Positions in Europe: Long Sweden (EWD); Long Germany (EWG)

Conclusion: Swedish economic fundamentals remain strong (despite being off 2010 levels) and the Riksbank sends a clear message of interest rate tightening to head off inflation. We’re bullish on Sweden’s growth profile, sober fiscal policy, and sovereignty outside of the Eurozone.

We bought Sweden via the etf EWD on 8/9 in the Hedgeye Virtual Portfolio and despite the hit that most European country etfs have taken over recent days on incremental news of Italy’s sovereign debt concerns, we like owning Sweden for a few concise reasons:

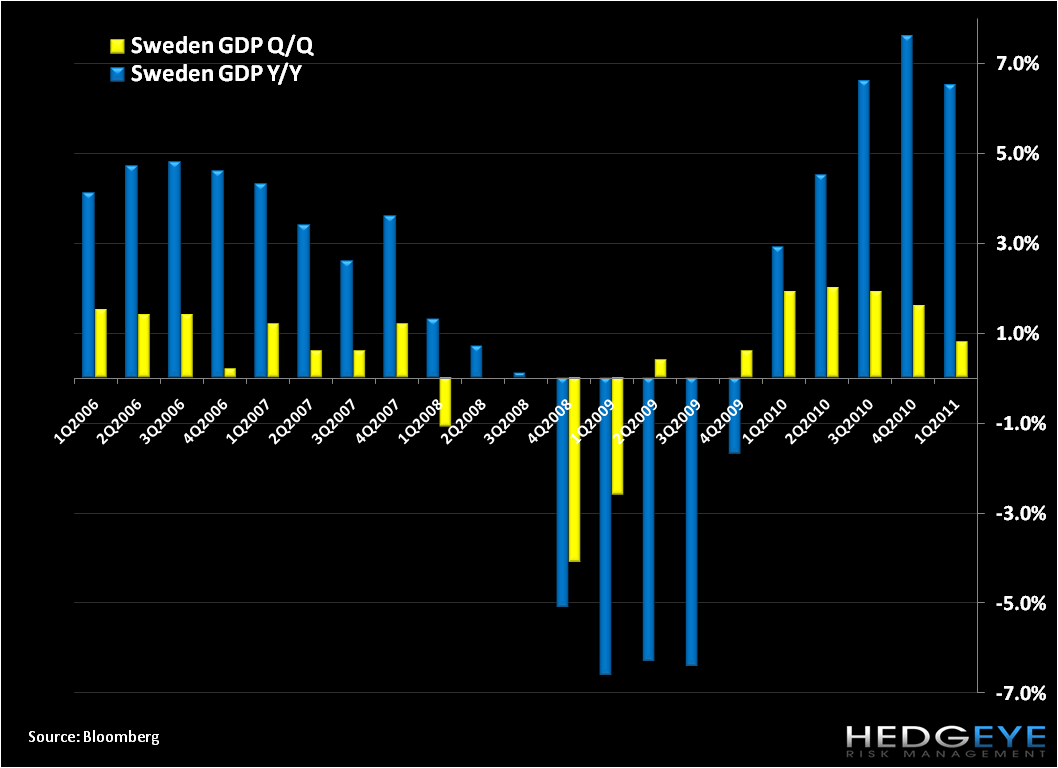

GDP – The country has a healthy growth profile of 4.5% this year. While off 2010’s growth rate of 5.4%, Sweden should continue to run a healthy trade surplus and find strong global export demand, especially considering that ~45% of its exports are destine to markets outside of the EU and therefore not tied to the region’s sovereign debt contagion threats. [For comparison, Eurozone 2011 GDP is estimated at 2.0%].

