There are a lot of reasons to be concerned about CAKE this quarter, but I think the top line will prevail. Along with the rest of the industry CAKE has outperformed the market significantly this year but in-line with the S&P 500 over the past 5 days. I certainly have my concerns for 2H11, but will address those after the company reports 2Q11 earnings, when I believe they will be more pertinent.

2Q11 SAME STORE SALES TRENDS

- The 2Q EPS estimate is based on an assumed range of comparable sales between 1.5% and 3%.

- CAKE has 1.4% of price on the menu exiting 1Q11.

- Assuming no change in two-year average trends, SSS will be 3.3% for the quarter

- Over the past three quarters, CAKE has benefited from an ongoing improvement in menu mix as beverage sales continued to stabilize.

- Broader casual dining trends continue to improve

EPS ESTIMATES - NOT MUCH UPSIDE

Coming into this year, CAKE had 60% of their costs contracted for. The remaining 40% must be purchased on the spot markets for the balance of the year. As of the last update in April, management guided to approximately 3.5% food cost inflation for the year, with +4.5% in the first half and +2.5% in the back half of the year. The reason for the drop off in inflation in the back half of the year was to come, according to management, from easier dairy cost compares in the fourth quarter. The company does not have dairy costs locked.

Guidance for the 2H11 assumes that commodity prices, dairy in particular, will not be at the high levels we saw in the fourth quarter last year. As the charts below illustrate, dairy costs are currently higher than they were in 4Q10. Of course, there has been significant volatility of late and there is potential for a snap-back. However, management may be forced to revise its expectations with respect to the dairy component of food costs if prices in cheese and milk markets remain anywhere close to where they are currently trending.

POSSIBLE FINANCIAL ENGEERING LURKING IN THE SHADOWS

It seems possible to me that CAKE may announce that it will be returning some excess capital to shareholders. It will likely come in the form of share repurchases and/or a dividend. Currently, the average dividend yields for SBUX, MCD, DRI, and YUM are 1.3%, 2.79%, 2.62% and 2.16%, respectively. CAKE could certainly get to a 2% yield and this would provide some support to the current stock price.

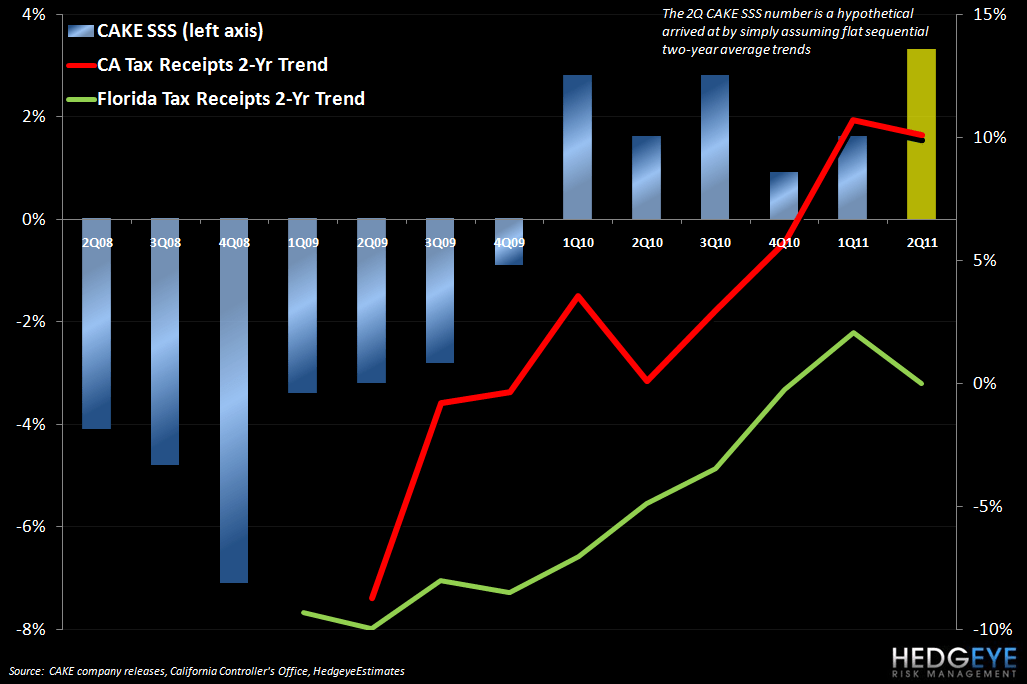

SALES TAX RECEIPTS LOOK BETTER THAN BAD

Sales tax receipts grew in California and Florida on a year-over-year basis. On a two-year basis, as the chart below indicates, there was a sequential slowing in sales tax receipts growth but the slowdown is hardly substantial. California and Florida account for 21% and 13%, respectively, of CAKE’s system units.

Howard Penney

Managing Director

Rory Green

Analyst