Notable news items and price action from the restaurant space as well as our fundamental view on select names.

MACRO

It seems that inflation is continuing to subside as the stronger dollar impacts market prices of commodities today. Supply and demand dynamics, however, continue to point higher for agricultural commodities; speculation mounted yesterday that hot weather in the growing areas of the U.S. may limit corn and soybean crop prospects this year.

Yesterday, the ICSC cut its forecast for June comps, now sees up 2%-3% ex-fuel, had seen 3%-4%. We are short CBRL in the Hedgeye virtual portfolio and very cautious on CAKE.

QUICK SERVICE

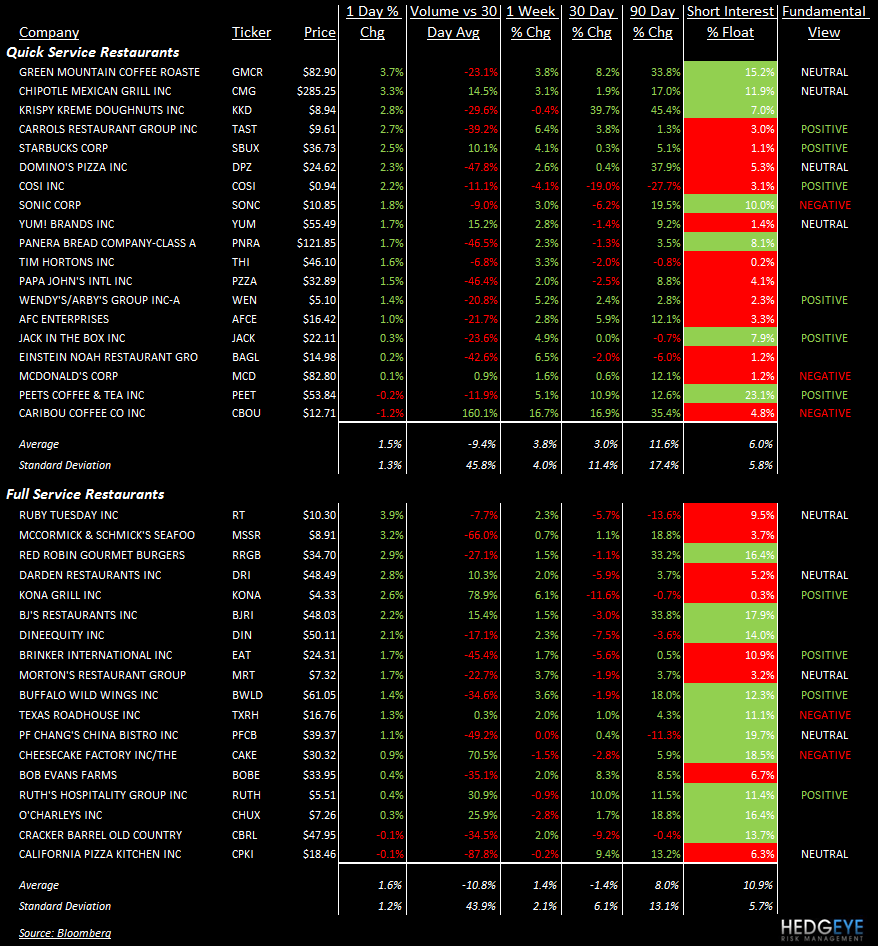

- SBUX is a Buy, according to UBS with upside to Fiscal 2012 consensus EPS in what the bank describes as “one of the best large capitalization growth stories” in consumer.

Hedgeye: While we are long SBUX in the Hedgeye Virtual Portfolio and believe that the CPG business offers SBUX room to continue its growth trajectory, from a quantitative perspective the stock is immediate-term TRADE overbought.

- KKD is going healthy, selling fruit juice, yoghurt, and oatmeal.

- YUM Director of IR Timothy Jerzyk spoke at the Jeffries conference yesterday and highlighted his company’s belief that YUM can have 20,000 restaurants in China, with profit in the country growing by 15%. East Dawning, according to YUM, is a “great opportunity” for China growth.

Hedgeye: YUM is leveraging its superior position in China and emerging markets to gain an advantage over its competition. While the U.S. business is performing poorly, China is now so important for the company that, in order to be negative on YUM, one must be negative on China.

- WEN upgraded to hold from sell at Argus Research.

Hedgeye: We still think there are two negative data points not in the stock (remodels being rethought and breakfast not working).

- SONC to report EPS today - Comps System +4.9%; Franchise +4.7%; Company +6.1%

Hedgeye - expectation are now elevated to the point that it’s going to be hard to beat. The turnaround is well established. Valuation is rich at 9.1x EV/EBITDA. Without big upward revisions, the upside from here is about $1.10.

FULL SERVICE

- DRI is one of the cheapest shares out there, according to Morgan Stanley, with limited downside and a dividend hike in its “back pocket”. DRI reports 4QFY11 earnings on June 30.

Hedgeye: As I said yesterday, the SSS have accelerated, but the question remains about consumer preference for the promotion, especially given the double digit inflation the company is experiencing in seafood.

Howard Penney

Managing Director