Moving Beyond EBA Conclusions That All is Well

Our view of the European bank stress tests released last Friday is rather dim. We criticized the leniency of the "adverse scenario" assumptions, noting in particular that the actual deterioration since year-end 2010 is already worse than the "adverse" assumptions in some cases. (Contact us if you want to see our full note.)

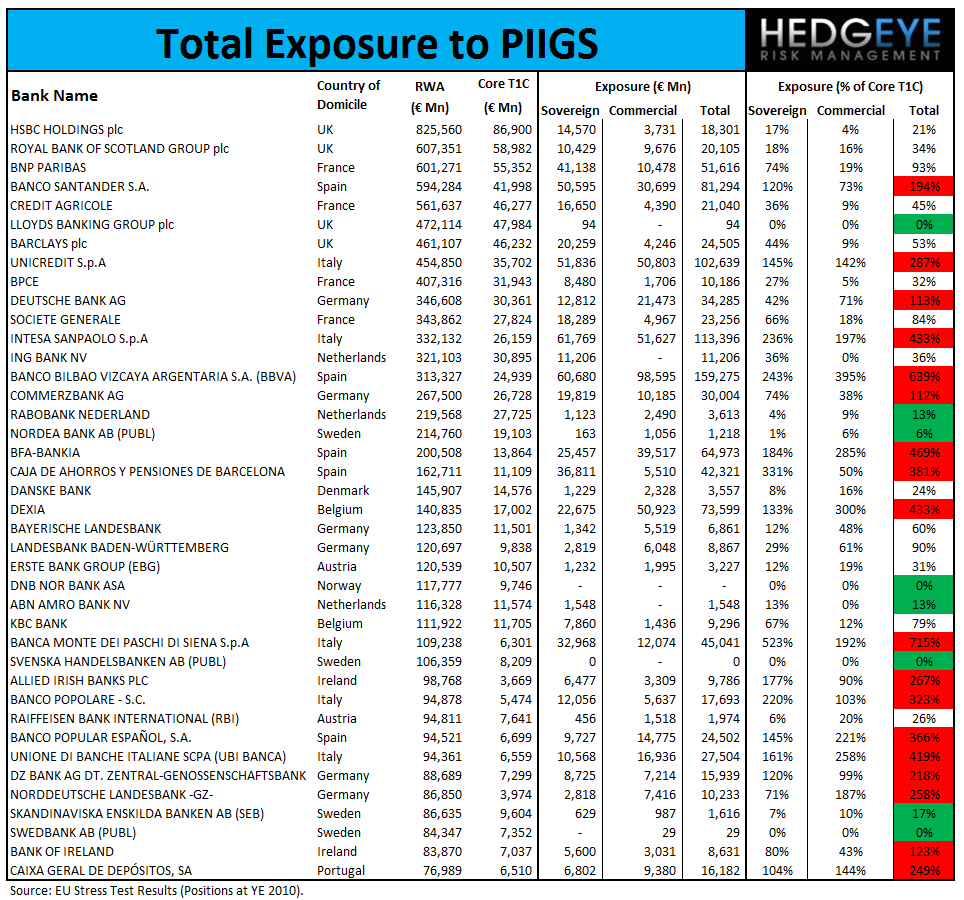

While we consider the loss assumptions to be balderdash, the stress tests were valuable in that they disclose a wealth of bank-specific data around sovereign and commercial exposures by country. Clearly, the greatest default risk is currently in Greece, Portugal and Ireland. Italy and Spain, while on slightly more stable ground, are rapidly deteriorating as well.

In the tables below, we show the exposure to sovereign debt and commercial loans by bank to each PIIGS country. Specifically, we show the top 40 most exposed European banks (among the 91 stress-tested), ranked by gross loans and sovereign debt holdings as a percentage of their Core Tier 1 Capital. Bear in mind that this data is as of December 31, 2010. In addition to showing which banks hold the greatest exposure on a country by country basis, we also show which banks hold the greatest exposure to Greece, Portugal and Ireland collectively, as we view those countries as being at greatest risk for default. Further, we show total exposure to all five PIIGS countries.

We highlight in red those banks with 100% or more of their Core Tier 1 Capital in the form of sovereign debt holdings and/or commercial loans to a given country or group of countries. The total exposure groups (all PIIGS) are presented two ways. First, we show exposure sorted by RWA. In other words we show the PIIGS exposure by bank for the 40 largest European banks. Second, we show exposure sorted by % of Core Tier 1 Capital at risk regardless of the size of RWA.

Summary Conclusions: 13 of the Top 40 EU Banks Hold Over 200% of their Capital in PIIGS Exposure

We find that there are numerous European banks with over 100% of their Core Tier 1 Capital committed to either PIIGS commercial loans or PIIGS sovereign debt holdings. For example, we found that 18 of the 40 largest European banks held 100% or more of their Core Tier 1 Capital in PIIGS sovereign debt or commercial loans. In 13 of these cases, the banks held more than 200% of their Core Tier 1 Capital in PIIGS sovereign debt or commercial loans.

As a general rule we found that the Nordic banks are the least exposed to PIIGS debt, typically holding less than 20% of their Core Tier 1 Capital, putting them at considerably less risk than the group as a whole.

Joshua Steiner, CFA

Allison Kaptur