Employment data a mixed bag for restaurants.

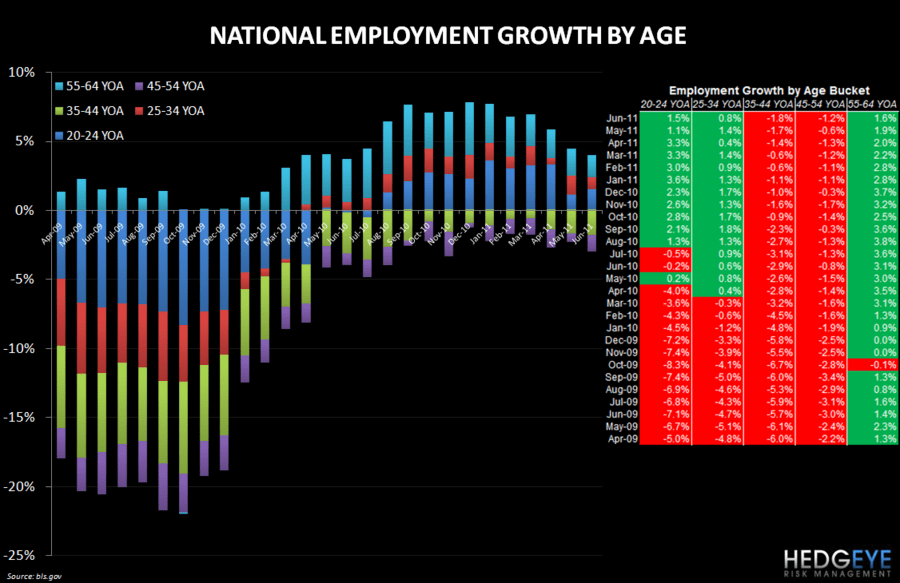

The overall jobs picture this morning was unambiguously awful and the unemployment rate has ticked up to 9.2%. The level of growth in employment among the 20-24 years of age cohort accelerated in June, which is a positive data point for QSR. May employment growth among this age cohort came in at a meager +1.1%. June’s employment level for 20-24 year olds grew 1.5%.

Overall, the jobs report was clearly worse-than-expected. The other four age cohorts we show in our chart, below, all show sequential deterioration in employment growth. As a reminder, much of the positive sentiment from management teams over the past number of quarters as been based upon an improving employment landscape. Equally, much of the improvement in consumer confidence surveys that has occurred has been driven by improving expectations, rather than current situation perceptions, and the slide in employment levels will likely weigh on expectations.

As the second chart, below shows, employment growth in the food service industry continues to be robust but there was an interesting slowdown in Full Service employment growth in May. This data lags the employment by age data by one month. The May Full Service slowdown may prove to be immaterial but, since late 2010, Full Service employment growth has lagged Limited Service employment growth. If this divergence were to become more pronounced, we would take it as being suggestive of slowing trends in casual dining versus quick service. The employment by age data for June, additionally, would corroborate this idea. The space has been on fire and we would need further confirmation from this and other factors to become more bearish, but these two data points are noteworthy this morning.

Howard Penney

Managing Director

Rory Green

Analyst