Last week, we saw the biggest diversion between weekly athletic apparel vs footwear sales in six weeks, as ASPs in apparel turned down sequentially by 7.4%, and both footwear units and apparel units and ASPs turned up. We’ll stick with the cliché that one week does not make a trend. But it’s definitely worth noting this especially given that the ICSC index turned positive as well, and the yy comparision for apparel is getting easier on the margin.

Weekly athletic apparel and footwear sales maintain positive underlying momentum following the conclusion of a strong June that was consistent with the rest of retail. While apparel sales reflect a sharp sequential deceleration in both sales and ASPs this week due to challenging one week compares, underlying two-year trends remain steady. Most noteworthy is the continued strength in ASP trends following a more promotional April/May period in footwear at a time when most of retail accelerates discounting ahead of back-to-school. This suggests that margins have likely improved at footwear and sporting goods retailers since May – good for DKS and HIBB, even more favorable for FL and FINL. Here are a few key callouts from the week:

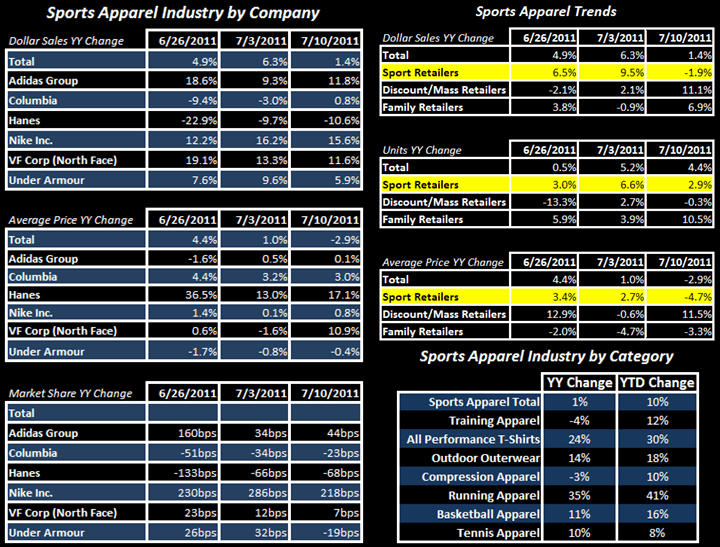

- Following a consistent stretch whereby athletic specialty retailers have outperformed the other channels, the discount/mass channel was the top performing last week. We expect strong yy sales growth in the athletic specialty channel to resume next week.

- For reference, in order to keep underlying 2-year trends in apparel constant with results since May, yy sales growth would have to return to HSD – LDD and ASP to LSD growth levels. With compares getting even more favorable in July after this week, we could see an acceleration of sales into quarter end.

- In apparel, Running (+35%) and All-Performance T-shirt (+24%) categories continue to substantially outperform Compression product (-3%) due in large part to Under Armour diversifying their apparel mix to include non-compression charged cotton product.

- Interestingly, while regional performance data has been temporarily discontinued by SportScan as they integrate new participants into the apparel sample, retailers commonly mentioned particularly strong sales in the Northeast during June. This is in stark contrast to the underperformance in the NE as reported by SportScan in through May – a notable improvement particularly for DKS, which is over-indexed to the region.

- Share gains at Nike in both footwear and apparel in recent weeks is the most notable brand callout. In apparel, these gains are coming largely at the expense of UA as sales of charged cotton moderate and Adidas. In footwear, Skechers, Puma, and New Balance continue to lose share to leading brands. As noted, sales growth of Under Armour apparel has decelerated to mid-to-high single-digits in each of the last three weeks following a run of double-digit growth over the past 3+ months since the introduction of its new charged cotton line.

- As a reminder, monthly footwear data will be out in next week providing additional clarity into sales trends within the athletic specialty channel through the first two months of the 2Q at which time we’ll highlight any changes to our view of expectations.

Casey Flavin

Director