Notable news items and price action from the restaurant space as well as our fundamental view on select names.

MACRO

Yesterday, the ICSC chain store sales index reported that chain store sales grew at an above-trend pace last week. Recent data points on consumer spending does not seem to be hit by the reductions in confidence as the debt ceiling debate continues along with fears of a European debt crisis and weaker stock prices. Year-over-year growth posted its best two weeks since late December, topping 4.5% for two consecutive weeks for the first time since April 2010, when sales were benefiting from a shift in Easter.

For the week ending July 15, 2011, the MBA mortgage composite index surged 15.5% week-over-week driven by a sharp rise in the refinance index; the refinance index jumped 23.1% on the back of the 30-year fixed mortgage rate well below its 3 month moving average. The reality is that the purchase index declined 0.1% from the previous week, indicative of a struggling economic recovery and low consumer confidence. So if no one is buying a new home there is lots of money left over to go out to eat!!

General Mills CEO on food costs - CEO Ken Powell said that higher food prices are here to stay and it was unlikely that food prices will slip into a deflationary cycle as they did last year. "The long-term trends are inflationary, not deflationary and you are going to see pricing in a significant way,"

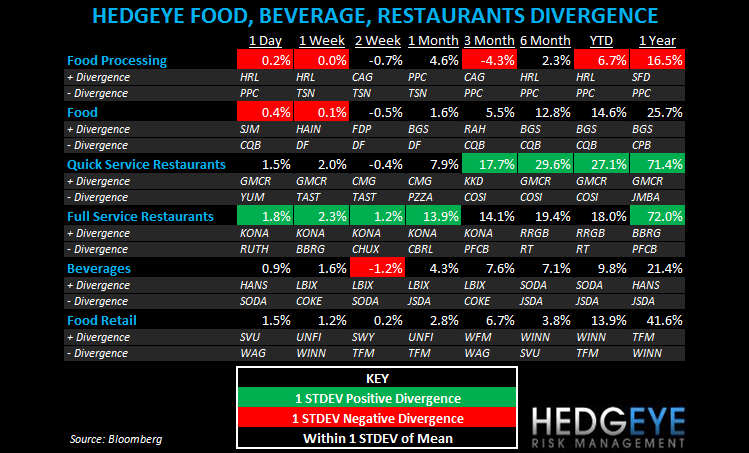

In our subsector model, food processing stocks continue to underperform.

QUICK SERVICE

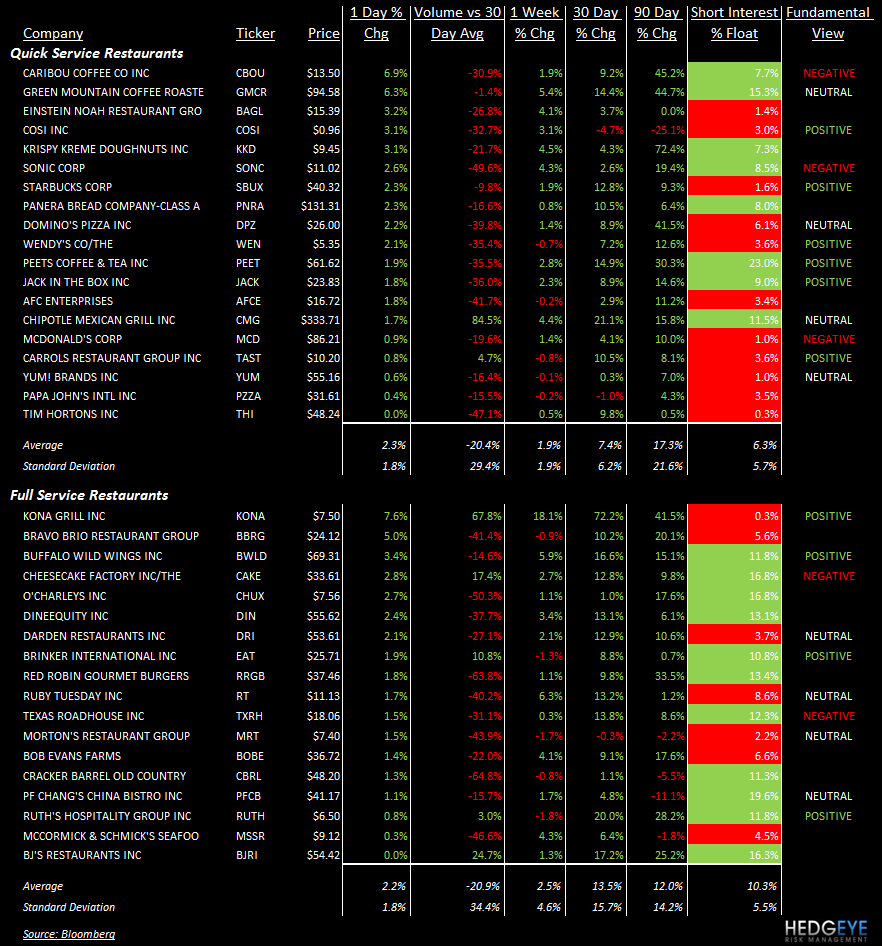

- CMG reported $1.59 in EPS, below street expectations, but the company’s strong top line outlook and plan to take price in 3Q has convinced JP Morgan to raise estimates and Piper Jaffray to raise its price target to $352.

- SBUX “ready-to-eat” chicken products have been recalled by Flying Food Group LLC. Approximately 204 pounds of ready-to-eat chicken wraps and plates that may be contaminated with Listeria monocytogenes are being sought by the Lawrenceville, Ga., establishment.

- SBUX has named Kris Engskov as the managing director for its UK and Ireland stores.

- MCD The first McDonald's restaurant in Bosnia opened for business in the capital Sarajevo on Wednesday.

FULL SERVICE

- MSSR - Discovery Group, a Chicago-based investment firm, acquired a 6.3-percent stake in McCormick & Schmick’s Seafood Restaurants Inc. in what some see as a move to take advantage of an expected higher sale price.

Howard Penney

Managing Director

Rory Green

Analyst