Notable news items and price action from the restaurant space as well as our fundamental view on select names.

MACRO

The CPI for food was 0.2% in June, half the pace seen in each of the previous two months and noticeably weaker than the 0.8% gain in March. Food prices were up 3.7% year-over-year in June, compared with 3.5% in May and the strongest since March 2009.

While YUM’s US business has plenty of problems specific to its businesses, management also pointed out that high gas prices are making the U.S. recovery harder. Gas prices are down 8% from early May but have rebounded 4% from the low on June 29.

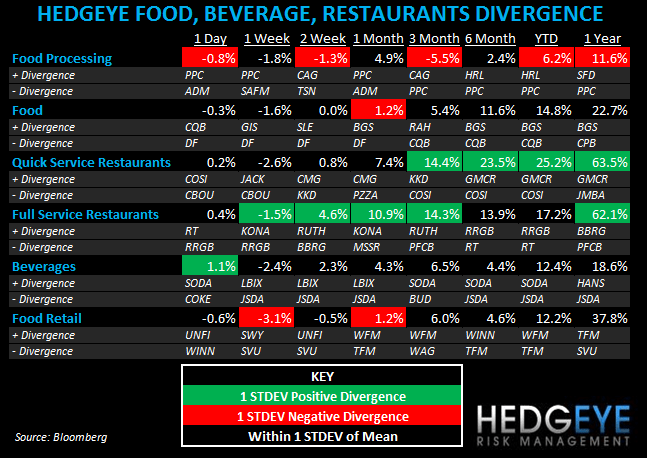

Restaurant stocks have been performing extremely strongly and food processors continue to underperform.

QUICK SERVICE

- SBUX will launch a JV with a Chinese coffee-growing company, the Ai Ni Group, later this year as the two sides signed an MOU Thursday. Ai Ni Group is a coffee-growing and –processing firm in the southwestern province of Yunnan.

- MCD has “adjusted” some prices in China after inflation has hit a three-year high.

- YUM traded higher thanks to extremely strong reported China top-line trends. Low quality EPS and down margins remain a concern.

- The coffee concepts declined on accelerating volume.

CASUAL DINING

- CBRL is almost certainly going to miss the quarter, in our view, as they announced news this morning that they are reducing management and staff positions. The charge is estimated to be $0.14-$0.17.

Howard Penney

Managing Director

Rory Green

Analyst