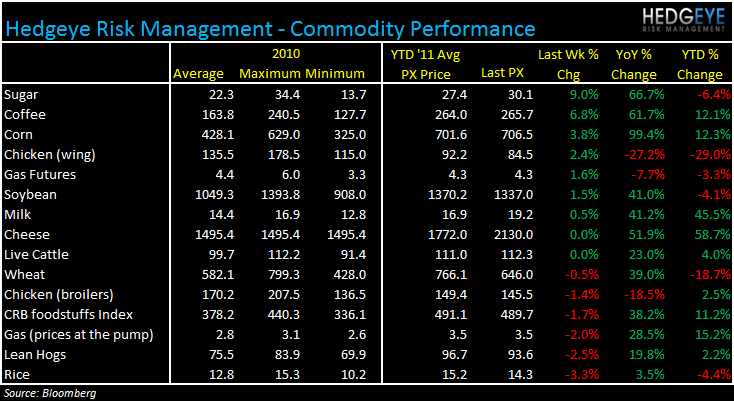

As the dollar has gone down week-over-week, the up-moves in agricultural commodities were more pronounced than the down-moves. Coffee, sugar, corn, and chicken wings all led the way, while rice and pork declined week over week. Heading into earnings season, it will be interesting to take stock of companies’ updated full-year commodity inflation guidance versus what it was at the time of the last earnings call. Some companies, like CAKE, are not guiding to realistic levels of inflation, in our view.

COFFEE

Coffee prices are up 6.8% over the past week as rising demand and higher fuel costs continue to impact the price of the commodity. For the coffee concepts, SBUX, PEET, GMCR, MCD, DNKN, CBOU, and THI, rising commodity costs are a serious concern. While some of these companies have prices locked in, to the extent that contracts may be coming up for renewal, prices are likely to burden restaurant-level margins sooner or later. Below is a selection of comments from management teams pertaining to coffee prices from recent earnings calls:

- PEET (5/3/2011): We believe we're better off lowering our earnings guidance by $0.10 this year and continuing with the plans we have in place than we would be curtailing spending activity or taking extraordinary pricing action that would be inconsistent with our long-term business interests, and the more sustainable long term cost of coffee we foresee. As a result, you will see throughout our call today that we have a very strong performing fundamental business, but we have to buy some unusually high priced coffee in the short term, then we're not going to do unnatural things in reaction to an unnatural market environment short term. Hedgeye: prices were sliding as the dollar caught a bid but, over the last couple of weeks prices have swung higher again. While it seems that prices may have been “unusual”, this elevated level of pricing may persist for longer than expected.

- GMCR: (5/3/11): Before closing, I also want to touch on rising coffee costs and the effect of our business. Like others in the industry, we are closely watching coffee prices. When we announced our last price increase in September of 2010, coffee prices had increased roughly 30% from $1.45 to $1.90 per pound over the course of roughly three months. Since then, costs have continued to escalate, recently hitting historic highs of more than $3 a pound, a nearly 60% increase since September. In attempt to offset rising green coffee costs, as well as increases in other input costs, we are currently in the process of raising prices for all packaged types. We expect that consumers will see an increase of approximately 10% at the point-of-purchase as the result of this price increase. We expect to see the full benefit of this price increase during our fiscal fourth quarter of 2011. We generally fix the price of our coffee contracts three to nine months prior to delivery so that we can adjust our sales prices to the marketplace. Hedgeye: Coffee has backed off the “historic” high of more than $3 per pound but is still at $2.60 plus and up over the last couple of weeks. Demand remains strong; without a rising dollar, expect price to continue to pressure retailers.

- SBUX (4/27/11): Regarding coffee costs, as I have indicated previously, we have fully locked our coffee costs for 2011 and are price-protected for a couple months into fiscal 2012. As we progress through the balance of 2011, we will progressively take actions to secure our coffee needs and lock coffee costs for additional months into 2012. While we expect that the costs we pay for coffee may be higher in '12 than they are in '11, we remain confident that we can offset those increased costs and preserve our long-term earnings growth targets. Hedgeye: SBUX is confident that it can pass on price and offset coffee inflation with other efficiencies. It is interesting that it expects higher coffee prices in 2012 than in 2011, which would somewhat contradict PEET’s assertion that in May that prices at the time had been unusual. SBUX expects worse prices to come.

CORN

Corn prices have bounced significantly of late as the dollar has declined, expectations of harvests in 2011 have dipped, overly moist fields have deterred farmers from planting, and ethanol production continues has depleted supplies. Corn is an important commodity for the broader restaurant industry because it is used as feed by meat producers. As prices in corn accelerate, it supports prices in beef, chicken, pork, and other meat markets. Below is some recent management commentary pertaining to corn prices:

- CMG (4/20/11): The only things we have locks on corn for most of the year, rice for the entire year, our tortillas and beans for most of the year as well. Hedgeye: CMG will likely have to renew any corn contract at a level far higher than the one it currently holds.

- MCD (4/21/11): And so if the commodity markets move significantly from here and the main ones obviously looking at beef, looking at corn, wheat, coffee, et cetera, our guidance reflects where the markets are today. Hedgeye: Looking at where the prices of these commodities have gone since this quote, one would have to think guidance for commodity costs are going higher.

CHICKEN WINGS

Chicken wing prices are ticking higher, as we have expected them to do – summer generally brings an uptick in prices as demand picks up. See the chart below. BWLD is certainly in the clear for 2011 but, the question mark as we progress through the back half of 2012, will be on prices in 2012.

- BWLD (4/26/11): For cost of sales, the traditional wing market continues to be favorable and the price of chicken wings for the first two months of the second quarter is averaging about a $1.02 per pound, which is lower than any quarterly price since 2003. It compares to last year’s average price for the second quarter of $1.51. Our Boneless Wings contract is extended through March of 2012 at flat pricing to 2010. Hedgeye: Traditional wings count for 20% of restaurant sales and boneless wings count for 19%.

Howard Penney

Managing Director