter, the company’s third fiscal year of 2011, and management were quick to blame weather, high gas prices, and the economy for sluggish performance. Management also highlighted Chili’s $6 lunch and “two very large chains” (Applebee’s and Chili’s) taking share as thorns in RT’s side. It will be interesting to see if the fourth fiscal quarter, which reflects a period of relatively robust casual dining sales trends, also proves disappointing for RT.

4QFY11 comps for RT need to come in higher than -2.2% for a sequential improvement in two-year average trends. While it seems that this is likely, given the impact of weather on the first quarter, investors will look for strong improvement and convincing management commentary supportive of better trends. RT, at 6.6x EV/EBITDA, is currently one of the cheapest stocks in casual dining but I would look for more catalysts, and conviction on sales trends, before getting more constructive on this name.

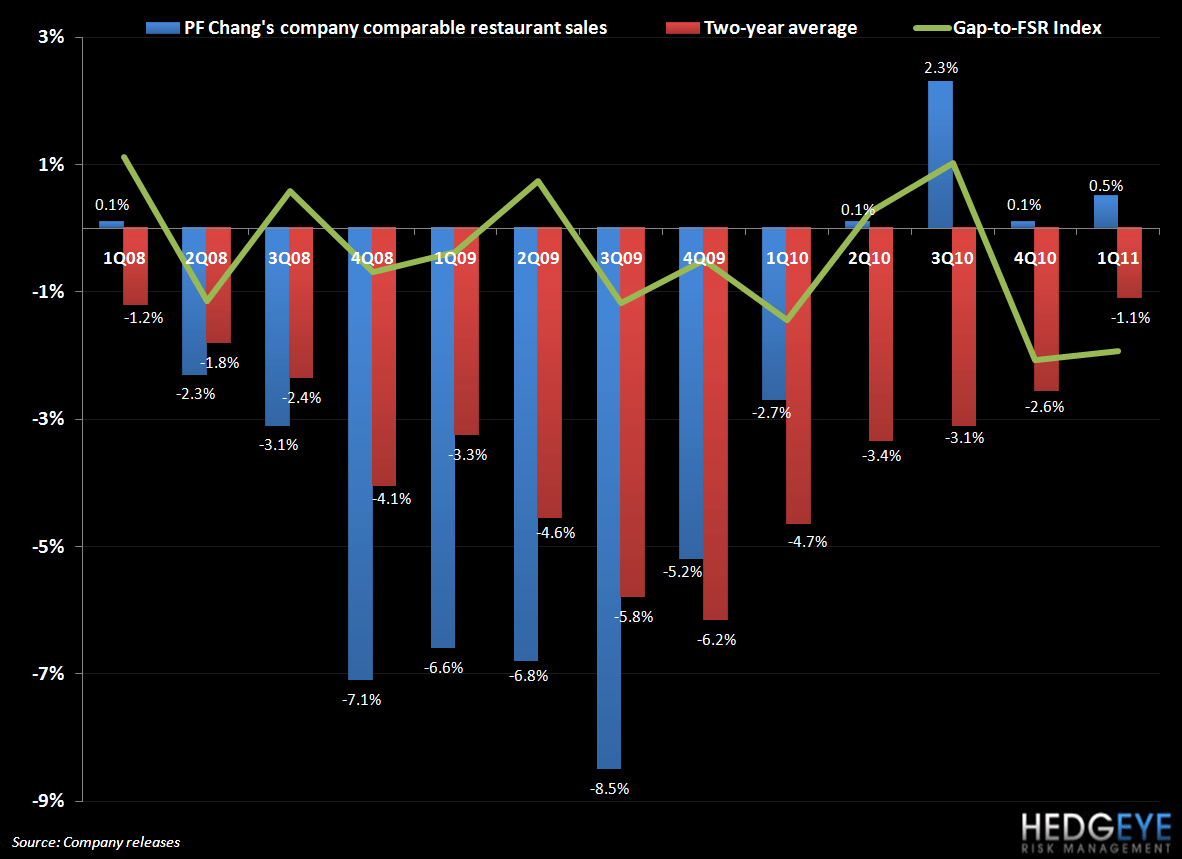

PFCB

Bistro

Sales at both concepts have lagged the industry over the last couple of quarters and, taking the management team’s commentary around April into account, it seems quite possible that 2Q will disappoint also. Specifically, management stated that January and February results were in line, March surprised to the downside and, at both concepts, April trends deteriorated from there, down -3% excluding the -2% impact of the Easter calendar shift. In order for the Bistro to maintain two-year average trends in the second quarter, a same-restaurant sales number of -2.2% or better is required.

Pei Wei

Pei Wei same-restaurant sales results were hampered in the first quarter by the fallout from an identity theft investigation focusing on Pei Wei employees in Arizona. According to management, the company will now be rolling out E-Verify for all new hires at Pei Wei. The Bistro already uses E-Verify.

Independent of the impact of the investigation on business in Arizona, there is concern about management’s ability to manage two concepts under one umbrella. The commentary around continuing soft trends (-3% excluding the -2% impact of the Easter calendar shift) in 2Q did little to raise investor optimism. In order for Pei Wei to sequentially improve two-year average trends, the concept needs to print same-restaurant sales better than -1%.

TXRH

Texas Roadhouse is a company that we hold a negative fundamental view of. Traffic compares for TXRH get increasingly difficult over the next three quarters. Adding price to the menu may have a muted impact on the overall comp given the traffic-heavy nature of the same-restaurant sales number’s composition. The TXRH core customer is sensitive to gas prices and it is possible that high gas prices during the second quarter, while declining overall since early May, could have impaired the company’s top line. The stock is trading at a lofty multiple of 8.3x EV/EBITDA, the fourth highest of the casual dining space behind BJRI, DIN, and BWLD.

BWLD

Buffalo Wild Wings is a company that has been performing well over the last twelve months, largely due to extremely favorable chicken wing prices, and same-restaurant sales improved significantly in the first quarter of this year. The second quarter faces an easy 2Q10 compare of -0.1%. In order to maintain sequential two-year average trends, BWLD will need to print company same-restaurant sales of at least 4.1%. Considering that April same-restaurant sales were up +5.3%, and Knapp Track trends in May were stronger than in April, it seems that an acceleration of two-year average trends in 2Q is probable, absent a slowdown in June.

KONA

Kona Grill has been a favorite idea of ours in 2011 and, as we wrote in June, the departure of former CEO Mark Buehler was not caused by business-specific factors. Furthermore, as we wrote at the time, business trends were in line with the company’s expectations and a remodel program coming through in 4Q11 will have a positive impact on comps. In order for Kona to maintain two-year average trends, same-restaurant sales of 5.4% or better will be required.

<chart14>

Howard Penney

Managing Director

Rory Green

Analyst