This note was originally published at 8am on July 13, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Emerging markets today are not what the developed markets were in their infancy.”

-Rama Bijapurkar

That’s a very simple, but often misunderstood, Global Macro investment point from a book I have recently cited about India’s Macro Consumer market: “We Are Like That Only”, by Rama Bijapurkar (2007).

Simple is as simple does - and this morning those who are still storytelling about China’s pending collapse are going to learn that lesson the hard way. China’s Q2 GDP report was outstanding.

Hedgeye isn’t a perma-bull on China. I personally don’t aspire to be perma-anything other than permanently managing risk. Risk lives and breathes through a vacuum of expectations. After seeing its stock market down -14.3% in 2010, expectations for Chinese stocks are low and short interest is high.

Before I get into what the short sellers of China have wrong, let’s rattle off what the bulls have right in this morning’s GDP report:

- China Q2 GDP beat our already bullish expectation of 8-9%, coming in at +9.5% (we care about buy-side expectations)

- Fixed Asset Investment growth in Q2 was up +25.6% year-over-year; that’s big – China can print government spending too

- June data reports (Retail Sales and Industrial Production growth) were big sequential accelerations versus May

Now, back to the short sellers…

On two critical leading indicators, Mr. Macro Market has warned the shorts that Chinese growth was not going to be the train wreck that US unemployment has become:

- Chinese stocks (Shanghai Composite Index) are up +6.6% since bottoming on June 20th, 2011

- Copper prices (highly correlated to Chinese demand) are up +12.5% since bottoming in mid-May

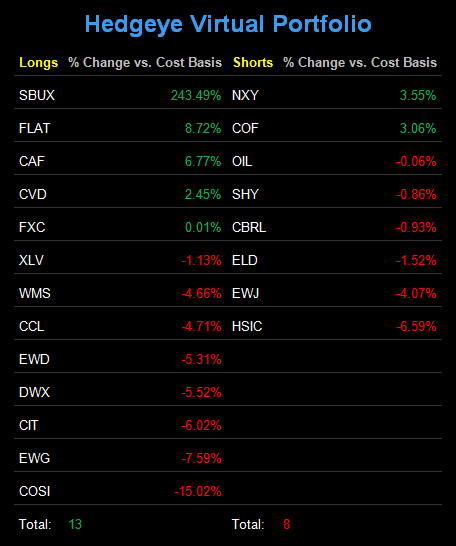

Hedgeye bought China (CAF) on June 16th.

Bottoms are processes, not points – we get that. Whether or not we bottom-ticked buying China isn’t the point. The point is that managing risk on a globally interconnected basis works both ways. Being Too Bearish at bottoms can carry a short seller out.

As a credibility check, we were long Chinese Equities in 2009 and short them in 2010. It’s actually amusing to get emails (from some of the same people who were accusing me of being “too bearish” on China in Q1 of 2010) insinuating that now I’m “too bullish!”

Thankfully, that’s the institutionalized business that we are paid to manage expectations in – a business where career risk management often trumps risk managed research – a business where plenty chase the rabbit, rather than being the rabbit.

Sometimes the rabbit gets eaten. We get that too. But Wall Street is smart enough to know that the weaponry of these 3 factors working in one direction is something that they need to manage career risk around:

- Bullish data

- Rising stock prices

- High short interest

Bullish data and the prices that support it are crystal clear for everyone to see this morning (China was up +1.5% on the “news”). What you can’t see are the shorts squirming. So here are a few more things to consider on that score:

- Short interest in Chinese stocks has almost doubled since the beginning of January 2011 (4.8% versus 2.9% of total shares)

- At $961M YTD, outflows in the FXI (China ETF) were the highest of ANY COUNTRY ETF in the 140 countries in XTF Inc’s database

- Moody’s (the ultimate lagging indicator) put China “bank debt concerns” on their radar on July 5th

Now those 3 factors aren’t exactly contrarian indicators of a “fresh new best idea” someone wants to present on the short side at the Ira Sohn conference (although someone did). Maybe they should be bucking up for some insurance research and read Hedgeye.

On Friday, our Macro Team will be making our 2ndslide presentation on being China Bulls with our launch of the Q3 Hedgeye Macro Themes. We’re calling one of our Q3 Themes “Chinese Cowboys.”

Giddy up.

My immediate-term support and resistance ranges for Gold, Oil, and the SP500 are now $1536-1572, $94.11-99.79, and 1301-1330, respectively. Manage your risk around the ranges.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer