Notable news items and price action from the restaurant space as well as our fundamental view on select names.

MACRO

The health of the consumer is a key question right now as chains pass on price in an effort to protect margins due to elevated input costs. Chipotle is the latest concept to make headlines for raising prices (see below). Of course, unless commodities prices decline, we can expect price increases across the industry.

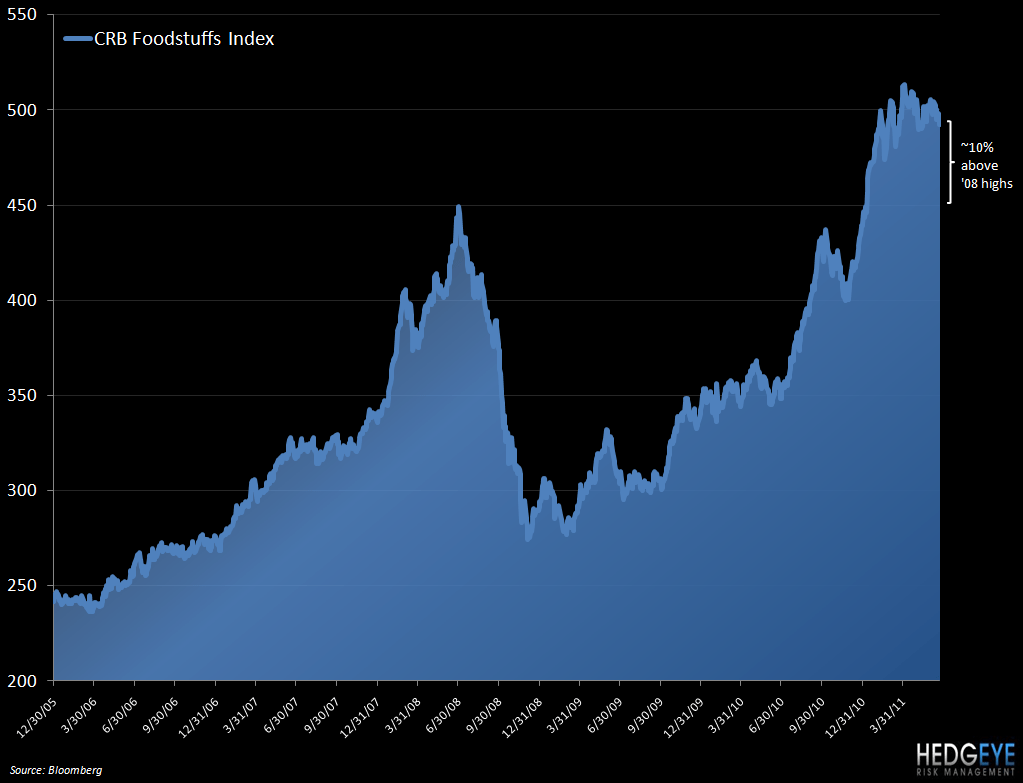

Food costs have declined somewhat but, as the chart below indicates, the CRB Foodstuffs Index remains far above historical norms.

QSR

- CMG is raising prices regionally after saying on its February 20th earnings call that no price increase would be considered until the third quarter. A few days shy of the third quarter rolling around, the company has decided that it will raise menu prices in the Northeast and Southeast over the next few weeks with changes in other markets to follow. According to The Wall Street Journal, NYC Chipotle restaurants increased prices by 50 cents last week, but lines were still “out the door”.

- MCD has expanded its smoothie line with a mango pineapple flavor as it looks to emulate its success of 2010 in selling beverages.

- MCD earned the title of “Most Effective Brand” in the inaugural Effie Effectiveness Index, which ranks brands by measuring the results of 40 worldwide marketing and advertising competitions.

- WEN Chief Operating Officer, Andrew Skehan, was surprised to learn of the scantily clad models hired to greet reports at the first Wendy’s restaurant in Russia last week. The Russian initiative was somewhat of a departure from the wholesome, pig-tailed, red-haired icon usually used to promote Wendy’s.

- THI was restated “Buy” at BofA with a price target of C$55.

CASUAL DINING

- EAT was mentioned on a list of potential M&A candidates by UBS.

- DRI will report a solid 4QFY11 on June 30th, according to JPM, based on recent industry sales trends and company-specific cost savings.

Howard Penney

Managing Director