Positions in Europe: Long Germany (EWG); Short Spain (EWP)

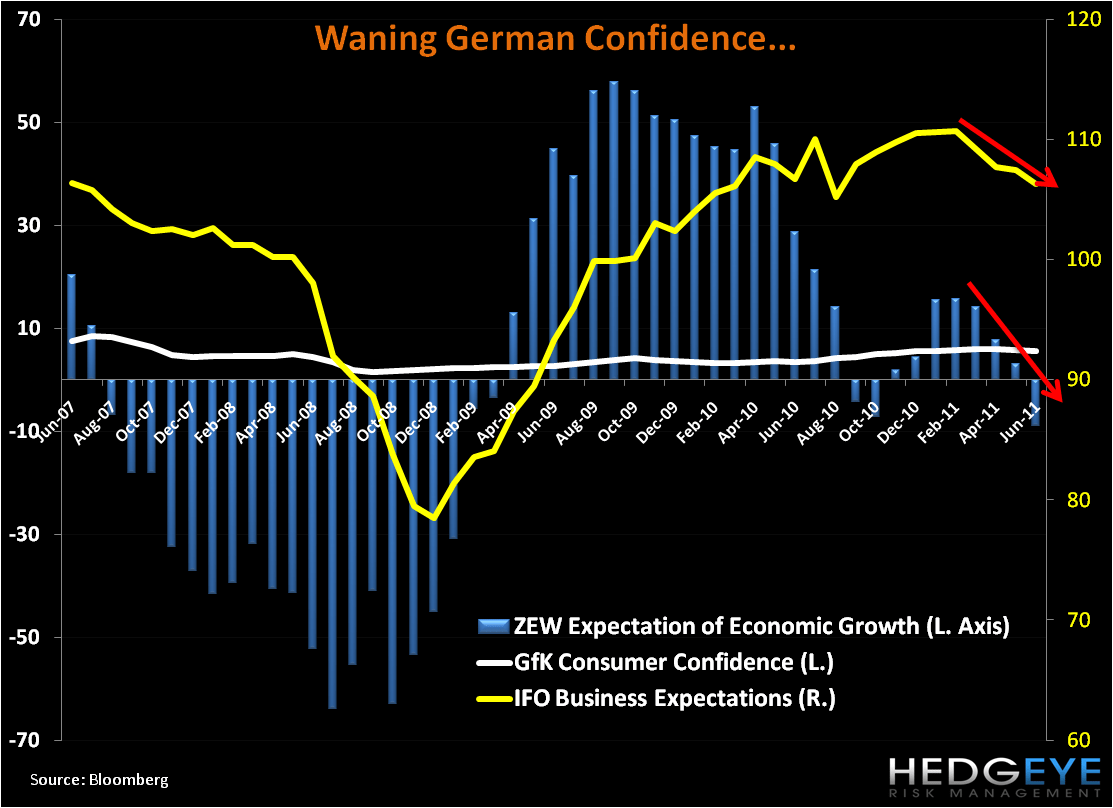

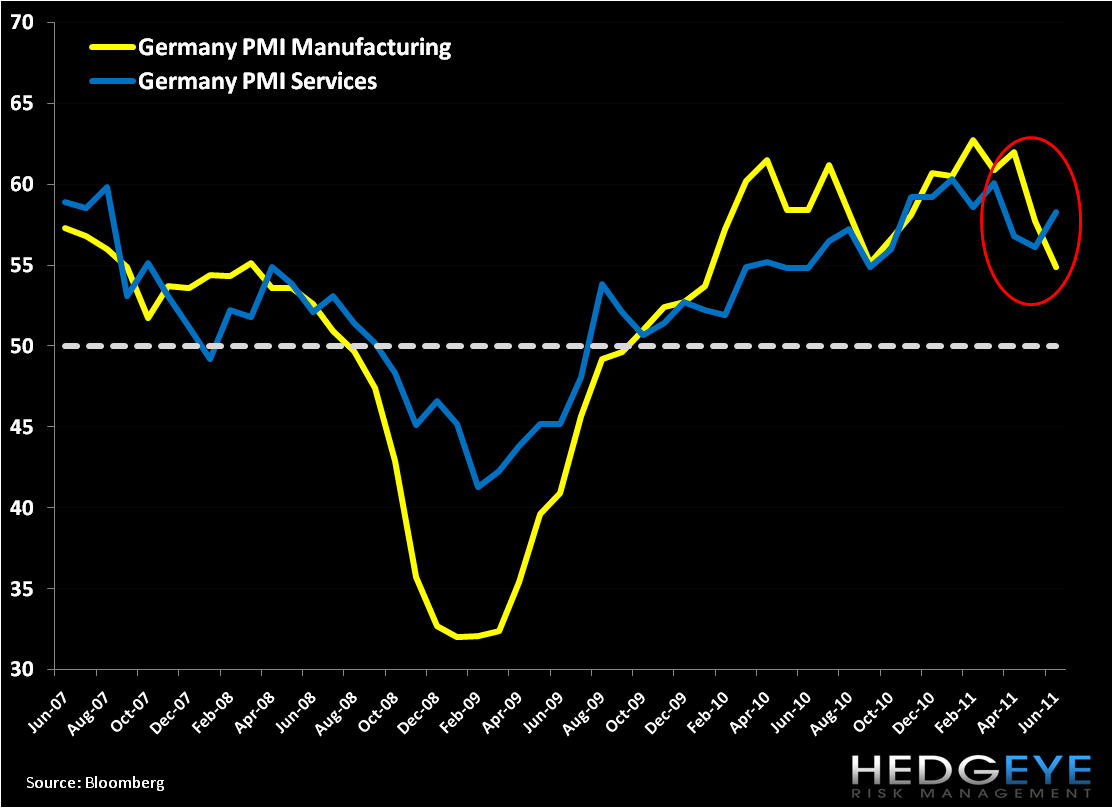

In sizing up our macro position in Germany, which we’re long in the Hedgeye Virtual Portfolio via the etf EWG, we want to emphasize that the high frequency data has slowed in recent months. While Germany continues to reflect a strong growth profile for 2011, especially when compared to many of its neighbors handcuffed by gross fiscal imbalances, high unemployment, government indecision and unruly populous’ over austerity measures, the charts below show that German consumer and business confidence have waned over the last four months, as forward-looking Services and Manufacturing PMI surveys have also tailed off—Manufacturing has declined for the last two months as Services has been mixed and off ytd highs established in Q1 (see charts below).

While we still like Germany’s fiscal discipline and ability to find demand for its goods and services, the risk that Germany does not meet its growth forecasts given the pressing macro climate makes us more cautious on the position. GDP forecasts include:

German Government: 2.6% in 2011. (Chancellor Merkel indicated in late May that GDP will probably be above 3% in 2011)

German-based Institute for the World Economy: 3.6% in 2011; 1.6% in 2012

Bundesbank: 3.1% in 2011; 1.8% in 2012

Contagion from the periphery remains a glaring threat. While the Troika (EU, IMF, ECB) appears poised to step in to save Greece at every step with additional funds and more favorable terms on its debt, great uncertainty exists on how long the Greek state will be subsidized by Big Brother, and the impact of similar issues for larger countries like Spain and Italy. The obvious spill-over risk could dent not only the German equity market, but also the common currency. Certainly while a weaker EUR is to Germany’s advantage, we’re certain that if a real currency crisis emerged, the advantage of “cheap” German exports wouldn’t be of note.

For now we’re managing our exposure to Germany real-time. The DAX is trading just above its intermediate term TREND support line of 7,106 (third chart below). Stay tuned.

Matthew Hedrick

Analyst