Conclusion: History suggests that releases from the SPR lead to lower crude prices over the next three months. Longer term, the potential disruption of marginal production will be supportive of higher prices.

To say we were surprised by the decision of the International Energy Association today to release oil from the Strategic Petroleum Reserve is an understatement. In aggregate, the United States and 27 allies will release 60 million barrels. The total releases by geography will be the U.S. at 30 million barrels, Europe at 15 million barrels, and Japan, Australia, New Zealand, and South Korea at 5 million barrels.

Ostensibly, the rationale of this release is to offset the disruption from Libya, which has reduced Libya oil production from 1.58 million barrels per day to 100,000 barrels per day as of May. The 60 million barrels will offset the disrupted production from Libya for an estimated 40 days. So, to borrow from Chairman Bernanke, this is only a "transitory" increase in supply.

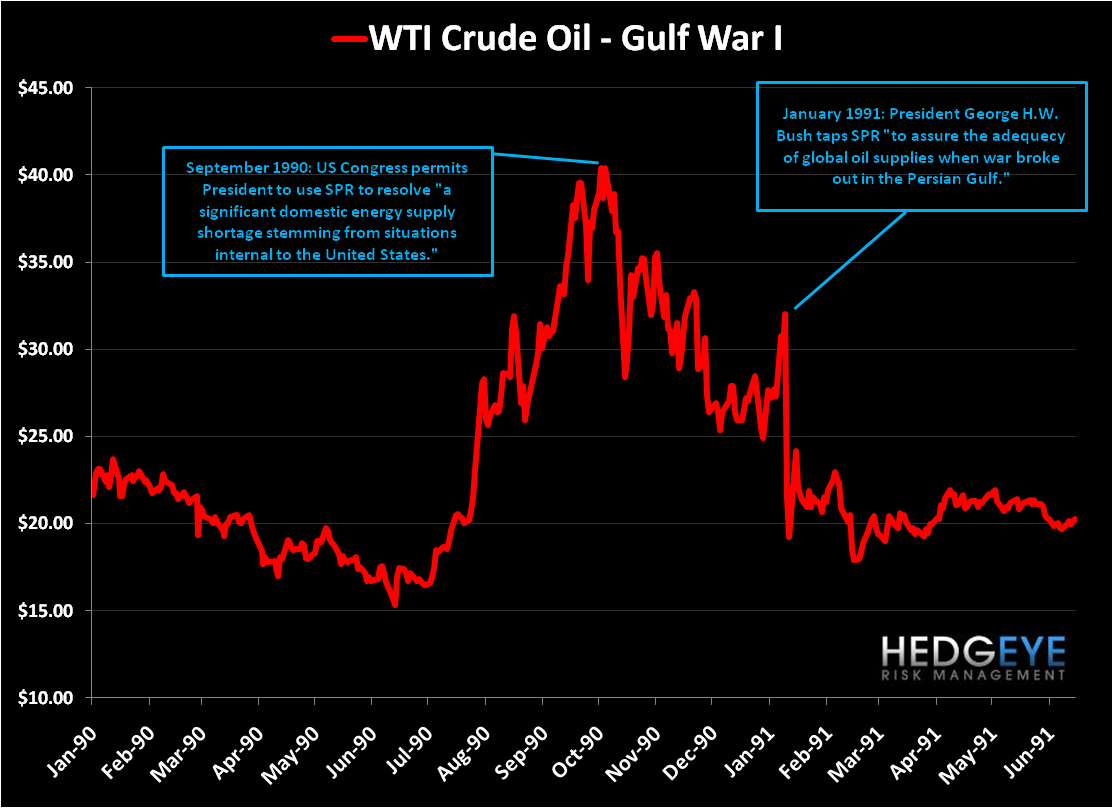

Nonetheless, history suggests that a release from the SPR has been a catalyst for lower prices in the future. The U.S. has released reserves from the SPR twice before, both times were bearish for crude prices – in 1991 during the Gulf War and in 2005 after Hurricane Katrina. In both instances, crude moved lower on both the TRADE (3 weeks) and TREND (3 months or more) durations. The two charts below highlight this point.

Longer term, though, the impact is probably less bullish for oil prices. On a simple level, lower oil prices discourage marginal production. In an increasingly energy-short world, this is not positive for supply in the long run. As our Energy Team recently noted:

“Since 1965 global oil production has grown at 2.1% while crude consumption has grown 2.8%, and that gap is widening; currently, neither OPEC nor Non-OECD nations have the spare capacity to satisfy the developing world’s growing appetite for energy. Within the last ten years, non-OECD oil consumption has grown nearly ~4%, while over the same duration global oil production has grown less than ~1%. In short, artificially manipulating prices eventually leads to supply dislocations and that in the long-run fuels higher prices in the physical markets.”

Our long-term of view of an imbalance in the global oil market has not changed, but in the short term this release from the SPR could well be a catalyst for lower prices. Our TAIL support line is currently at $89.76, if oil breaks that price sustainably, we would expect another leg down in the price of oil. Prices are reflexive, afterall.

Daryl G. Jones

Managing Director