We have aggregated the Consumer sector into fourteen sub-sectors in the table below.

The table shows performance of each sub-sector and highlights moves by sub-sectors that are more than one standard deviation from the mean return of the fourteen sub-sectors. As the key at the bottom of the table describes, a number highlighted in green indicates a return greater than one standard deviation above the mean return of the fourteen sub-sectors. Red indicates one standard deviation below. Additionally, the best and worst performing stocks in each sub-sector, for each period, are highlighted in the divergence rows of the table. The consumer space has been on a tear since last year with Restaurants, Autos & Auto Parts, and Department stores leading the way.

Looking at the table below, it is clear to see that over the past six months restaurant stocks (both Quick Service and Full Service) have led the way. The laggards over the first half of 2011 have been the Food Processors ($6 corn is a problem) and Homebuilders (we continue to be very bearish of the housing market). In addition to the Restaurant sector, Footwear Apparel Specialty retail and Department Stores have been strong performers over the past six months.

Overall the performance has been very strong over the past six months; nine of the fourteen buckets shown below have returned double-digit gains.

Looking at the performance over the past three weeks Food Tobacco and the Discount stores are stand outs to the downside, while Full Service Restaurants, Auto & Auto Parts, Apparel Specialty Retail and GLL have been strong.

In terms of outliers, Hedgeye’s recent consumer ideas feature heavily. In Restaurants, KONA has outperformed over the last two, three and four weeks. KONA continues to be one of our favorite ideas. Concern around the resignation of former CEO Marc Buehler has largely been eased and the company’s reimaged stores are set to provide a boost to comps starting in 4Q. RUTH has also performed strongly over the past week and is trading at a large discount to the space.

CBRL is a favorite idea of ours on the short side. This is a company that has grown its store base by 11% since the beginning of fiscal 2007 and, over the same period, seen sales grow by 2.3% and EBIT remain essentially flat. While gasoline prices have declined sharply since May, the year-over-year increases in gasoline prices remain significant and 2Q results from CBRL will certainly be impacted by the high gasoline prices. Another of Hedgeye’s favorite ideas, EAT, has returned 74% over the last year. Our thesis one year ago was that sales would be choppy for a few quarters, but that comps would ultimately improve and margin enhancements, coupled with share buybacks, would drive EPS growth.

COSI stands out as a disappointment when looking at the performance over the past six months, but I remain convinced that the fundamentals of the company’s performance will continue to improve and reported sales trends for 2Q will be strong.

In gaming, MPEL has been a firm favorite of our GLL Team for some time now. Their conviction in MPEL’s prospects in Macau is strong and, additionally, their estimates are ahead of the Street for the second quarter. WMS has been the laggard in the space and Hedgeye GLL has expressed concern about WMS in the short-term (while favoring IGT and BYI), while remaining positive on the slot-supplier sector over the long-term.

In retail, Specialty Apparel has been performing strongly over the past one, two, three, and four weeks. Over these durations, the returns of the space have been more than one standard deviation above the average return of the sub-sectors. While Department Stores have been performing largely in line with the broader consumer space, JCP, one of our favorite ideas on the short side in the Retail space has been working well. JCP has been underperforming the category over the past one, two, and three weeks.

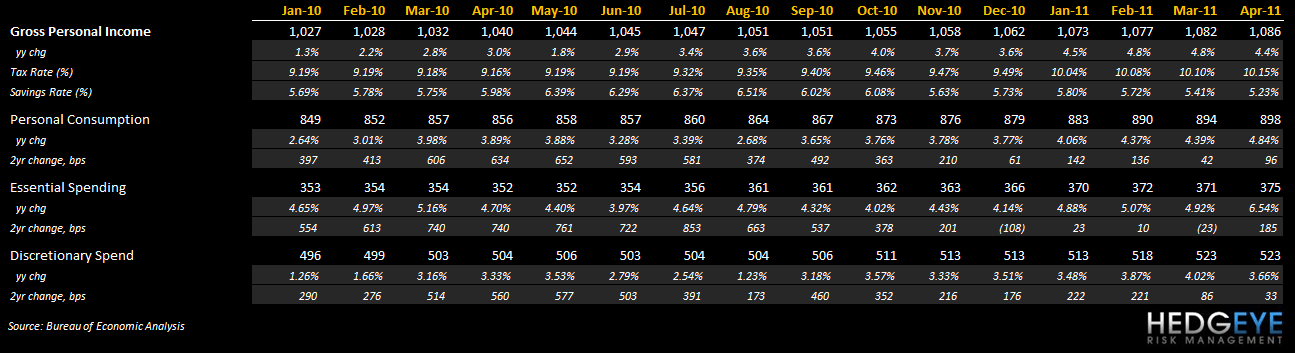

Thanks in no small part to continuing government support, the monthly PCE data shows, personal income, consumption and expenditure accelerated in January and have been growing robustly in 2011. More recently, we have seen a slowdown in two-year trends in April, as the slowing discretionary spending could be linked to the spike in gas prices that peaked in May.

Howard Penney

Managing Director

Rory Green

Analyst