“Any fool can know. The point is to understand.”

-Albert Einstein

To truly embrace the analytical incompetence of central planners tasked with managing globally interconnected risk, one has to accept that these people are Fiat Fools. Sure, any one of them can know what happened yesterday. But can they proactively predict risk?

We introduced the term Fiat Fool during the initial stage of the European Sovereign Debt crisis (2010). To understand what the Fiat Fools are doing to economies and markets alike, all you have to do is pay attention.

Fiat Fools fundamentally believe that they can smooth economic cycles and tone down market volatility. I guess that’s what the IMF’s latest dudette in Chief, Christine Lagarde, was trying to do this morning when she proclaimed her mystery of faith that “some of the Italian numbers are excellent.”

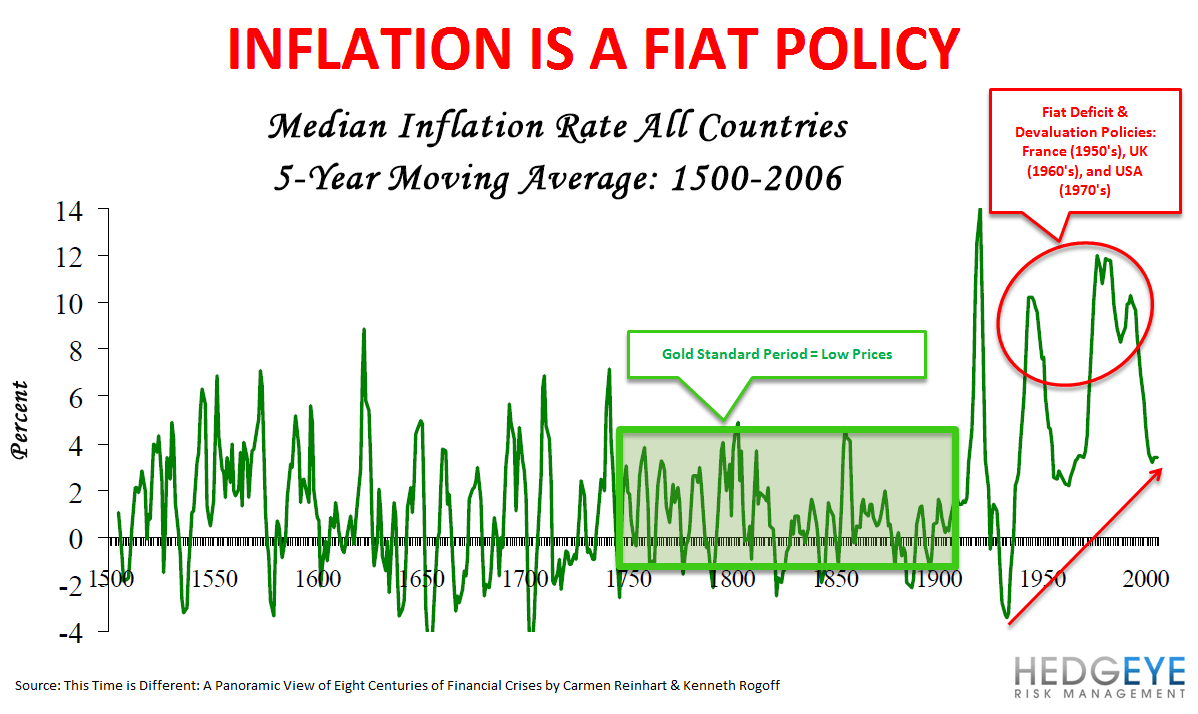

Hedgeye’s long-term conclusion has been that the Fiat Fools do two things:

- They shorten economic cycles

- They amplify market volatility

That’s it. There is no smoothing and toning. There is no “price stability.” And there most certainly is no “full employment.” So, it’s time for La Bernank to unite with his Keynesian storytellers in Europe and admit who they are, and what they do. Greenspan did.

