“If it ain’t broke, don’t fix it”

-Bert Lance, former OMB Director under President Carter

The current Debt Ceiling Debate ongoing in Washington, DC has largely gone unnoticed by investors. The conventional wisdom appears to regard the daily back and forth between Democrats and Republicans with only passing interest. As the Sector Head for Healthcare here at Hedgeye, what may be a curious side show to many, has deep implications for investment decisions today.

Many news stories have struggled to understand Wall St.’s complacency toward the debt ceiling debate. On the one hand, and in the face of warnings from Secretary of Treasury Geithner, who has made multiple statements regarding the “economic catastrophe” that follows if Congress fails to raise the government’s ability to borrow above $14.3T by August 2nd, there has yet to be the US equivalent of the Greek CDS chart. Senator John Boehner, the Republican Majority Leader in the Senate, called the August 2nd deadline “an artificial date created by the Treasury secretary.” It may just be that we’ve seen this movie before and all know the ending.

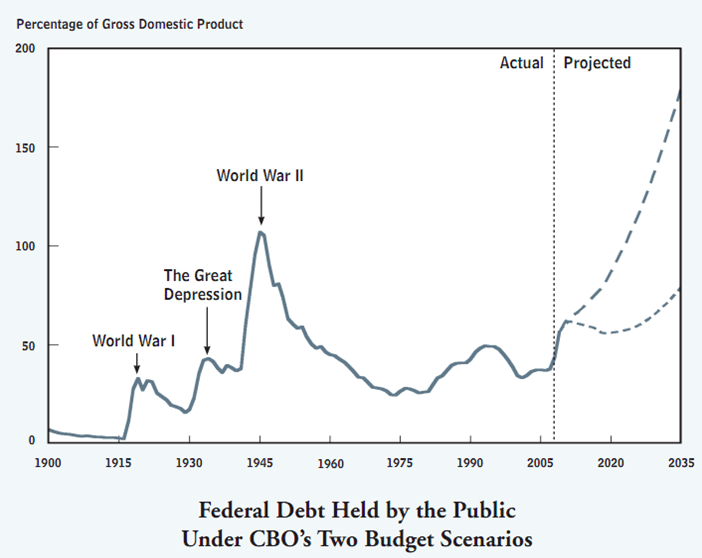

Republicans and Democrats have staked out their respective Debt Ceiling positions by centering on Medicare. It makes sense to focus on Medicare. Medicare spending is the fastest growing and single largest (54%) outlay within Health and Human Services (HHS), the federal department which consumes the largest percentage of federal outlays (23%). To put this in context, Defense (16%) and Treasury (14%) are number 2 and 3, respectively. The Congressional Budget Office (CBO), in their more reasonable ‘Alternative Fiscal Scenario’ outlined in their ‘Long Term Budget Outlook’, chart the widening gap between federal income and outlays due entirely to accelerating growth in Medicare spending.

The current Debt Ceiling debate has been decades in the making as government outlays for Medicare and Medicaid have grown substantially since 1960. Indeed, over the life of available data (since 1960) we’ve witnessed a discrete, secular cost shift away from the individual consumer towards their employer and increasingly towards federal & state sources. National Health Expenditure data from the Center for Medicare Studies, the agency that administers Medicare and Medicaid, show government sourced dollars have grown from ~20% of total spending to 49%, while Private sources, which include out-of-pocket and Private Health Insurance, have gradually shifted from ~75% to 51% over that same timeframe . Moreover, Out-of-Pocket expense as a percentage of Total Private Sources has declined from 47% to 12% over the same time period.

Despite the rapid growth in total medical spending, the Healthcare Economy in the United States by many measures and opinions is broken. The cliché is to state that we spend far more per capita ($7,290) than any other developed nation ($3,700) yet regularly rank poorly for statistics such as life expectancy (42nd), level of health (72nd), and health system performance (37th), at least according to the World Health Organization. The rebuttal is that the US healthcare system is better than any in the world, provided the patient carries health insurance and can pay. But even here, Americans look unfavorably on their health insurance carriers. According to a December 2010 Gallup survey, 56% percent of those surveyed thought the health insurers as fair or poor at providing their service. Poor health outcomes is the routine reality for the upwards of 50M people not lucky enough to have health insurance to complain about. For all the money spent, these statistics suggest we could do better as a country with the dollars spent.

The Affordable Care Act (ACA), also know widely as Health Reform, attempted to correct many of the issues listed above; by expanding insurance coverage, building tools to control costs, and cutting the federal deficit by $143B over ten years. Unfortunately, the fix may actually be making the problem worse.

The ACA expands coverage by expanding Medicaid by raising the poverty limit to qualify, offering tax credits to small firms to offer health insurance, and providing subsidies to individuals and families to purchase their own insurance on an Insurance Exchange. It saves money by encouraging the formation of Accountable Care organizations, provider groups who will share in the savings they generate while providing care audited for quality. The ACA, according the CBO, cuts the federal deficit by lowering Medicare outlays, particularly to private insurance companies who offer Medicare Advantage.

Since President Obama signed the ACA into law many of the underlying assumptions are coming undone. The ACA “froze” the benefit level states offered under Medicaid, but in recent months, and as states grapple with peak budget shortfalls in 2012, they are looking to cut Medicaid expenses, their second highest expense. In the last few days, both Democrats and Republicans have publicly contemplated allowing the states to lower eligibility and provider rates under Medicaid. ACA looks likely to expand Medicaid coverage from a much lower run rate.

Additionally, 1433 companies (representing 3.5M insured lives) have sought and received waivers from HHS to avoid complying with ACA insurance rules. The Obama Administration has since stopped granting waivers.

Accountable Care Organizations were touted as capable of reducing costs and increasing quality, but this plan too has faltered. After a steady stream of providers formed ACOs prior to the proposed rules offered to govern them, the concept has run up against the reality of foregoing revenue while incurring costs to comply with the rules set to govern them. At this point, even the 5M lives estimated by the CBO to be cared for in an ACO appears aggressive.

Recently, the news has turned to a discussion of the Insurance Exchanges, slated to begin offering insurance in 2014, corporate tax credits for offering insurance and the number of people who already have insurance through their job. McKinsey conducted a controversial survey of employers which suggests a significant percentage of employers (30%+) stop offering health insurance for their employees and pay the smaller penalty set out in the ACA. A larger than expected coverage drop will increase the government cost of subsidizing health insurance through the planned subsidies. The CBO currently expects 1M out of a total population of 163M to lose employer health insurance.

Douglas Holtz-Eakin went further with his estimates and calculated the penalty-insurance cost gap would induce employers to drop an additional 38M workers from employer sponsored plans and onto Insurance Exchanges. This is in addition to the number and subsidy cost of Insurance Exchange participants the CBO estimates, 19M and $450B over 10 years. With an additional 38M lives, the Insurance Exchange Hotltz-Eakin estimates the subsidy cost will rise to $1.4T, driving the ACA deep into the red. We have invited Douglas Holtz-Eakin to speak on a call with our clients July 13, and I am looking forward to learning more about his analysis.

The Insurance Exchanges should not present a significant problem as long as the transfer from employer plans to the Insurance Exchanges is 100% efficient. Similar to the corporate penalty-cost of insurance spread, the individual mandate that compels purchase of health insurance has a very low penalty that starts at $95 for individuals in 2014. Assuming that just 5% of young healthy employees, who are high margin since they don’t incur many costs, decide to pay the penalty, this leaves a higher cost population behind. Those that remain will have to pay higher premiums, drawing more subsidies per member, raising the deficit impact, and inducing more individuals to forego insurance, and so on.

While the Debt Ceiling debate goes largely unnoticed today, and may yet be pushed to another day, the day of reckoning approaches for the Health Economy. Government, corporate, and individual pressures to contain costs will eventually lead to slower growth and margin pressure. Medicare and Medicaid will need to be cut, the penalties and taxes raised to corporations and individuals, and more aggressive cost control measures put in place. In the interconnected Health Economy, the ensuing revenue and margin pressures will pose a challenge to everyone; it’s just a question of when.

Thomas Tobin

Managing Director, Healthcare

Source:CBO