The trends at JACK are getting better “on the margin” but the company is not in the clear just yet. As I see it, the current risk/reward is favorable. JACK is the last QSR company with a market capitalization over a billion that is trading below 6.0x EV/EBITDA. By comparison, the average multiple for the QSR sector is now at 9.8X EV/EBITDA. However, excluding CMG and GMCR, the QSR average multiple drops to 8.6X EV/EBITDA.

If JACK’s fundamental were to continue improving “on the margin” and the street were to reward the company with a higher multiple, I believe there could be over $10 of upside in the stock, or +40% from current levels.

The case for investors to revalue the stock over the next twelve months is as follows:

- 70% to 80% franchise mix by the end of fiscal year 2013 (just 18 months out) in line with other in the QSR space (the company needs to sell approximately 300 restaurants between now and the end of 2013.)

- 16% restaurant level margins by 2013

- Slowing franchise remodel incentive payments in FY2012

- “Deflating the Inflation” into FY2012

THE TOP-LINE AT A GLANCE

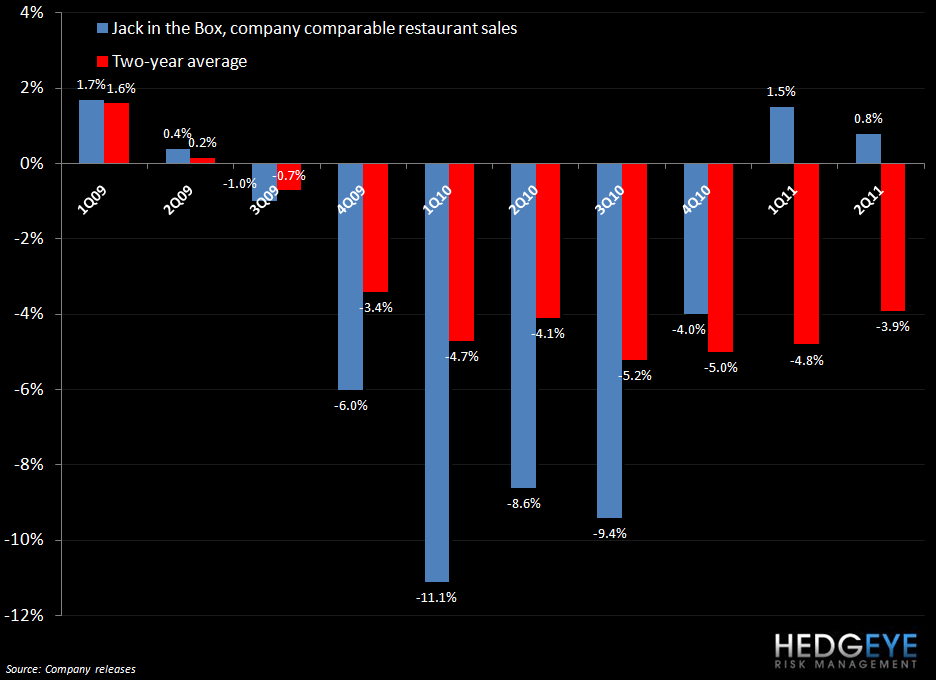

I see FY3Q11 same-store sales growth guidance of +2-4% for Jack in the Box company units is reasonable, given the sequential improvement in two-year average trends during fiscal 2Q11 and the stable/improving QSR MACRO environment.

The full-year guidance of +1-3%, though not completely out of reach, seems to be a bit more of a stretch given that the company would have to achieve a nearly 150 bp improvement in two-year average trends during the fourth quarter to hit the low end of the range, assuming 3Q11 same-store sales come in at 2%. I would note that SONC showed a 645 basis point improvement in 2-yr trends at company-owned restaurants between 2QFY11 and 3QFY11 (quarters ended February and May, respectively). For Jack in the Box, the YOY comparison gets increasingly more difficult during fiscal 4Q11 as the company is lapping a -4.0% comp from 4Q10 relative to -9.4% in 3Q10.

The Qdoba same-store sales growth target of +4-6% for both fiscal 3Q11 and the full year seem easily achievable given recent two-year average trends.

MARGIN TRENDS AT A GLANCE

The company’s commodity inflation guidance of up 6-7% in fiscal 3Q11 and +4.5-5.5% for the full year implies commodities are up about 5-8% during the fourth quarter, which will continue to put pressure on restaurant level margins. There is some risk to this commodity guidance as management has been incorrect in its prior guidance of these costs, initially guiding to inflation of +1-2% and then +3-4%. And, given recent commodity trends, I would expect the company’s commodity costs, particularly, its beef costs (guided to a 14% increase in full-year beef costs), to exceed the company’s current expectations.

