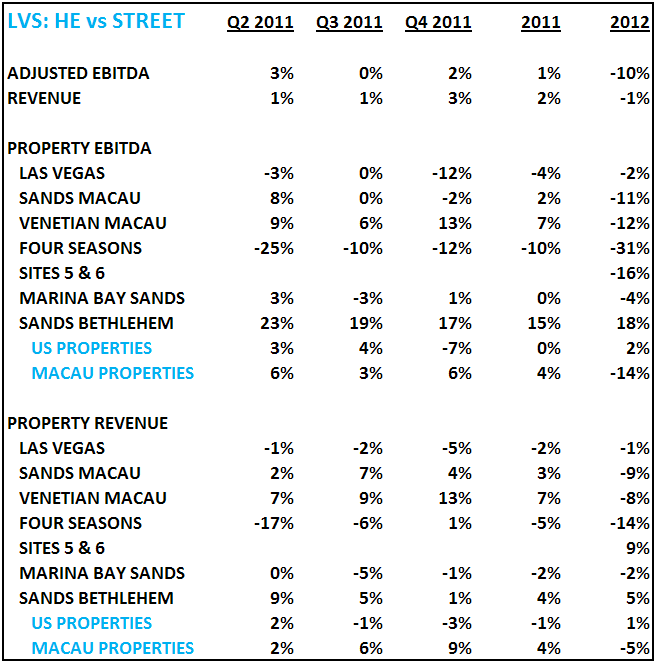

We’re expecting LVS to report a slight beat after the help of high hold in Macau. Singapore could be the standout, finally, after a few quarters of “disappointing” results.

We don’t think LVS will match WYNN’s standout quarterly release from last night. We’re even more confident that MPEL overpowers all Macau operators for Q2, particularly LVS. The Street looks a little light to us in Macau and Singapore and a high in Las Vegas. Wynn’s blowout in Las Vegas may not carry over to Venetian Las Vegas. As always, LVS has a lot of moving parts and high expectations so it’s particularly difficult to predict the post earnings stock reaction. Expectations are likely to be even higher after Wynn reported last night so we are a little cautious. A bigger beat than expected in Singapore could be the only hope for a positive move in the stock.

MACAU

We estimate that LVS’s Macau properties will report property level net revenue of $1,183MM and EBITDA of $394MM, 2% and 6% ahead of Street estimates. Sands and especially Venetian played lucky, while FS suffered from poor luck. All in, we estimate that lady luck helped LVS’s Macau properties by $65MM on the net revenue front and by $34MM in EBITDA.

Sands

We estimate that Sands will report $339MM of revenue and $105MM of EBITDA, 2% and 8% ahead of consensus, respectively.

- Net gaming revenue of $331MM benefiting from high hold

- Gross VIP table win of $240MM and $163MM net

- Table drop up 4%, to $7.5BN, assuming 10% direct play, and hold of 3.2%

- We estimate a hold benefit of $26MM on gross revenue, $18MM on net revenue and $10MM on EBITDA

- Gross VIP table win of $240MM and $163MM net

- Mass table revenue of $139MM (assume 15% increase in drop and 20% hold)

- Slot win of $29MM (assume 18% increase in handle and 6% win rate)

- Net non-gaming revenue of $8MM and expenses of $4MM

- Variable expenses of $188MM

- Taxes of $159MM

- Gaming commissions in excess of the rebate of $18MM

- Fixed expenses of $42MM – in-line with 1Q and 5% below 2Q10

Venetian

We estimate that Venetian will report $729MM of revenue and $262MM of EBITDA, 7% and 9% ahead of consensus, respectively.

- Net gaming revenue of $647MM benefiting from high hold

- Gross VIP table win of $452MM and $317MM net

- Table drop up 30% YoY, to $12.7BN, assuming 18.5% direct play, and hold of 3.5%

- We estimate a hold benefit of $89MM on gross revenue, $62MM on net revenue and $36MM on EBITDA

- Gross VIP table win of $452MM and $317MM net

- Mass table revenue of $279MM (assume 15% increase in drop and 27% hold)

- Slot win of $52MM (assume 5% increase in handle and 7% win rate)

- Net non-gaming revenue of $82MM and expenses of $20MM

- Variable expenses of $346MM

- Taxes of $305MM

- Gaming commissions in excess of the rebate of $21MM

- Fixed expenses of $101MM – flat with 2Q10

Four Seasons

We estimate that Venetian will report $116MM of revenue and $27MM of EBITDA, 17% and 25% below consensus, respectively.

- Net gaming revenue of $95MM hurt by low hold

- Gross VIP table win of $71MM and $46MM net

- Table drop down 32.5% YoY, to $3.3BN, assuming 40% direct play, and hold of 2.2%

- We estimate hold dragged down gross revenue by $22MM, net revenue by $15MM and $12MM on EBITDA

- Gross VIP table win of $71MM and $46MM net

- Mass table revenue of $38MM (assume 31% increase in drop and 30% hold)

- Slot win of $11MM (assume 70% increase in handle and 7% win rate)

- Net non-gaming revenue of $21MM and expenses of $7MM

- Variable expenses of $61MM

- Taxes of $47MM

- Gaming commissions in excess of the rebate of $11MM

- Fixed expenses of $21MM compared to an estimated $19.4MM in 1Q11 and $28MM in 2Q10

SINGAPORE

We estimate that MBS will report $640MM of net revenue (in-line with Street) and $338MM of EBITDA (3% higher than the Street).

- Net gaming revenue of $500MM

- Gross VIP table win of $292MM and $162MM net

- Table drop of $10.4BN and hold of 2.8%

- Gross VIP table win of $292MM and $162MM net

- Mass table revenue of $223MM (assume $1,006MM of table drop and 22% hold)

- Slot win of $116MM

- Net non-gaming revenue of $130MM ($162MM net of $32MM of promotional expenses)

- Variable expenses of $113MM

- Taxes of $106MM

- Fixed expenses of $180MM compared to an estimated $182MM in 1Q11

U.S.

We estimate that LVS’s US operations will report in-line results of $416MM of net revenue and $102MM of EBITDA

Las Vegas

We estimate that Venetian and Palazzo will report combined revenue of $314MM and EBITDA of $77MM, slightly below street estimates.

- Net gaming revenue of $101MM

- Table win of $76MM

- Flat YoY drop of $417MM and ‘normal’ hold of 18.3%

- Table win of $76MM

- Slot win of $38MM

- 30% decrease in slot handle to $470MM and 8% win rate

- Non-gaming revenue of $235MM

- $117MM of room revenue

- 93% occupancy and ADR of $196

- $117MM of room revenue

- F&B, retail and other revenue of $119MM

- $22MM of promotional allowances

- Operating expenses of $229MM, up 13% YoY and comparable to 1Q11 operating expenses of $233MM

Sands Bethlehem

We estimate that Sands Bethlehem will report net revenue of $102MM and EBITDA of $28MM, 23% and 9% above consensus, respectively.

- Casino revenue of $92MM

- Table win of $24MM

- Slot win of $68MM

- Non-gaming revenue of $10MM

- $41MM of taxes and $33MM of operating expense