Now that the plausibility of LIZ jettisoning its ailing Mexx division is an increasing reality, we can’t help but think that people will start to look more closely at other pieces of the puzzle.

LIZ previously announced a Chinese JV that was literally lost by all the noise around this name. For those of you who are doing the deeper-dive analysis on LIZ (which we strongly recommend), here’s our analysis around this JV. Is it an absolute game changer? Probably not. But after doing the math, it turned out to be bigger than we initially suspected (over $0.20 in EPS run rate within 5-years – big for a company that’s currently losing money).

The Facts:

- LIZ has formed a new JV with E.Land, a Korean fashion company, to accelerate growth of Kate in mainland China

- the company has reacquired its Kate Spade business in China from Globalluxe starting June 1st, 2011 – at no cost

- The Kate Spade brand currently has 70 full price; 8 outlet stores in Asia (includes Japan roughly 50% of count, 5 stores in mainland China and SE Asia locations)

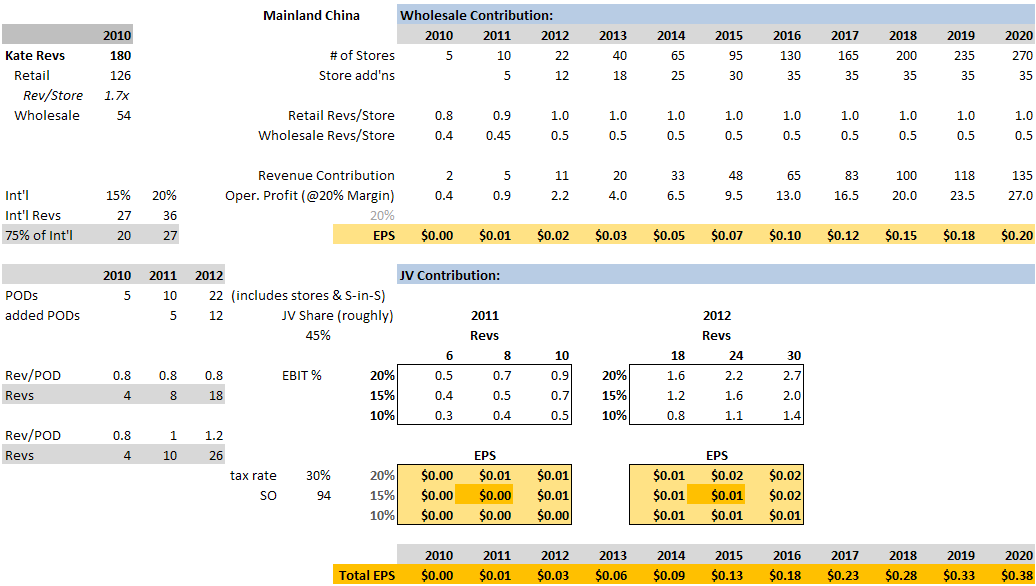

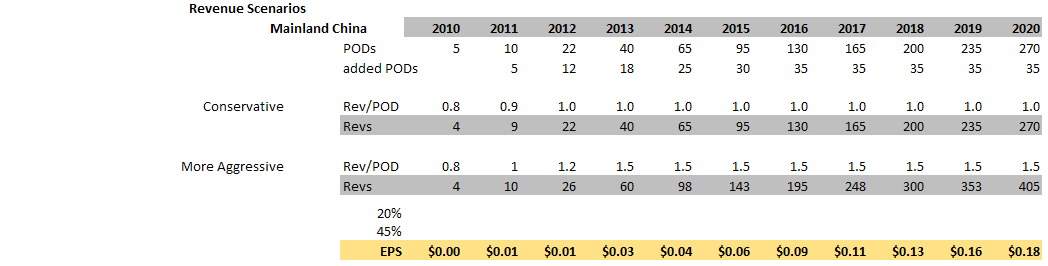

- Expects to grow Points Of Distribution in mainland China from 5 to 300 by 2020 = ~30/yr on average, but will ramp from ~10/yr initially (~5 in 2011)

- PODs include mall stores, free standing, and shop-in-shop locations

- Company plans to also reacquire is SE Asia business in 2014

Financial Implications:

- The prior structure was a distributor agreement whereby LIZ sold to Globalluxe on a wholesale basis

- The new structure will be to sell to the JV on the same wholesale basis (no change in revs to Kate), but LIZ will also realize a share of the profits/losses from the JV – realized in the “Other Income Line” in the P&L

- Of Kate’s ~$180mm in 2010 revs, retail and wholesale account for a 70/30 split respectively

- approximately 15-20% of revs were int’lly-based = $28mm-$36mm, the majority of which was Asia

- Assuming Asia accounts for 75% = $20mm-$28mm

- Assuming $8-$14mm is Japan; the rest is mainland China (probably only $2-$4mm) and SE Asia $6-$12mm

- Under the current JV agreement, LIZ and E.Land share start-up store costs based on their proportionate share. This costs are similar to the current U.S. structure:

- ~2k sq. ft. store

- ~$350/ sq. ft. initial capital costs

- = ~$700k / store (shop-in-shops are considerably less, typically under $100k)

- The following EPS impact is based on the beginning number of stores (5) and assuming a blended rev/store since the POD locations include mall stores, free standing, and shop-in-shop locations. Current Revs/Retail Store are $1.7mm per store based on 2010 results – our estimates suggest that ramps to $2.5mm per store in 2011. We assume $0.8mm-$1.0mm per store for our calculations below.

Contribution Forecast from Kate Spade China pre-deal:

Casey Flavin

Director