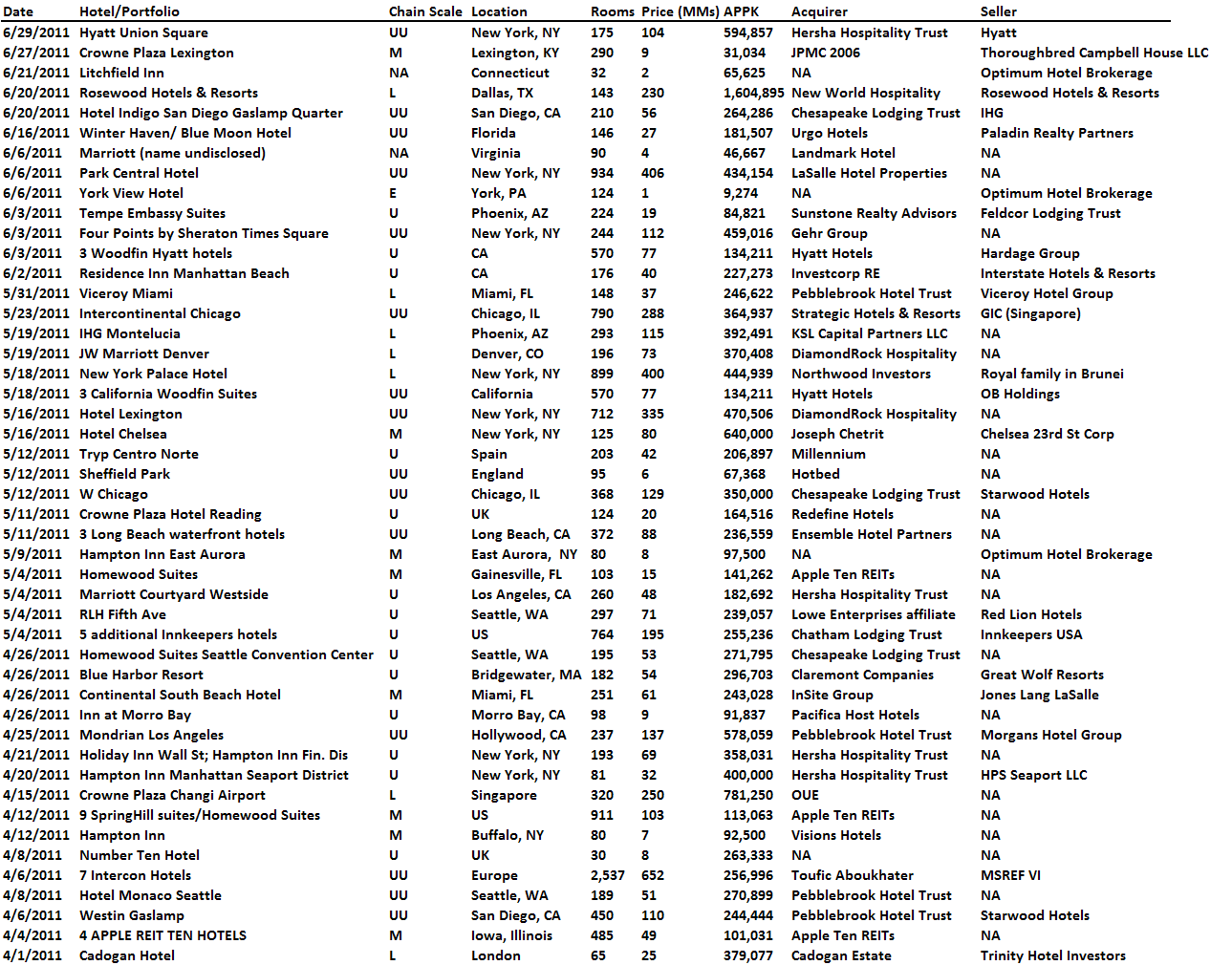

Hotel transaction market continues to chug along at a good pace.

Market M&A Trends for Q2

- Q2 US hotel transaction volume neared $4BN, lower than the ~$5BN seen in 1Q but enough to surpass all of 2010’s total volume.

- Q2 US Upper Upscale Hotel Volume declined 30% QoQ but the number of transactions doubled and Average Price per Key grew 12% QoQ in Q2.

- No surprise, REITs continued to dominate the M&A market in Q2; however, we did see a handful of transactions by Hyatt and Starwood.

- There were more portfolio deals relative to Q1.

- Hotel delinquencies have stabilized. The latest data from Fitch showed Q2, as of May, hotel delinquencies hit 13.9%, a little better than Q1’s 14.3%.

- CMBS loans are seeing 60-70% LTV with 5-year terms of between 5.5% and 6.5%.

- Rates on three- to five-year, fixed-rate deals, with 50% to 65% LTV, are in the 5% range.

- Lenders were more likely to fund longer-term (10-year) deals.

Luxury Segment

- Average Price per Key

- Q2 2011 Global average: $546,628

- US average: $611,871 (5 transactions)

- Q1 2011 Global average: $279,697

- US average: $289,733 (4 transactions)

- Q2 2011 Global average: $546,628

Upper Upscale Segment

- Average Price per Key

- Q2 2011 Global average: $320,937

- US average: $327,187 (13 transactions)

- Q1 2011 Global average: $257,295

- US average: $291,945 (7 transactions)

- Q2 2011 Global average: $320,937