Make That $60B?

The New York Post is out this morning saying that the servicing settlement will be much larger than previously reported. The settlement will be $55-60B, not the $20B previously rumored, according to "sources close to the discussion" cited by the Post. The money would be applied to restitution for harmed borrowers, civil penalties, and 51 funds - one for each state plus a national fund - for regulators to use at their discretion. These discretionary funds could be used to do principal reductions, although the banks and some AGs worry that principal reductions for delinquent borrowers will create a moral hazard for borrowers who are still current.

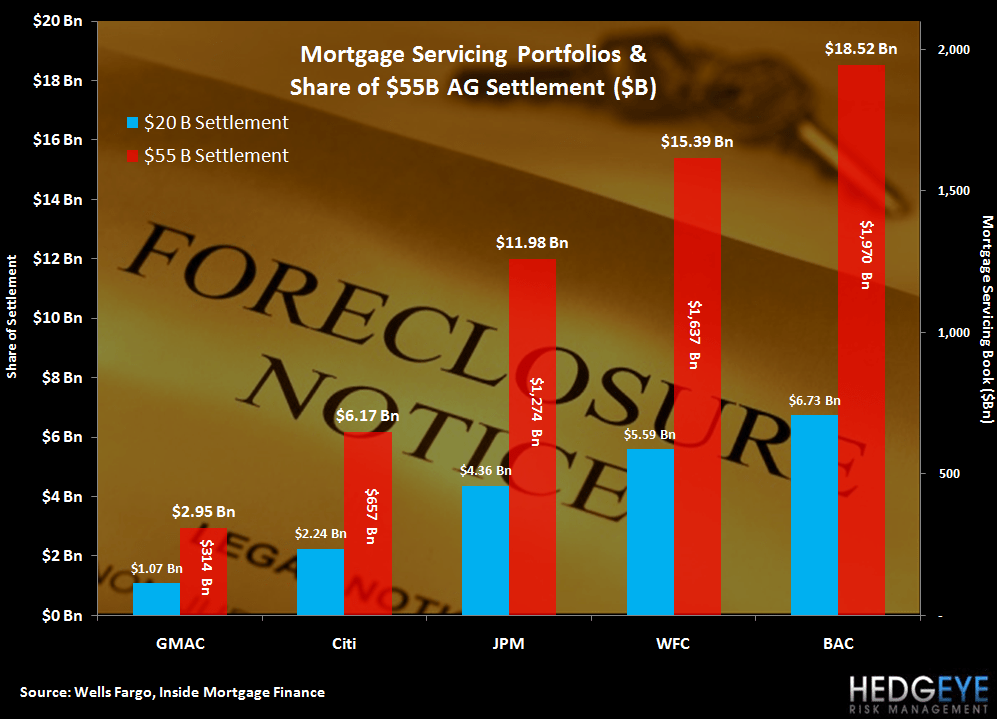

We have used the top five servicers' market share to determine their possible liability. The chart below shows the mortgage servicing market share of the top five banks, which collectively control 60% of the market, as of 2009. BAC is the largest servicer, with Wells Fargo in second place. For purposes of this calculation, we are assuming that the settlement amount is $55B and is split on a pro rata basis according to market share among the top five servicers.

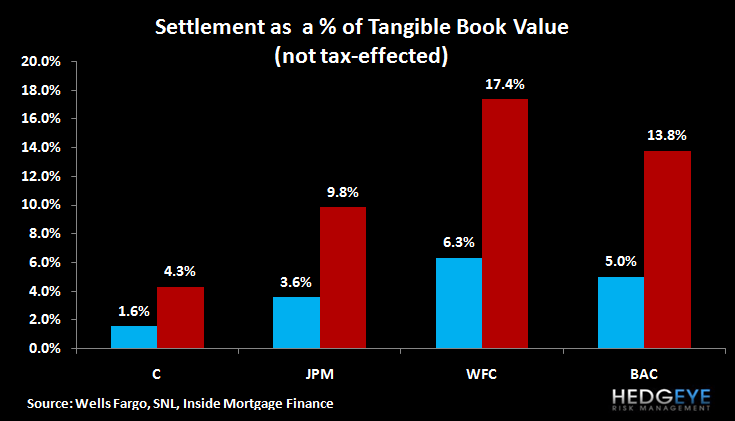

To put these levels in context, a $18.5B settlement from BAC is equal to 14% of their tangible book value, while WFC's penalty would be 17% of tangible book. That said, it's likely that any penalty would be due over a period of time, rather than in a lump sum. It's also likely that national regulators would be partially motivated by safety and soundness of the financial system, and would be averse to a settlement so punitive that banks would require recapitalization.

Joshua Steiner, CFA

Allison Kaptur