In the May 27th issues of the Hedgeye Edge I included BWLD as one of my top ideas. While it’s still a name I like, we need to start looking at taking some of the chips off the table.

Within the Casual Dining names, year-to-date, BWLD is the third-best performing name after RRGB and BJRI, up 52.7%. This outperformance has been driven by the company being revalued in the marketplace; over the past 6 months BWLD has seen consensus EPS rise 7.5% (RRGB, MRT, DIN and EAT all had even better revision trends than BWLD) and its forward NTM P/E multiple 45%. At the very least, the performance of BWLD is telling you that the NFL lockout will end soon and not disrupt sales trends in 4Q11.

The sell-side sentiment monitor still stands at a bullish reading of 58.8% buys (was 55.6% in January 2011; while the buy-side sentiment reading (Bloomberg short-interest ratio) has decline from 8.47 in January to 7.29 currently (was 12.44 last August).

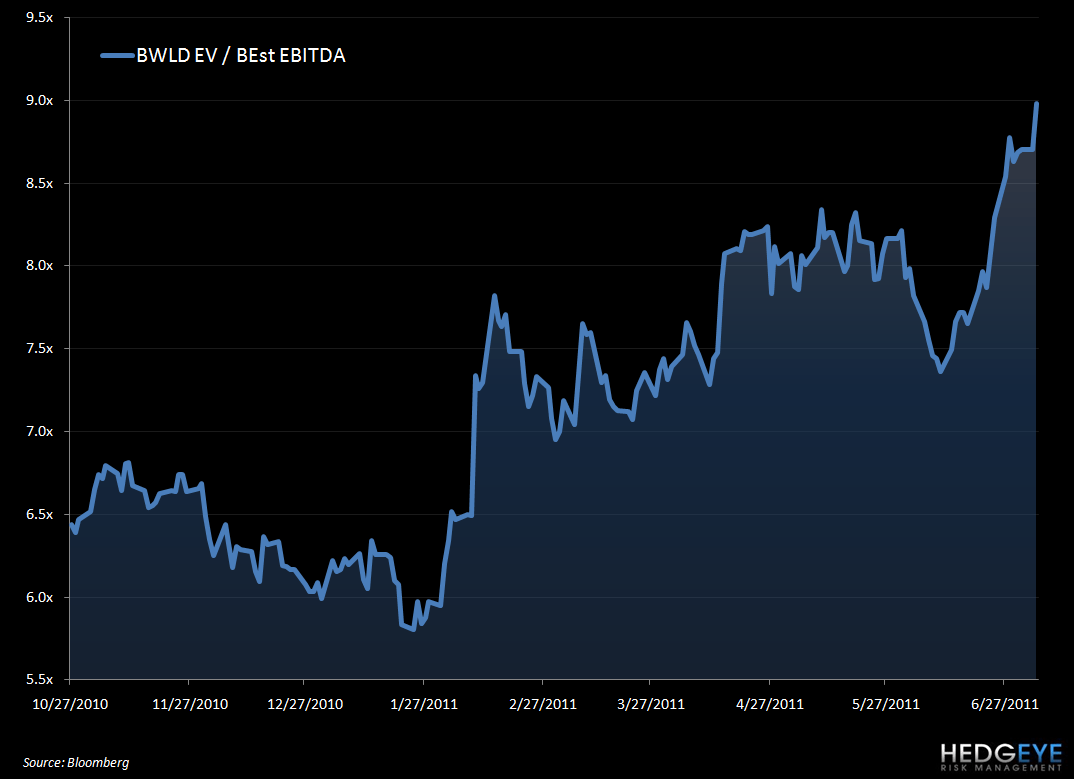

Year-to-date the stock has worked with very little support from the sell-side and the shorts have been covering on the back of better-than-expected sales and earnings driven in part by lower food coast, among other things. Trading at 9.1x EV/EBITDA, there is about $7.06 (10.7%) of upside if the market revalues the stock to 10.1X EV/EBITDA (and there is no more upward revisions to EPS).

We have been pointing out recently that the top-line is, by far, the most important metric investors are considering at the moment and, with respect to this view, we believe BWLD will report a strong 2Q11. Depending on how strong comparable restaurant sales are for 2Q, 3Q could see a sequential deceleration on one- and two-year average trends.

Regarding food costs, BWLD will be lapping the benefit of lower chicken wing prices in approximately six months. Below, I discuss more in depth the sales and margin trends.

BWLD same-store sales trends:

Although April same-store sales trends were up an impressive +5.3%, it is important to remember that the company was lapping an easy comparison from April 2010, when comparable sales declined -3.7%. This +5.3% growth implies a 120 bp slowdown in two-year average trends from two-year average trends in the first quarter. I would expect to see two-year trends slow somewhat during the second quarter, given the slower start to the quarter and the decreased level of pricing during 2Q11 of 1.9% relative to 2.4% in 1Q11.

Management also stated that incremental gift card redemptions benefited same-store sales growth by about 60 bps during the first quarter, which will likely not be as beneficial going forward. That being said, the same-store sales growth comparison gets easier in 2Q11, so comparable sales growth should continue to be strong on a one-year basis. I am currently modeling a +3.0% comp for the second quarter.

The year-over-year comparison gets increasingly more difficult come the third quarter and if the company does not implement another price increase (management said it has not yet decided whether it will take any further menu price increases), pricing will decrease to +1.3% in the second half of the year. Assuming no disruption to the NFL season, I am currently modeling a 1.5% comp for the third quarter and +4% growth during 4Q11.

During the first quarter, average weekly sales at company units outpaced same-store sales growth by 390 bps. I would expect company average weekly sales to continue to outpace comparable sales growth as management continues to close underperforming restaurants (the company said it will close or relocate 8 older units) and new unit performance is strong.

BWLD Restaurant-level Operating Margins:

Restaurant-level margins improved about 360 bps YOY during the first quarter. The bulk of that YOY growth was driven by lower traditional wing prices (traditional wings accounted for 20% of sales), which were down 36% YOY during the quarter. Accelerated same-store sales growth on both a one-year and two-year average basis also contributed to the company’s increased operating leverage.

Given that traditional wing prices averaged $1.02 per pound during the first two months of the second quarter (down 33% YOY from 2Q10’s $1.51 per pound cost and down nearly 22% on a two-year average basis), BWLD should continue to see significant favorability on the COGS line for the remainder of the year. As a percentage of sales, the YOY favorability should moderate, however, as traditional wing prices peaked during 1Q10.

Partially offsetting the COGS benefit, BWLD experienced higher labor expenses during the first quarter which management attributed to higher training costs related to its new menu rollout and increased hourly wages as the company invested in speed of service initiatives. The incremental training costs will roll off during the second quarter but management still expects to experience higher hourly expenses; though it said continued leverage of management wages should result in flat YOY labor expenses as a percentage of sales. I am modeling some slight deleveraging of the labor expense line during the second quarter given my assumption that same-store sales trends will moderate slightly from the first quarter on a two-year average basis.

All in, I think restaurant level margins will continue to improve for the remainder of the year; though 1Q11 should prove to be the high point from a YOY basis point growth standpoint. Management’s full-year EPS target of more than 18% growth should be easily achieved, assuming no major NFL disruptions (I currently forecasting full-year EPS growth of nearly 22%). I would not be surprised to see 2Q and 3Q11 earnings fall short of that annual goal, however, largely as a result of the expected significant YOY jump in preopening expenses during those quarters.

Howard Penney

Managing Director

Rory Green

Analyst