TODAY’S S&P 500 SET-UP - June 27, 2011

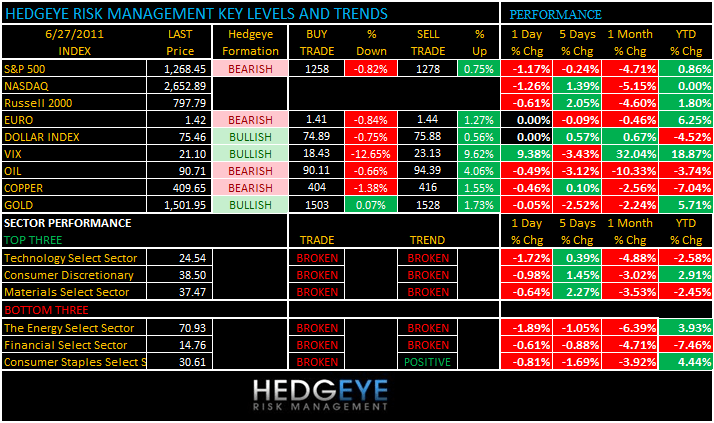

Ahead of the likely sluggish income and spending numbers, futures are modestly higher. Asia-Pacific stock markets posted losses overnight except China (we are LONG) and Europe was higher in the early morning. As we look at today’s set up for the S&P 500, the range is 20 points or -0.82% downside to 1258 and 0.75% upside to 1278.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -838 (-352)

- VOLUME: NYSE 1740.41 (+55.74%)

- VIX: 21.10 +9.38% YTD PERFORMANCE: +18.87%

- SPX PUT/CALL RATIO: 2.11 from 2.41 (-12.30%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 23.61

- 3-MONTH T-BILL YIELD: 0.02%

- 10-Year: 2.88 from 2.93

- YIELD CURVE: 2.53 from 2.58

MACRO DATA POINTS:

- 8:30 a.m.: Personal income, est. 0.4%, prior 0.4%

- 8:30 a.m.: Personal spending, est. 0.1%, prior 0.4%

- 10:30 a.m.: Dallas Fed, est. (-3.2), prior (-7.4)

- 11 a.m.: Fed’s Kocherlakota speaks on leverage in Montana, audience Q&A

- 11 a.m.: Weekly export inspections (corn, wheat, soybeans)

- 11:30 a.m.: U.S. to sell $27b 3-mo. bills, $24b 6-mo. bills

- 1 p.m.: Fed’s Hoenig speaks in Washington, audience Q&A

- 1 p.m.: U.S. to sell $35b in 2-yr notes

- 4 p.m.: Crop conditions

WHAT TO WATCH:

- Greek lawmakers begin 3-day debate on austerity package

- “Cars 2” from Disney’s Pixar opened as the top film in U.S., Canadian theaters this weekend, collecting $68m in ticket sales

- President Obama meets with Senate leaders to see if they can restart the deficit/debt talks that fell apart last week

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Longest Losing Streak Since 2008 Ending for Commodities as Futures Surge

- Bread in Japan Becoming Costlier May Curb Purchasing Power, Slow Recovery

- Commodities Tumble to Five-Month Low on Basel Rules, Greek Austerity Vote

- Oil Slides on Outlook for Slower Demand as IEA May Release More Stockpiles

- Copper Falls as Greece’s Debt Crisis May Curb Demand for Industrial Metals

- Smithfield Foods’ Hunger for Bacon Makes Sara Lee Merger Target: Real M&A

- Gold Pares Drop After Reaching 1-Month Low on Dollar’s Gains Against Euro

- Cocoa Climbs as Purchasers Secure Mid-Crop Supplies; Sugar Prices Decline

- Wheat, Corn Drop as Greek Debt Woes Cut Investor Appetite for Commodities

- Food Crisis Cooperation ‘Doomed’ Unless Action Taken, Warns Kofi Annan

- Shanghai Sea-Cargo Volume to Increase 10% Annually as Plants Move Inland

- Speculators Cut Agriculture Bets as Improving Weather Eases Supply Concern

- Copper-Alloy Product Output From Japan Climbs as Demand Begins To Recover

CURRENCIES

EUROPEAN MARKETS

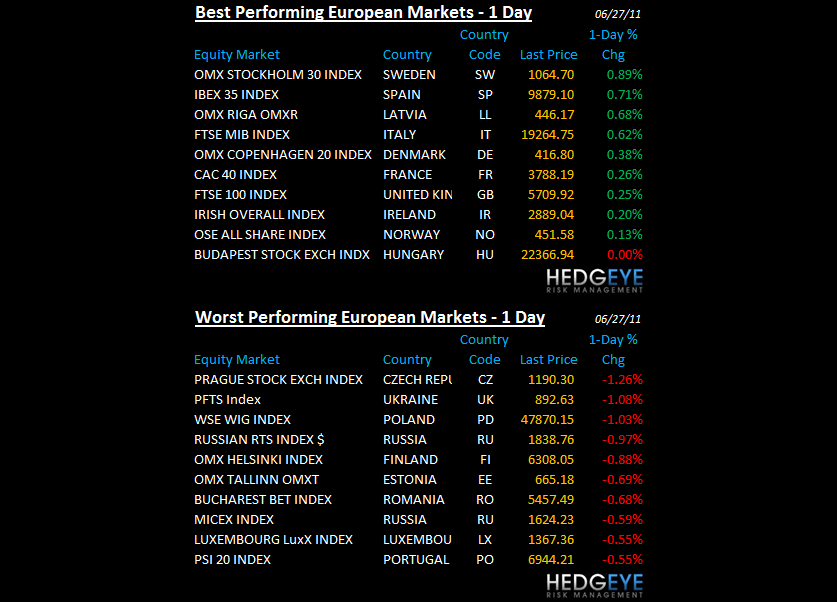

- Europe is generally higher lead by Span (we are short) and Italy.

ASIAN MARKETS

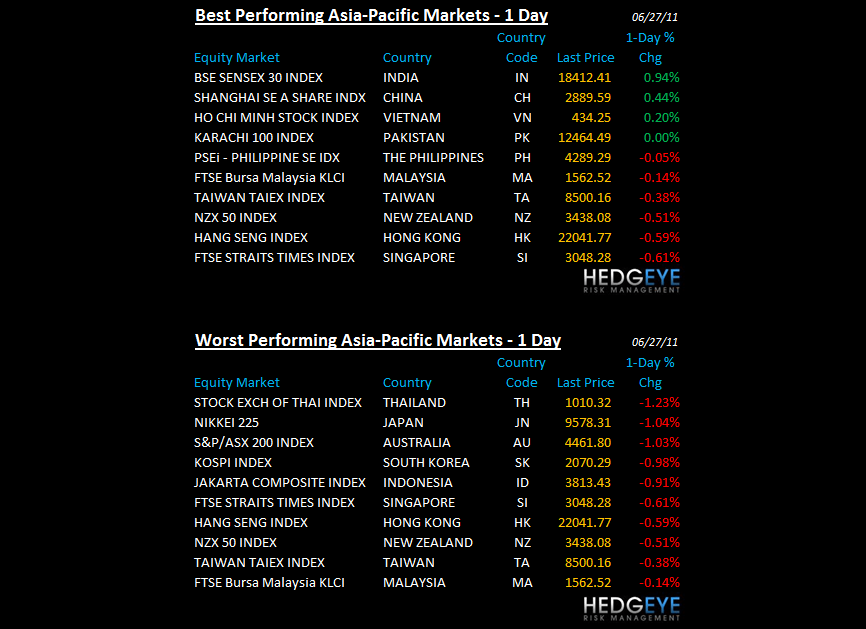

- Asian market are generally weaker (we are short Japan down -1.03%) and LONG China up +0.44%

MIDDLE EAST

Howard Penney

Managing Director