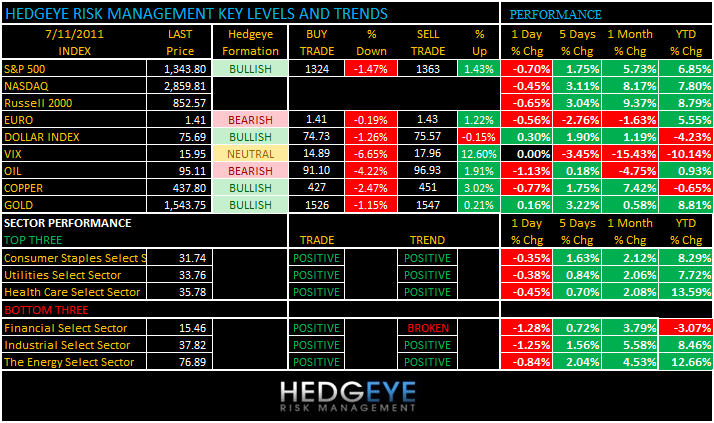

TODAY’S S&P 500 SET-UP - July 11, 2011

As we look at today’s set up for the S&P 500, the range is 39 points or -1.47% downside to 1324 and 1.43% upside to 1363.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -1202 (-2926)

- VOLUME: NYSE 771.13 (-8.57%)

- VIX: 15.95 YTD PERFORMANCE: -10.14%

- SPX PUT/CALL RATIO: 1.65 from 1.15 (-44.05%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 22.57

- 3-MONTH T-BILL YIELD: 0.03%

- 10-Year: 3.03 from 3.17

- YIELD CURVE: 2.63 from 2.68

MACRO DATA POINTS:

- 11 a.m.: Export inspections: Corn, soybeans, wheat

- 11:30 a.m.: U.S. to sell $27b in 3-mo., $24b in 6-mo. bills

- 4 p.m.: Crop conditions

WHAT TO WATCH:

- Ruth’s Hospitality (RUTH) may rise as much as 40% in next 18 mos. as economy rebounds: Barron’s, citing Rollins Capital

- Morgan Stanley (MS) may be attractively priced after 27% plunge from its Feb. high: Barron’s

- European officials meet today to consider how to dig Greece out of its financial hole; meanwhile markets are battering bonds of Spain, Italy

- Williams board was expected to meet yesterday about whether to raise its bid for Southern Union, CNBC reported. SUG trading ~5% above Energy Transfer’s offer price

- Monsanto, Sinochem said to be in advanced talks over strengthening ties between cos.: WSJ

- “Transformers: Dark of the Moon” top-grossing film at U.S., Canadian theaters for second weekend, taking in $47m

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Copper May Decline on Concern Sovereign-Debt Crisis Might Spread to Italy

- Gold May Advance for a Sixth Day as Growth Concern Fuels Demand for Haven

- Wheat Drops as India May Allow 2 Million Tons for Sale to Foreign Buyers

- Sugar Drops as Sovereign-Debt Crisis May Spread to Italy; Coffee Slides

- Platinum Eyes ‘Top End’ of India’s Mass Bullion Jewelry Market, Group Says

- Monsoon Rain Covering India a Week Early Boost Crops From Rice to Soybeans

- Tin Exports From Indonesia Jump to Highest Level Since 2009 as Rain Eases

- Codelco Miners Fight Job Cuts in Company’s First General Strike Since 1993

- Palm Oil Stockpiles in Malaysia Climb to 18-Month High on Increased Output

- Copper Imports by China Climb for First Time in Three Months on Stockpiles

- Gillard Hits Miners as Bond Spreads Widen Most in Year: Australia Credit

- Hedge Funds Raise Bets on Gasoline After Retail Price Drop: Energy Markets

- Bangladesh Plans to Buy More Wheat for Welfare Programs, State Agency Says

- Steel Beating Oil on China Demand Spurs Metalloinvest Debut: Russia Credit

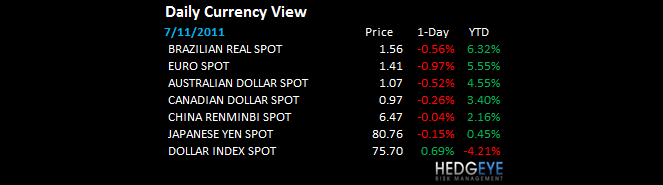

CURRENCIES

EUROPEAN MARKETS

- EUROPE: just a mess this morn; FTSE and DAX holding TREND, but Greece and Spain in particular look awful; Finland down 1.6% to -14% YTD

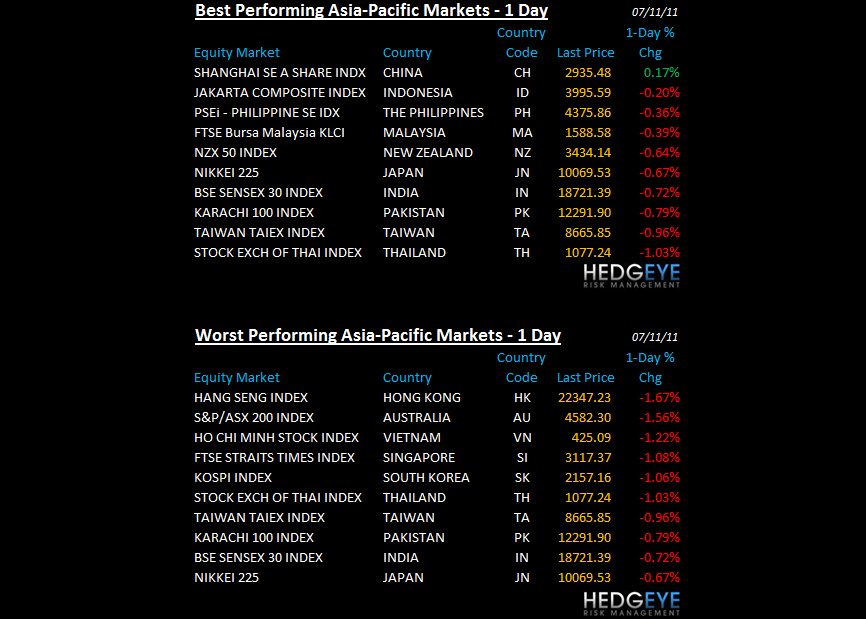

ASIAN MARKETS

- ASIA: overdue correction across the board except China (we're long) which closed up +0.18%; KOSPI and Sensex holding TREND support

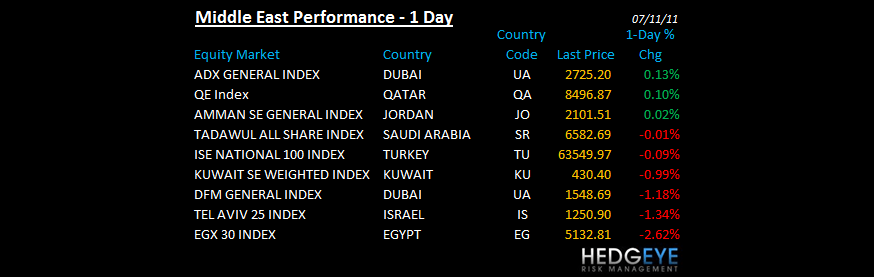

MIDDLE EAST

Howard Penney

Managing Director