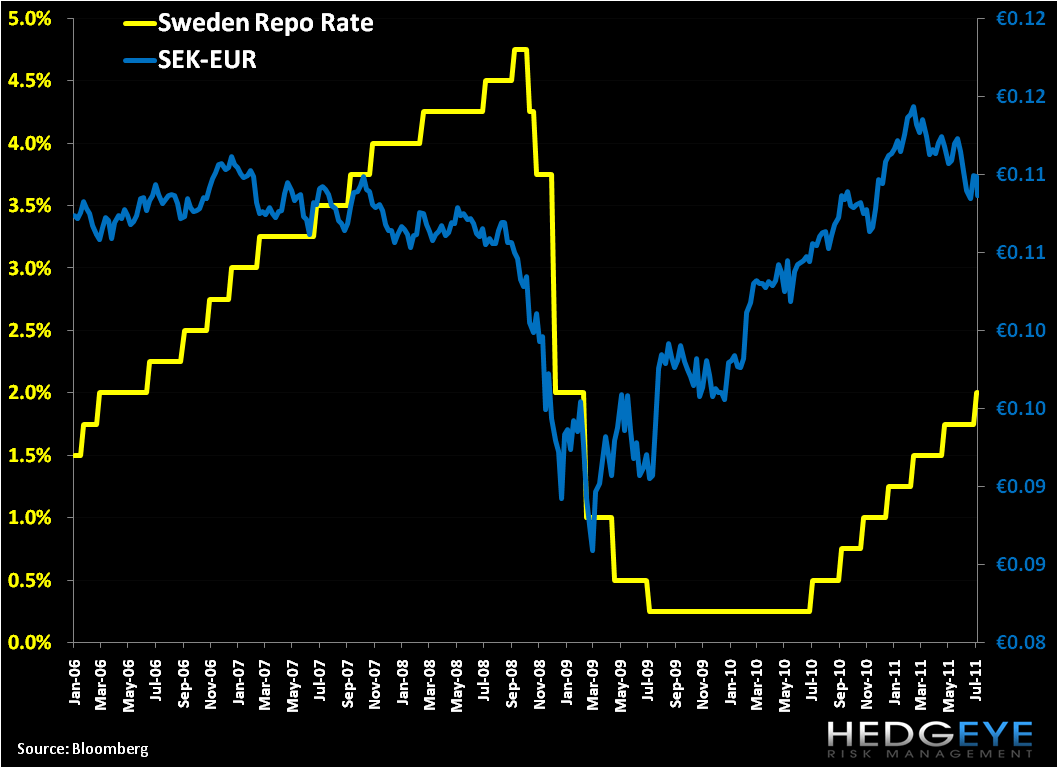

Interest Rates — The Riksbank has proactively raised the benchmark repo rate seven times since July ‘10 to combat inflation, in particular to cool the housing sector. While we haven’t ruled out another 25bp hike into year-end, at 2.00% the Bank has room to cut and maneuver around additional economic headwinds, should they arise.

Inflation – CPI stood at 3.1% in June Y/Y, above the 2.0% target rate, yet the strength of the SEK has helped mitigate imported price inflation, while the statistical office continues to report that domestic cost pressures remain low. As our Q2 theme of Deflation of the Inflation plays out, in particular for food and energy prices, we expect Swedish inflation to move closer to the target; CPI comparisons will also get more difficult as we move in the latter half of 2H2011, which should help to bring down the level.

SEK/Exports — The actions of the Riksbank have strengthen the SEK vs major currencies, and like the CHF, the SEK has provided a safe haven trade as the EUR remains mired in sovereign debt worries. [That said, the SEK has weakened versus the EUR and USD since early March ‘11 and early May ‘11, respectively. YTD the SEK-EUR is down -2.4% and the SEK-USD is up 2.3%]. In general we like the investment profile of a country with a strong currency. While a strong currency is a worry for exporting nations like Sweden, Swedish central bank Governor Stefan Ingves recently stated that the 22% surge in the Krona vs the USD over the past year marks a “normalization” that won’t harm exporters. [We’ve seen a similar positive outcome from Swiss exports despite a white hot CHF vs EUR and USD].

Unemployment – The unemployment rate stands at 7.9% in May, above the 6% level seen before the great recession, but below the Eurozone’s 9.9% or the US’s 9.2%. We think the rate made a top in January of this year and expect the rate to slowly trend lower into year-end.

Risk Metrics – Risk as assessed by sovereign CDS and bond yields is incredibly tame in Sweden, with 5YR Swedish CDS at 32.5bps (vs Germany at 54.3bps, or Greece, Portugal, and Ireland all above 1000bps!). The 10YR yield on Swedish government bonds is 2.686% (vs Germany at 2.711% or Greece, Portugal, and Ireland all over 12%!). Debt as a percentage of GDP is 40% versus 79% in Germany and 144% in Greece. Finally the country is not running a budget deficit.

Headwinds Exist

Despite our bullish outlook on Sweden, it’s clear that growth and optimism are off levels seen in 2H2010. In particular, Sweden’s strong manufacturing sector has slowed, with PMI Manufacturing narrowing to 52.9 in June versus 56.1 in May and Consumer Confidence has dipped, falling to 16.7 in June versus 17.9 in May according to a survey from the National Institute of Economic Research.

Household Credit borrowing also deteriorated, falling to 6.9% in May Y/Y versus 7.2% in April and has trended lower year-to-date. And Retail Sales have declined over the last two months, most recently at -1.1% in May Y/Y.

While we see an independent Swedish bank and currency as a positive, Sweden is not immune to Europe’s sovereign debt contagion, but perhaps just better sheltered. We’ll have to see how sentiment moves on the fiscal imbalances of Italy and Spain, economies far larger with far great banking counterparty exposure than Greece, Portugal, or Ireland.

Below we chart GDP, CPI, and the Riksbank Repo rate for reference.

Matthew Hedrick

Analyst