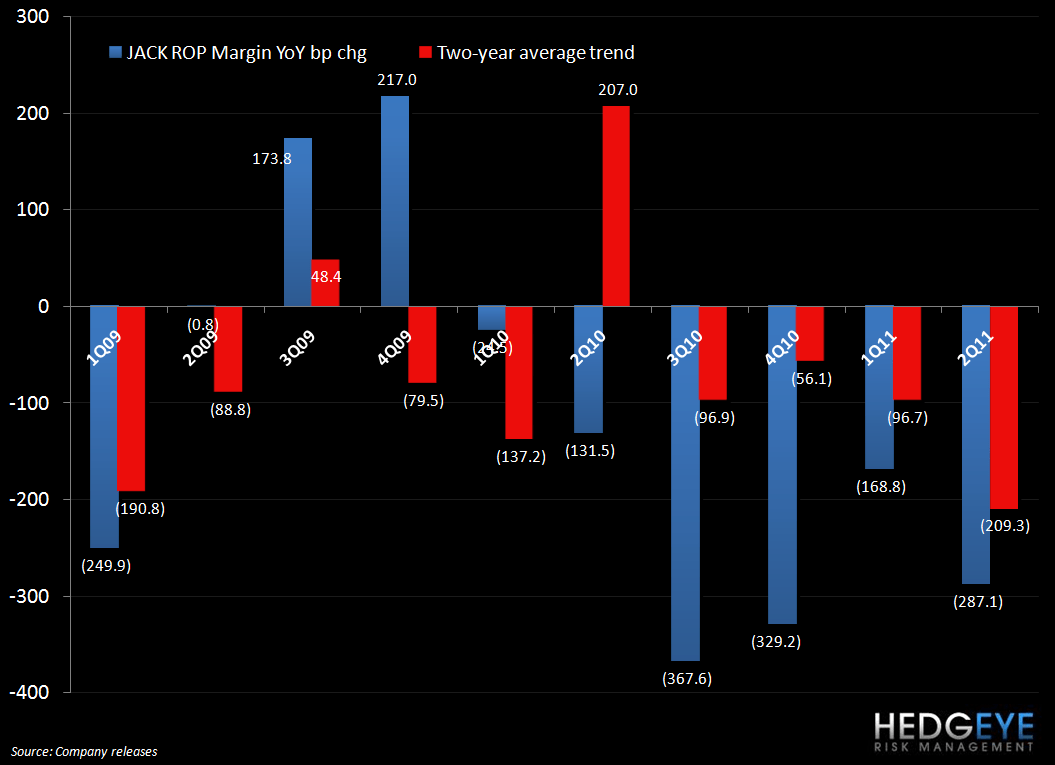

JACK’s full-year restaurant level margin guidance of 12.5% to 13.5% implies the YOY margin declines moderate during the second half of the year. It is important to remember that following the first quarter’s 170 bp decline in restaurant level margins, management guided to a significant improvement in YOY trends for the remaining three quarters. Fiscal 2Q11 margins, however, declined nearly 290 bps, largely as a result of the larger-than-expected increase in commodity costs. Margins have also been negatively impacted YOY by the company’s investment in guest service initiatives, which at least is a high quality problem.

JACK has posted margin declines for the last seven quarters. I would expect margins to continue to contract YOY during the second half of the year, but the magnitude of these declines should moderate significantly from fiscal 1H11, with the fourth quarter being less bad than the third on a YOY bp change basis. Obviously, if same-store sales growth surprises to the upside, stronger margin trends could result.

JACK has not yet turned the corner, but same-store sales trends have stabilized and turned positive during 1H11. Trends are still fairly negative on a two-year average basis but are improving nonetheless. Margin improvements should slowly follow with margins beginning to stabilize in 2H11. That being said, current commodity pressure will only slow this process.

OTHER THING TO CONSIDER:

- The company is lapping its 53rd week from fiscal 2010 in fiscal 4Q11.

- JACK increased its share repurchases during fiscal 1H11 to $75 million from $50 million during 1H10.

- The company’s diluted share count decreased 8.6% YOY during 2Q11. Full-year earnings will continue to benefit from this lower YOY share count and continued share repurchases.

Howard Penney

Managing Director