TODAY’S S&P 500 SET-UP - June 23, 2011

As our CEO, Keith McCullough, said today about Ben Bernanke's performance, the poor guy is confused. “If my forecasts were wrong by a half-bagger this year, I'd be too.” Ultimately, Mr. Bernanke Keynesian Experiment is failing - and markets are figuring that out. As we are seeing in the Eurozone today growth continues to be lower than hopeful expectations, and the Fed's estimates for growth remain too high. We shorted the S&P500 ahead of Bernanke walking down his forecasts.

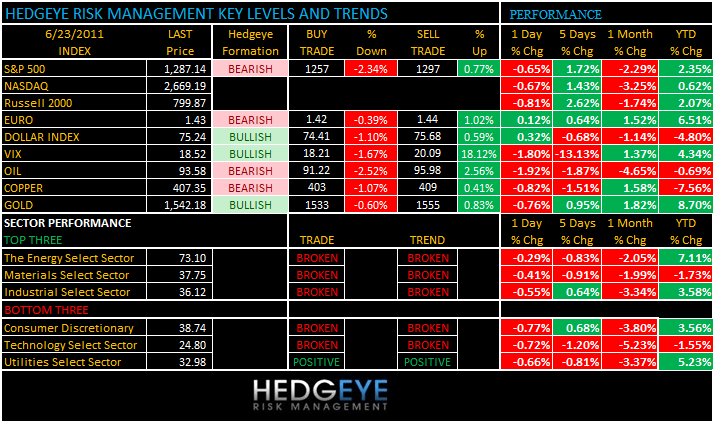

As we look at today’s set up for the S&P 500, the range is 40 points or -2.34% downside to 1257 and 0.77% upside to 1297.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: -521 (-2688)

- VOLUME: NYSE 856.36 (+0.61%)

- VIX: 18.52 -1.80% YTD PERFORMANCE: +4.34%

- SPX PUT/CALL RATIO: 2.01 from 1.57 (+27.44%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 23.54

- 3-MONTH T-BILL YIELD: 0.02%

- 10-Year: 3.01 from 2.99

- YIELD CURVE: 2.62 from 2.59

MACRO DATA POINTS:

- Initial Jobless and Continuing Claims at 08:30 ET

- Bloomberg Consumer Comfort Index for w/e 19-Jun at 09:45 ET

- May New Home Sales at 10:00 ET

- EIA Natural Gas Inventories for w/e 17-Jun at 10:30 ET

WHAT TO WATCH:

- ECB President Trichet said risk signals for euro-area financial stability are flashing “red” as the debt crisis threatens to infect banks

- IMF chief candidate Lagarde expected to speak to reporters

- Supreme Court rulings expected

- BJ's Wholesale wants $55/share from Leonard Green/CVC - NY Post

- Regulators look at freight-rail industry - WSJ

- 'Shadow housing inventory' declines in the US - FT

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Commodities Tumble After Federal Reserve Cuts Growth, Employment Forecasts

- Zinc Production Dropping in Japan to Double Imports to Highest in 11 Years

- France’s Sarkozy Urges Action Against the ‘Plague’ of Food Price Surges

- Mitsubishi Materials Agrees Annual Processing Fees for Copper Ore With BHP

- Crude Declines on Demand Concerns After Fed Lowers U.S. Economic Forecast

- Corn Futures Drop to Three-Month Low as Better U.S. Weather Reduces Risks

- Lending Crackdown Sidestepped as Soybeans Become Collateral: China Credit

- Gold May Decline From Seven-Week High as Fed Damps Stimulus Speculation

- Rubber in Tokyo Drops to Six-Week Low on Demand Concerns, Expanding Supply

- Copper May Drop for a Second Day as Europe’s Debt Crisis Threatens Banks

- Silver’s 74% Surge Creates ‘Headwind’ for Solar Rivalry With Fossil Fuels

- Tea Exports From India to Climb as Output Rebounds, African Supplies Drop

- Cargill, Royal DSM Are Said to Make Bids in $2.6 Billion Sale of Provimi

- K + N Pushes Maersk to One-Click Shipping in Ryanair Mold: Freight Markets

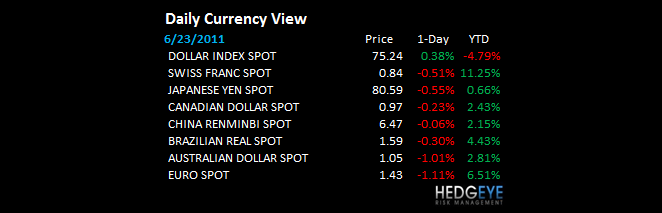

CURRENCIES

EUROPEAN MARKETS

- EUROPE: flat out ugly; Spain and Italy -1.5% each (were short Spain) on the realization that the sovereign debt default cycle is in early innings

- Eurozone Jun preliminary Manufacturing PMI 52.0 vs consensus 53.8 and prior 54.6

- Eurozone Jun preliminary Services PMI 54.2 vs consensus 55.5 and prior 56.0

- Eurozone Jun preliminary Composite PMI 53.6 vs consensus 55.1 and prior 55.8

ASIAN MARKETS

- ASIA: dazed/confused but Chinese stocks up for the 3rd consecutive day, closing +1.5%, and we like that because we are now long China.

MIDDLE EAST

Howard Penney

Managing Director