We track initial claims as an early read into bank credit, as initial claims are a good indicator of frequency for delinquencies. This morning, we are adding bankruptcies to our weekly report. Bankruptcies help predict net charge-offs (since a consumer who declares bankruptcy sees card debt move straight to charge-offs without necessarily passing through delinquent buckets). The chart below shows bankruptcies from January 2009 through May 2011. On a year-over-year basis, bankruptcies continue to improve, dropping 16% in May. This is a positive sign for bank credit in 2Q as well as for the health of the consumer.

Initial Claims Remain Flat - Again - As QE2 Ends

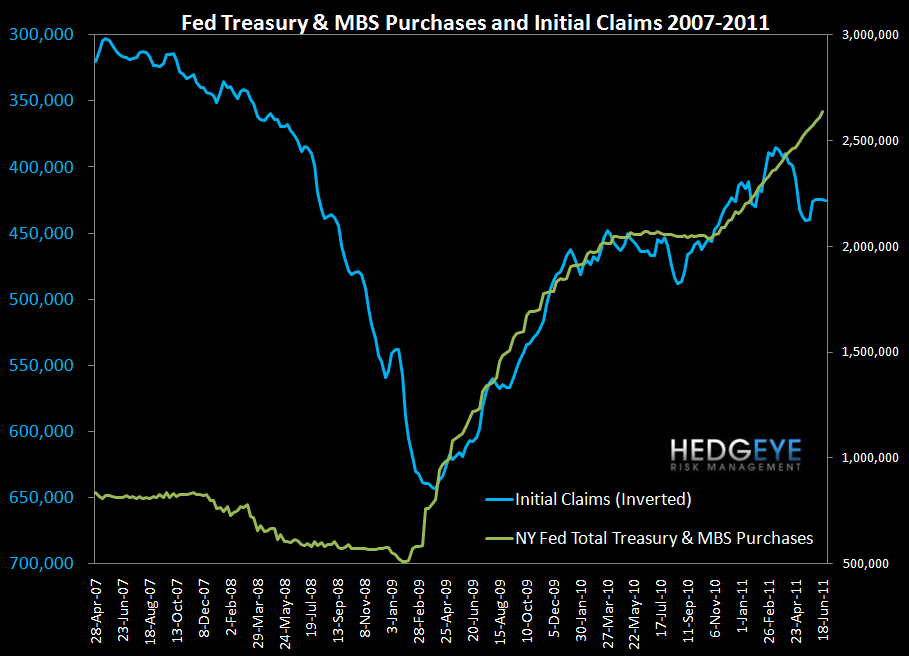

Initial claims were close to flat last week, dropping just 1k to 428k. This is the fifth week in a row that the 4-week moving average has been almost exactly flat. We have been noting for some time that claims stopped going down and started going sideways when QE1 ended. We'll begin to see the effect of QE2's end over the coming weeks, but the early read is not positive. Claims have now been higher than they were at the start of the year for nine consecutive weeks.

2-10 Spread Close to Flat Week Over Week

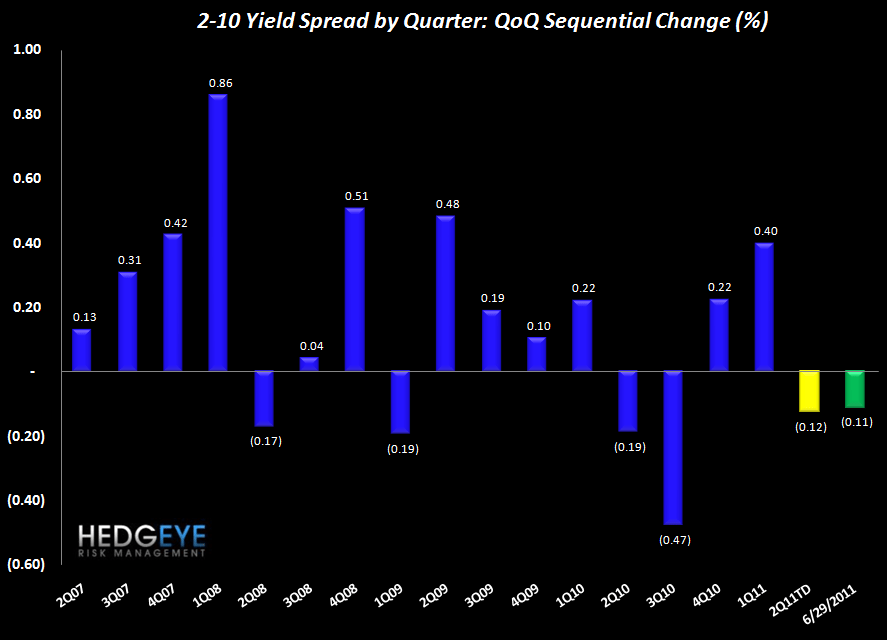

We track the 2-10 spread as a proxy for bank margins. This week's level of 264 bps is up slightly from a level of 261 bps.

Financials Subsector Performance

The chart below shows the price performance of subsectors over four durations.

Joshua Steiner, CFA

Allison Kaptur