Stress Test Results Tomorrow Will Dramatically Understate Risk

We don't think it's too great a stretch to call tomorrow's EU "Stress Tests" absurd. Why? Consider the following. The stress test results to be released tomorrow. are based on balance sheet data from the banks at December 31st, 2010. No changes in exposure since then are reflected. Furthermore, the macro assumptions work off of a baseline of what the world looked like at year-end 2010. This means that the current state of the world is actually much worse than the so-called "adverse" scenario in many cases.

The charts below look at what the EU considered for its "adverse" scenario, namely the backup in sovereign bond spreads relative to German Bunds, compared with what has actually occurred in the market.

The starting point for the tests is YE2010. This is the date when the stress test scenario analysis begins. In the charts below we show the amount by which the stress tests assumed sovereign spreads would widen vs. the amount they have actually already widened by. Let's do a quick case study on Portuguese 15 year sovereign bonds, as these are the bonds the stress test assigns the biggest haircuts to under their adverse scenario. Looking at the 15 year bonds of Portugal, the EU stress test assumes the bonds widen by 251 bps against German bunds in an adverse scenario. In reality, however, Portuguese 15 year bond spreads have already widened by 612 bps since YE2010. Under the 251 bps scenario, the EU estimates that the haircut on those bonds would be 30.6%. You can do the math on what a 612 bps scenario means for the haircut.

Performing the same analysis on the 2-year Portuguese bonds, the stress test assumes 201 bps of spread widening, when in reality 2-year spreads have widened by 1,860 bps. Under the EU stress test adverse scenario, their 201 bps assumption triggers a 5.5% haircut on those bonds. Given the actual widening is closer to 9x what they've assumed it seems reasonable to conclude that the stress tests will quite materially understate the real risk in the system.

This profound ignorance of reality repeats across durations and countries. As such, it will be hard to take seriously the EU's conclusions tomorrow when they announce which banks are adequately capitalized and which banks are not. Portugal, Greece & Ireland are all trading well in excess of the adverse scenarios. Italy is quite close to their adverse scenario assumption.

Assumptions of the 2011 Stress Tests

If the lead-in section of this note hasn't dissuaded you from the Stress Tests' relevance, here's some additional lunacy to consider.

The "Adverse Scenario" in the stress tests makes assumptions around GDP growth, unemployment, home prices, exogenous shocks, and other macro variables. Let's skip straight to the big question: What are the assumptions about sovereign default?

- No sovereign defaults. (No, really.) The adverse scenario does not contain a default of any sovereign issuance. Instead, sovereign "shock" is purely a function of higher interest rates on sovereign bonds and higher credit spreads.

- No assumption of any change in ratings. (Coincidentally, the EU is considering banning ratings agencies.)

- Valuation haircuts are only applied to held-for-trading bonds for each bank - that is, those that are already marked-to-market.

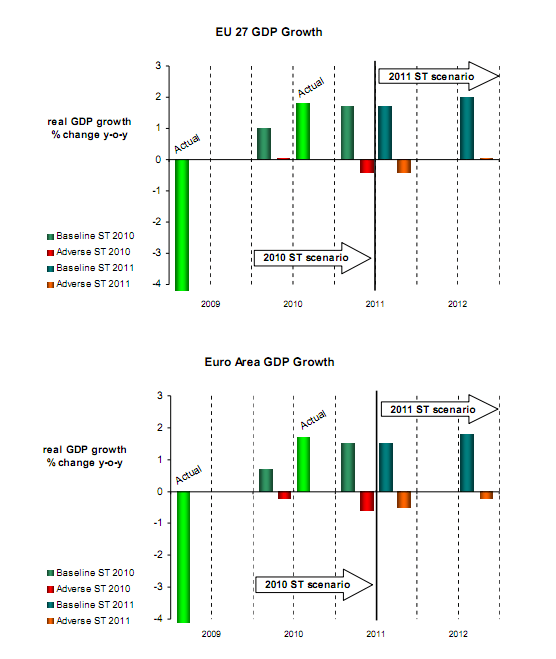

GDP Assumptions

The chart below, from the European Banking Authority, shows the assumptions around GDP growth in the 2010 and 2011 stress tests.

For those interested in the overview of the stress tests, take a look at the following document, which describes in greater detail what we have summarized in this note.

Detailed Disclosures Will Be Forthcoming

One thing the stress tests will provide is a great deal of data for individual banks' exposures (or at least what those exposures were at December 2010). Refer to a disclosure template at the following link:

One side note is that the stress test data will not be comparable to the BIS data that many investors have used to get a handle on exposures. According to the EBA, the data is aggregated in a way that makes reconciliation "impossible."

Market Reaction to 2010 Stress Tests

The chart below shows the Euro STOXX Bank Index back to 2009. The market was in an uptrend at the time of the stress test release, and in the 7 trading days immediately following the July 23rd, 2010 release, the index squeezed 9.2% higher. Today, the index is 24% lower than its level on the day of the release. We think this is probably a good way for thinking about how the stocks will trade again this go-around. Remember, it was clear to everyone last summer that last year's stress tests were also a complete joke. Somehow, this time around, the market seems to think that this round of stress tests is much more serious. While that is clearly wrong, the market may well use it as an excuse to move higher in the short-term.

Conclusion

Based on the fact that it relies on assumptions that border on disbelief, we think clients should treat with extreme skepticism the likely bullish conclusions of tomorrow's EU Stress Tests (Round 2). While it served as a catalyst for the market to go higher in the short-term last summer, those gains proved short-lived as the market went on to retrace all that and more.

Joshua Steiner, CFA

Allison Kaptur