TODAY’S S&P 500 SET-UP - July 20, 2011

Yesterday, volume and Volatility (2 of our 3 core risk management factors) didn't confirm the PRICE move today, but 2 or 3 more days of follow through on this PRICE strength should do it and could easily carry this market towards 1352 SPX. If today's Tech move (+2.3% XLK) was a head-fake (doubtful given AAPL at the close), it would need to be confirmed by a TREND line breakdown of SPX 1319.

As we look at today’s set up for the S&P 500, the range is 33 points or -0.58% downside to 1319 and 1.90% upside to 1352.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: +1749 (+3888)

- VOLUME: NYSE 870.65 (-0.41%)

- VIX: 19.21 -8.31% YTD PERFORMANCE: +11.5%

- SPX PUT/CALL RATIO: 1.63 from 1.99 (-18.19%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 23.68

- 3-MONTH T-BILL YIELD: 0.03% +0.01%

- 10-Year: 2.91 from 2.94

- YIELD CURVE: 2.57 from 2.57

MACRO DATA POINTS:

- 7 a.m.: MBA Mortgage Applications, prior (-5.1%)

- 9 a.m.: Moody’s U.S. commercial property prices

- 10 a.m. Existing home sales, est. 1.9% to 4.9m, prior (- 3.8%)

- 10:30 a.m.: DoE inventories

- 6:15 p.m.: Fed’s Sack to speak to money marketers in NY

WHAT TO WATCH:

- President Obama will renew talks at the White House this week, praised bipartisan Senate proposal for a $3.7t debt- cutting plan that emerged yesterday; House Republicans passed their own version yesterday

- Greek Prime Minister George Papandreou to meet with EU leaders in Brussels tomorrow as officials struggle to agree on measures to restore confidence in region’s creditworthiness

- WSJ is cautious on Cheerios (GIS), Frosted Flakes (K), Grape-Nuts (RAH)

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Oil Climbs for Second Day on Shrinking Crude Stockpiles, Stronger Economy

- Copper Declines for First Day in Four as Three-Month High Spurs Selling

- Corn Gains for a Second Day as Hot Weather in U.S. Midwest May Hurt Yields

- Gold May Decline on Optimism Solution Is Nearer for Sovereign-Finance Woes

- Coffee Falls as Supplies May Be Adequate to Meet Demand; Sugar Advances

- Gold Price at Record Fails to Deter Purchasing in India as Demand Advances

- Milk Powder Slumps to Eight-Month Low After Fonterra’s Call Proves Correct

- Japan Won't Rule Out Possibility Radioactive Fukushima Beef Was Exported

- Zinc Trades Near the Highest Price Since April as Supplies May Be Limited

- Rice Exports From India at $400 a Ton May Lower Global Prices, Group Says

- Rubber Supply Tightness Lasting Until 2018 May Raise Costs for Tiremakers

- Ethanol Rebounds on Tax Credit, Price Discount to Gasoline: Energy Markets

- Russia Arctic Route to Rival Suez May Aid Sovcomflot IPO: Freight Markets

CURRENCIES

EUROPEAN MARKETS

- EUROPE: ominous bounce to lower-highs; Italy fading here and Greece about to go negative on day; Sold my Germany yesterday; shorting Italy with impunity

- Germany Jun PPI +5.6% vs consensus +5.5% and prior +6.1%

- BOE MPC Committee minutes say recent developments had reduced the likelihood that a tightening in policy would be warranted in the near term

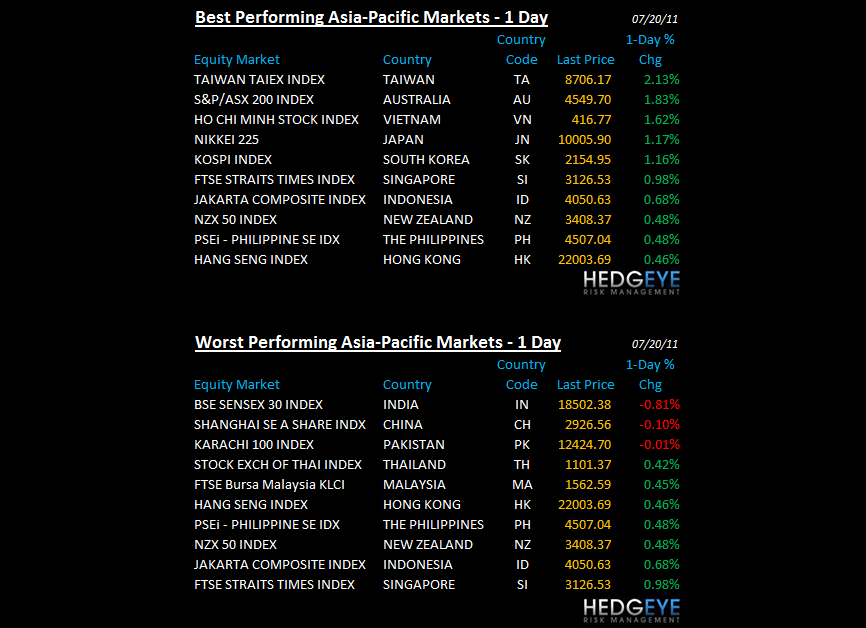

ASIAN MARKETS

- ASIA: surprisingly mixed give the Apple of everyone's American eye - India down -0.8%; China down -0.1% w/ Korea/Japan/Aus all up over 1%

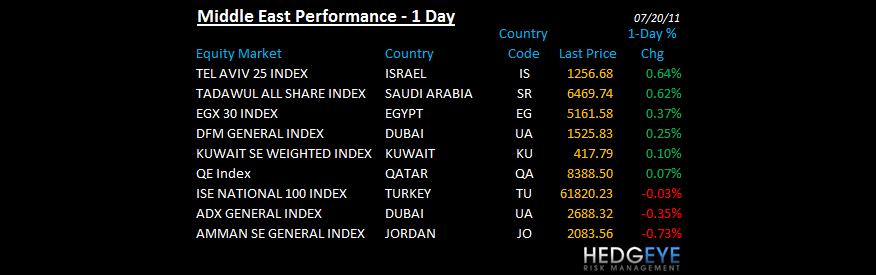

MIDDLE EAST

Howard Penney

Managing Director