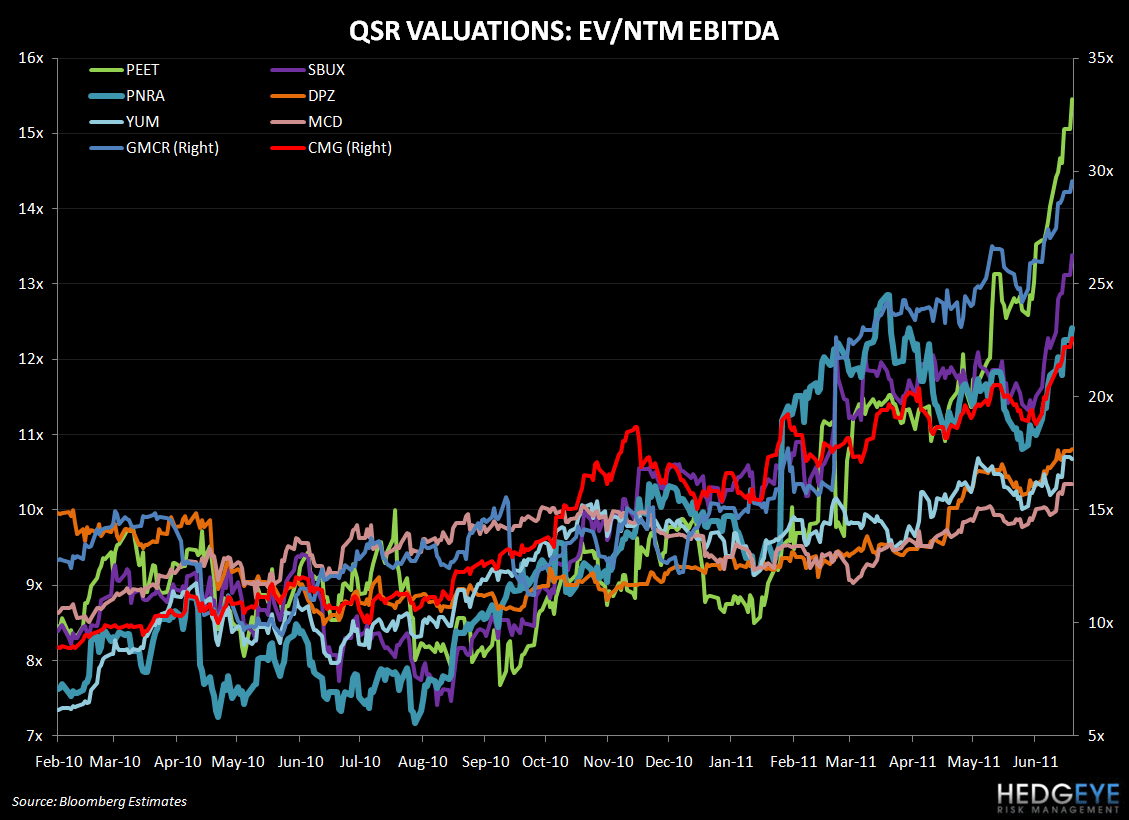

I have never seen so many restaurant companies trading at 10x EV/EBITDA or better.

Every day I open my industry valuation models and, of late, I have been amazed to see the number of companies trading at double digit EV/EBITDA multiples. As of today, there are ten companies with that distinction. In the past, a double digit cash flow multiple was reserved for those companies that demonstrated 15-20% unit growth or had an international presence that made it look more like a consumer multi-national.

Coming out of the Great Recession, the industry is being revalued despite some serious headwinds. The double digit valuations are being achieved despite rampant food inflation, which has traditionally has caused investors to flee from the space (especially the more mature names).

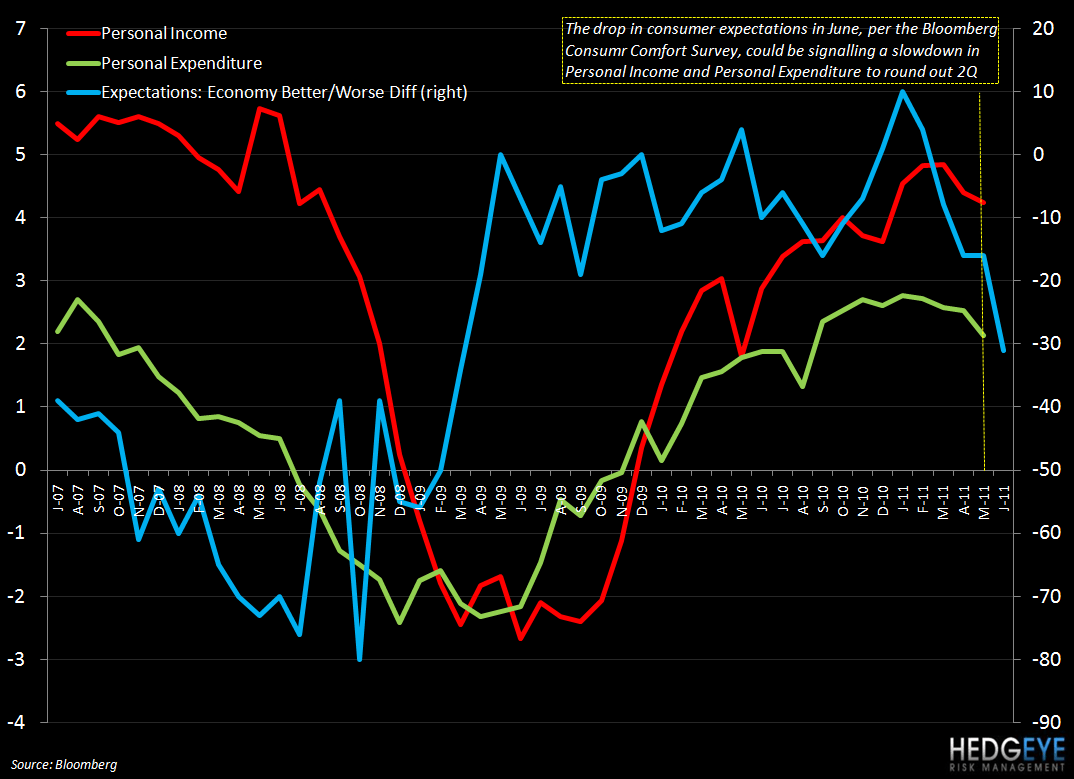

This is also inconsistent with traditional measures of future demand like consumer confidence, which has flat-lined since 2009. More importantly the small improvement in consumer confidence since bottoming in late 2008 has been driven by the expectations component which is now rolling over. Not surprisingly, we are now starting to see personal income and spending roll over too.

While overall demand for eating out is holding up, all of the restaurant companies that are valued by the street with double-digit cash flow multiples have seen same-restaurant sales slow on a one-year basis. Looking at two-year trends, however, paints a more positive picture. Two-year average trends are improving and much of the decline in one-year comps may be due to difficult compares.

On the positive side, restaurant companies have not been raising prices as aggressively as supermarkets and reduced spending on other more “durable” categories is helping maintain the consumer’s frequency of eating out. The industry is not overly levered and the cash flow generation, dividend yields and high margin franchises business models of some of the more mature companies are very attractive.

With this being said, when trying to justify a revaluation of a business or an industry, there is an acute risk of stretching the facts. The rolling over of consumer expectations is a concern for me, as are the peak multiples being awarded to restaurant companies at the present time.

Howard Penney

Managing Director

Rory Green

Analyst