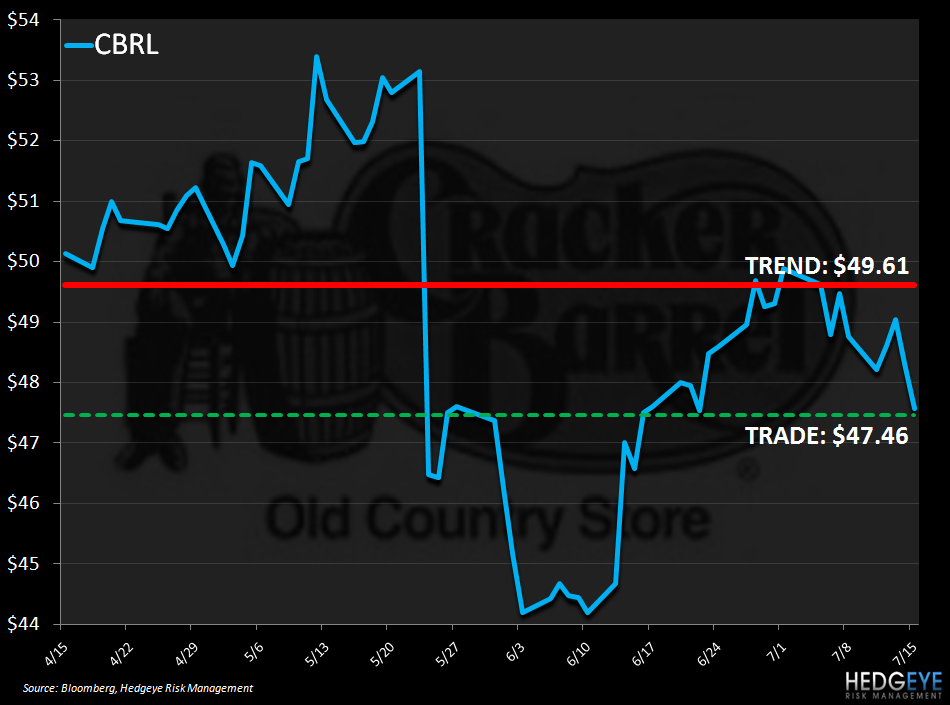

Keith just covered CBRL in the Hedgeye Virtual Portfolio as the stock is immediate term TRADE oversold. Both the quantitative and fundamental setups are bearish on the intermediate term TREND duration.

I hold a cynical view of the CBRL announcement today. My impression even before today's "news" was that they were going to miss the quarter and today’s headline only confirms that view. The charge the company is taking, estimated to be between $0.14 and $0.17, is related to the reduction of staff and management levels.

Why do you think CBRL made the decision now to get religion on the cost structure? The answer is clear; they are going to miss the quarter. There is also a possibility that an activist investor may be exerting some pressure on the company's management team.

As the chart below illustrates, the stock is immediate-term TRADE oversold from a quantitative perspective. While Keith covered the stock in the Hedgeye Virtual Portfolio this afternoon, the intermediate term TREND setup remains bearish.

Howard Penney

Managing Director

Rory Green

Analyst