Not that the Obama Administration wants to be held accountable for perpetuating Keynesian Economic Ideologies, but none of these political people who support Bernanke and Trichet should forget what their idol himself admitted to Henry Waxman (under oath) during the thralls of 2008.

HENRY WAXMAN: “Do you feel that your ideology pushed you to make decisions that you wish you had not made?”

ALAN GREENSPAN: “Well, remember that what an ideology is, is a conceptual framework with the way people deal with reality. Everyone has one. You have to -- to exist, you need an ideology. The question is whether it is accurate or not. And what I'm saying to you is, yes, I found a flaw. I don't know how significant or permanent it is, but I've been very distressed by that fact.”

No. I don’t think reminding professional politicians of context and causality is going to change them this morning. Sadly, these people are more concerned with their own career risk management than that of your markets and economy. So onto the next.

Back to the Global Macro Grind…

Here’s our real-time risk management look at Global Equities:

- China was down -1.7% overnight to 2754, barely holding onto our immediate-term TRADE line of support = 2730

- India’s BSE Sensex dropped -1.8% to 18411, barely holding onto our immediate-term TRADE line of support = 18357

- Hong Kong got blasted for a -3.1% drop and remains bearish TRADE and TREND in our model (resistance = 22499)

- FTSE in London is breaking its intermediate-term TREND line of 5897

- DAX in Germany is breaking its intermediate-term TREND line of 7199

- MIB in Italy is crashing, down -22% since its February 2011 high (down another -2% this morning)

- IBEX in Spain looks awful (bearish TRADE and TREND)

- Greek stocks continue to crash (down -31% since their February 2011 lower long-term high), making lower 2011 lows today

- Russian, Norwegian, and Saudi stock markets are all breaking their intermediate-term TREND lines as Oil prices break down

- SP500 TREND line support is under attack in pre-open futures trading (Hedgeye’s line in the sand = 1317)

On the Commodity front, Deflating The Inflation remains our call:

- CRB Commodities Index (18 components) challenged TREND line resistance (349) last week and failed

- WTIC Oil’s TREND line remains at approximately $103/barrel (Goldman is the bull, Hedgeye the bear)

- Wheat and Corn prices are down another -2-3% this morning and have both broken TREND line support

- Cotton prices are getting slammed this morning (down -4%) and should alleviate some cost pressures out there

- Gold looks like a champ (as it usually does when real-interest rates are negative; UST Treasury yields plummeting again)

- Copper is the outlier on the bullish side, holding intermediate-term TREND line support of $4.20/lb

Currency and Credit Markets are all over the place:

- European Sovereign CDS in Spain and Italy are pushing toward (or above in Spain’s case) the critical Lehman Line of 300bps

- Italian Bond yield at Italy’s 12 month debt auction came in a lot higher sequentially versus last (3.67% vs 2.15%)

- EUR/USD is getting annihilated after breaking what we’ve called out as critical intermediate-term TREND support ($1.43)

- US Dollar Index is making a big bid for a TRADE and TREND breakout – this will continue to Deflate The Inflation

- US Treasury yields are all breaking down through TRADE and TREND line support (like they did in May-June)

- US Treasury Yield Spread continues to compress; 10-year minus 2-year yields = 250 basis points wide (long FLAT)

All the while, this morning’s high-frequency economic data was what I consider fine. Chinese Money Supply Growth (M2) came in at 15.9% (it’s been proactively cut in HALF by the Chinese since we got bearish on China at the end of 2009). Meanwhile German, French, and British Consumer Price Inflation (CPI) readings for June were benign enough to provoke Europe’s Fiat Fool in Chief to stop raising rates.

As for the Fiat Fools having anything in the area code of a modern day real-time risk management process, you can bet your Madoff that they don’t have one. Nor do they have any experience managing any of the aforementioned globally interconnected risk where it matters – on the tape.

My immediate-term support and resistance ranged for Gold, Oil, and the SP500 are now $1, $92.96-96.74, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer