This note was originally published at 8am on June 23, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Confusion now hath made his masterpiece!”

-William Shakespeare

So… according to La Bernank in his Fed Presser yesterday, US Growth Slowing As Inflation Accelerates is “part temporary” … but “part longer lasting”… and while “we don’t have a precise read on why”… we are confident that the entire market should trust our forecasts for growth to re-accelerate.

Ben Bernanke’s growth forecasts haven’t been sort of wrong in 2011 - they have been wrong by almost a half! So how can a country that was founded on such fiercely independent principles put up with this level of analytical incompetence from its economic Central Planner in Chief?

I don’t know. But after doing a full day of meetings with major money managers in NYC yesterday, I can tell you that Keynesian Confusion is starting to breed contempt. Dollar Debauchery was all good and fine, until people stopped getting paid.

What we do know is that economics, never mind Keynesian economics, is a social science (Mr. Krugman, that’s different than a hard science, fyi). We also know that market-based practitioners who apply math to markets make a living off of the academic dogma of Keynesian economists.

This is great for my Research and Risk Management business – but really bad for the US economy. My team and I get paid to be right. These guys at the Fed get paid what they’d be worth to an asset management firm managing Globally Interconnected Risk - not much.

Back to this morning’s Global Macro Grind…

USA

- CURRENCY – we’ve had a bullish bias towards the US Dollar since the beginning of June; now the USD Index is breaking out above its $74.41 immediate-term TRADE line of support. This is bad for asset prices that are highly correlated (inversely) to the US Dollar.

- TREASURIES – we’ve been bullishly positioned on the long-term Treasury (TLT) side of the bond market since May. Yes, we understand that bond yields are low – but we think they are going lower – primarily because people aren’t yet Bearish Enough on US Growth.

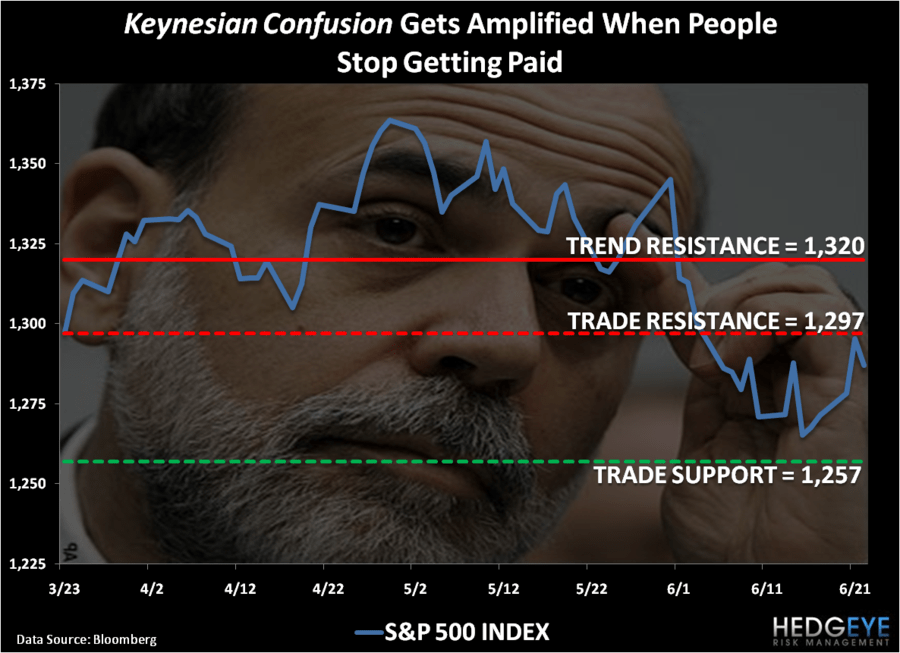

- STOCKS – we re-shorted the SP500 (SPY) at 3:14PM EST on Tuesday, June 21st ahead of the Greek confidence vote in socialism and La Bernank walking down this forecasts for US Growth. Timing matters.

EUROPE

- CURRENCY – having a bullish bias towards the US Dollar (with near-term catalysts that are USD bullish – QG2 ending, a mid-July Debt Ceiling compromise) is reason enough to be bearish on Euros. But the bigger bear brewing in the FX market is Europeans behaving European on go- forward monetary policy. There’s an increasing probability that the ECB considers going for a hybrid version of Quantitative Guessing II.

- EUROCRAT BONDS – plenty of European Sovereign bonds look like the Sovereign Debt Default Cycle is just getting started. If you think this is isolated to Greece, market prices are pricing in the other side of that thought. Major risks – and they are not going away anytime soon.

- STOCKS – we are long Germany (EWG) and short Spain (EWP). Germany’s PMI (Producer Manufacturing) print slowed significantly in June (54.9 versus 57.7 in April) and we’d be unaccountable to not call that data point out for what it is – Growth Slowing, globally. Across European Equities, the only major market that has not broken its intermediate-term TREND line yet is the German DAX (7103 support), but it’s close!

ASIA

- CURRENCY – since one of our Q2 Macro Theme remains “Deflating The Inflation”, we finally sold our 2-year (buy and hold!) long position in the Chinese Yuan (CYB) this week. We think Asian currencies will weaken as commodity inflation does. Don’t forget that most of these countries (China, Australia, India, etc.) have been vigilant in raising interest rates – now they can stop with that.

- CHINESE STOCKS – after being bearish on China for the last 15 months, we’ve been on the road articulating the research scenario analysis around A) Chinese Growth Slowing At A Slower Rate and B) Chinese Inflation Deflating. The research and the risk management calls are two very different things (one is research, the other timing), but we did finally buy exposure to the A-shares on June 16th and we are in the money. Despite the Keynesian Confusion, Chinese stocks were up +1.5% last night and have been up for 3 consecutive days, outperforming most of the majors in Global Equities.

- JAPANESE STOCKS – we remain long-term bears of the gigantic Keynesian Experiment in Japan and we remain short of Japanese Equities (EWJ) here. Yes Japanese stocks are down -6% YTD and, yes, they had a natural disaster. But the real long-term disaster in Japan is that the average annual GDP Growth rate since 1992 has been 0.85%. Bernanke would be less confused if he embraced Richard Koo’s economic ideas about “Balance Sheet Recessions” and what perpetuates them (cutting rates to the ZERO bound and scaring the hell out of your people).

COMMODTIES

- OIL – we remain on the other side of Goldman’s call to buy oil and see immediate-term downside in WTIC Oil to $91.22 this morning.

- GOLD – we remain long Gold (GLD) and think it will continue to perform as long as real-interest rates in America remain negative.

- COPPER – we remain respectful of Dr. Copper’s Ph.D in the antithesis of Professor Bernanke’s confusion. Bearish TREND is as bearish does.

Otherwise, in the land of nod, it’s a pretty quiet morning. We don’t see any probability of Keynesian Confusion leading to any level of American style accountability and/or change in whatever it is that they do to come up with these embarrassingly bad forecasts.

My immediate-term support and resistance ranges for Gold, Oil and the SP500 are now $1533-1555, $91.22-95.98, and 1257-1297, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer